Time Warner Cable 2014 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2014 Time Warner Cable annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

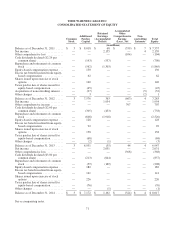

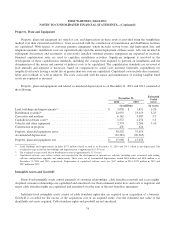

TIME WARNER CABLE INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Fair Value Estimates

Business Combinations

Upon the acquisition of a business, the fair value of the assets acquired and liabilities assumed must be estimated.

This requires judgments regarding the identification of acquired assets and liabilities assumed, some of which may not

have been previously recorded by the acquired business, as well as judgments regarding the valuation of all identified

acquired assets and assumed liabilities. The assets acquired and liabilities assumed are determined by reviewing the

operations, interviewing management and reviewing the financial, contractual and regulatory information of the acquired

business. Once the acquired assets and assumed liabilities are identified, the fair values of the assets and liabilities are

estimated using a variety of approaches that require significant judgments. For example, intangible assets are typically

valued using a discounted cash flow (“DCF”) analysis, which requires estimates of the future cash flows that are

attributable to the intangible asset. A DCF analysis also requires significant judgments regarding the selection of discount

rates that are intended to reflect the risks that are inherent in the projected cash flows, the determination of terminal

growth rates, and judgments about the useful life and pattern of use of the underlying intangible asset. As another

example, the valuation of acquired property, plant and equipment requires judgments about current market values,

replacement costs, the physical and functional obsolescence of the assets and their remaining useful lives. A failure to

appropriately assign fair values to acquired assets and assumed liabilities could significantly impact the amount and

timing of future depreciation and amortization expense, as well as significantly overstate or understate assets or liabilities.

Derivative Financial Instruments

Derivative financial instruments are recognized in the consolidated balance sheet as either assets or liabilities at fair

value and are designated, if certain conditions are met, as either (a) a hedge of the exposure to changes in the fair value of

a recognized asset or liability or an unrecognized firm commitment (a “fair value hedge”) or (b) a hedge of the exposure

to variable cash flows of a forecasted transaction or a hedge of the foreign currency exposure of a forecasted transaction

denominated in a foreign currency (a “cash flow hedge”). For a derivative financial instrument designated as a fair value

hedge (e.g., the Company’s interest rate swaps), the gain or loss on the derivative financial instrument is recognized in

earnings in the period of change together with the offsetting loss or gain on the hedged item attributable to the risk being

hedged. As a result, the consolidated statement of operations includes the impact of changes in the fair value of both the

derivative financial instrument and the hedged item, which reflects in earnings the extent to which the hedge is ineffective

in achieving offsetting changes in fair value. For a derivative financial instrument designated as a cash flow hedge (e.g.,

the Company’s cross-currency swaps), the effective portion of the gain or loss on the derivative financial instrument is

initially reported in equity as a component of accumulated other comprehensive income (loss), net, and subsequently

reclassified into earnings when the hedged item (e.g., a forecasted transaction denominated in a foreign currency) affects

earnings. The ineffective portion of the gain or loss is reported in earnings immediately. Derivative financial instruments

are used to manage the risks associated with fluctuations in interest rates and foreign currency exchange rates and are not

entered into for speculative or trading purposes.

The fair value of interest rate swaps is determined using a DCF analysis based on the terms of the contract. This

valuation requires estimates of future interest rates and judgments about the future credit worthiness of the Company and

each counterparty over the terms of the contracts. Similarly, the fair value of cross-currency swaps is determined using a

DCF analysis based on the terms of the contracts. This valuation requires estimates of future interest rates, forward

exchange rates and judgments about the future credit worthiness of the Company and each counterparty over the terms of

the contracts. Refer to Note 11 for further details.

75