Vodafone 2004 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2004 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

Annual Report 2004 Vodafone Group Plc

95

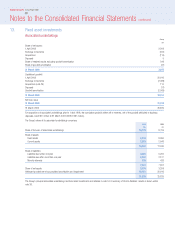

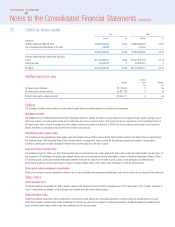

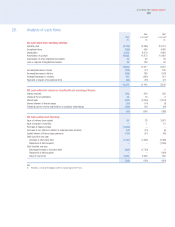

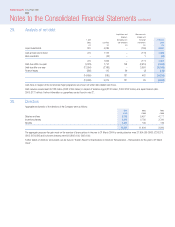

21. Provisions for liabilities and charges

Post

Deferred employment

taxation benefits Other provisions Total

£m £m £m £m

1 April 2003 3,032 217 447 3,696

Exchange movements (157) (3) (17) (177)

Disposals –(60) (6) (66)

Profit and loss account 744 41 180 965

Utilised in the year – payments –(123) (149) (272)

Other (11) (4) 66 51

31 March 2004 3,608 68 521 4,197

Deferred taxation

The deferred tax charge of £744 million (2003: £905 million) in respect of deferred tax liabilities excludes a charge to the profit and loss account of £47 million

(2003: £36 million) relating to associated undertakings and a credit to the profit and loss account of £49 million (2003: £129 million) relating to deferred tax

assets. Therefore the net deferred tax charge is £742 million (2003: £812 million), or £736 million (2003: £818 million) before exceptional items.

The net deferred tax liability/(asset) is analysed as follows:

2004 2003

£m £m

Accelerated capital allowances 1,652 1,383

Deferred tax on closure of derivative financial instruments (13) (48)

Deferred tax on overseas earnings 1,425 1,007

Other short term timing differences (19) (28)

Unrelieved tax losses (402) (306)

2,643 2,008

Analysed as:

Deferred tax asset (note 15) (965) (1,024)

Deferred tax provision 3,608 3,032

2,643 2,008

The amounts unprovided for deferred taxation are:

2004 2003

£m £m

Accelerated capital allowances (6) (170)

Gains subject to rollover relief 10 10

Other short term timing differences (118) (165)

Unrelieved tax losses (11,018) (11,226)

(11,132) (11,551)

A deferred tax asset has not been recognised in respect of unrelieved tax losses of £11,018 million (2003: £11,226 million), accelerated capital allowances of

£6 million (2003: £170 million) and short term timing differences of £118 million (2003: £165 million) as it is not anticipated that sufficient taxable profits will

arise within the foreseeable future.

The potential net tax benefit in respect of all tax losses carried forward at 31 March 2004, including amounts both recognised and unrecognised for deferred tax

purposes, was £50 million in United Kingdom subsidiaries (2003: £52 million) and £11,370 million in international subsidiaries (2003: £11,480 million). These

losses are only available for offset against future profits arising within these companies subject to the laws of the relevant jurisdiction. The Group’s share of

losses of international associated undertakings that are available for offset against future trading profits in these entities is £nil (2003: £225 million).

Other provisions

Other provisions primarily comprise amounts provided for legal claims, decommissioning costs and restructuring costs. The associated cash outflows for

restructuring costs are substantially short term in nature. For decommissioning costs, the associated cash outflows are generally expected to occur at the dates

of exit of the assets to which they relate, which are long term in nature. The timing of cash outflows associated with legal claims cannot be reasonably

determined.