Vodafone 2009 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2009 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Performance

Vodafone Group Plc Annual Report 2009 35

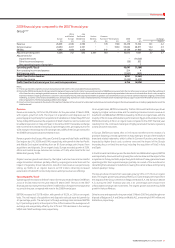

The impact of merger and acquisition activity and foreign exchange movements on

revenue, service revenue, EBITDA and adjusted operating profit are shown below:

Organic M&A Foreign Reported

growth activity exchange growth

% pps pps %

Revenue

Africa and Central Europe 13.6 6.0 1.2 20.8

Service revenue

Vodacom 16.5 – (7.9) 8.6

Other 11.2 9.5 6.6 27.3

Africa and Central Europe 13.2 6.2 1.6 21.0

EBITDA

Vodacom 18.3 – (7.9) 10.4

Other 13.9 3.6 3.6 21.1

Africa and Central Europe 15.6 2.1 (0.6) 17.1

Adjusted operating profit

Vodacom 19.1 – (7.5) 11.6

Other 17.0 52.7 (7.1) 62.6

Africa and Central Europe 18.0 22.6 (7. 5) 33.1

On an organic basis, voice revenue grew by 12.0% and messaging revenue and data

revenue rose by 6.6% and 103.9%, respectively, as a result of the 22.4% organic

increase in the average customer base.

Vodacom

Vodacom’s service revenue increased by 8.6%, or 16.5% at constant exchange rates,

which was a chieved largely th rough ave rag e customer grow th of 23 .1% . The customer

base was impacted by a change in the prepaid disconnection policy, which resulted

in 1.45 million disconnections in S eptember 20 07 a nd a hig her ongoing discon nection

rate. Vodacom’s data revenue growth remained very strong, driven by a rapid rise in

mobile PC connectivity devices.

Vodacom’s EBITDA rose by 10.4%, or 18.3% at constant exchange rates. The main

cost drivers were operating expenses, which increased by 19.3% at constant

exchange rates, and direct costs which grew by 17.1% at constant exchange rates,

primarily as a result of increased prepaid airtime commission following the growth

of the business. Growth at constant exchange rates was in excess of reported

growth as Vodacom’s reported performance in the 2008 financial year was

impacted by the negative effect of exchange rates arising on the translation of its

results into sterling.

Other Africa and Central Europe

Service revenue increased by 27.3%, by 11.2% on an organic basis, driven by

performances in Turkey and Romania.

At constant exchange rates, Turkey delivered revenue growth of 24%, assuming the

Group owned the business for the whole of both periods, with 25.2% growth in the

average customer base compared to the 2007 financial year. While growth rates

remained high, they slowed in the last quarter of the year, but remained consistent

with the overall growth rate for the market. In order to maintain momentum in an

increasingly competitive environment, the business concentrated on targeted

promotional offers and focused on developing distribution, as well as continued

investment in the brand and completing the planned improvements to network

coverage. The revenue performance year on year was principally as a result of

the increase in voice revenue driven by the rise in average customers, but also

benefited from the growth in messaging revenue, resulting from higher volumes.

In Romania, service revenue increased by 15.0%, or 19.6% at constant exchange

rates, driven by an 18.3% rise in the average customer base following the impact

of initiatives focusing on business and contract customers, as well as growth in

roaming revenue and a strong performance in data revenue following successful

promotions and a growing base of mobile data customers. However, service revenue

growth slowed in the last quarter, when compared to the same quarter in the 2007

financial year, in line with lower average customer growth, which was in turn driven

by increased competition in the market, with five mobile operators competing for

market share.

EBITDA grew by 21.1%, or by 13.9% on an organic basis, with the main drivers

of growth being Turkey and Romania.

Turkey generated strong growth in EBITDA, assuming the Group owned the business

for the whole of both periods, driven by the increase in revenue. The closing customer

base grew by 21.8% following additional investment in customer acquisition activities,

with the new connections in the year driving the higher customer costs. Direct costs

were up, mainly due to ongoing regulatory fees, which equate to 15% of revenue.

Operating expenses remained constant as a percentage of service revenue but

increased following continued investment in the brand and network in line with the

acquisition plan.

Romania’s EBITDA grew by 15.8%, or 20.9% at constant exchange rates, with increases

in costs being mitigated by ser vice revenue performance. Direct cos ts grew, reflecting

the 18.3% rise in the average customer base. As a percentage of service revenue,

customer costs increased as a result of the increased competition for customers.

Increases in the number of direct sales and distribution employees, following the

market trend towards direct distribution channels, led to a 6.6% increase in operating

expenses, or 11.0% at constant exchange rates.

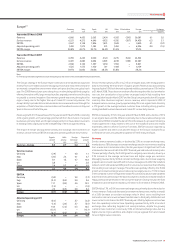

Asia Pacic and Middle East(1)

Asia Pacific

and Middle

India Other East % change

£m £m £m £ Organic

Year ended 31 March 2008

Revenue 1,822 2,577 4,399 87.4 15.9

Service revenue 1,753 2,348 4,101 90.4 16.2

EBITDA 598 878 1,476 78.7 14.3

Adjusted operating profit 35 495 530 12.3 8.1

EBITDA margin 32. 8% 34.1% 33.6%

Year ended 31 March 2007

Revenue – 2,347 2,347

Service revenue – 2,154 2 ,154

EBITDA – 826 826

Adjusted operating profit – 472 472

EBITDA margin – 35.2% 35.2%

Note:

(1) The Group revised its segment structure during the year. See note 3 to the consolidated

financial statements.

Vodafone continued to execute on its strategy to deliver strong growth in emerging

markets during the 2008 financial year, with the acquisition of Vodafone Essar

(formerly Hutchison Essar) in India and with strong performance in Egypt. The Group

began to differentiate itself in emerging markets, with initiatives such as the

introduction of Vodafone branded handsets.

On 8 May 2007, the Group continued to successfully increase it s portfolio in emerging

markets by acquiring companies with interests in Vodafone Essar, a leading operator

in the fast growing Indian mobile market, following which the Group controls

Vodafone Essar. The business was rebranded to Vodafone in September 2007.

In conjunction with the Vodafone Essar acquisition, the Group signed a memorandum

of understanding with Bharti Airtel, the Group’s former joint venture in India, on

infrastructure sharing and granted an option to a Bharti group company to buy its

5.60% direct interest in Bharti Airtel, which was exercised on 9 May 2007.

Revenue growth for the year ended 31 March 2008 was 87.4% for the region, or 15.9%

on an organic basis, with the key driver for organic growth being the increase in

service revenue of 90.4%, or 16.2% on an organic basis.

EBITDA increased by 78.7% for the year ended 31 March 2008, or 14.3% on an organic

basis, due to performances in Egypt and Australia.