Priceline 2010 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2010 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

101

paid $13.3 million in debt financing costs associated with the 2015 Notes for the year ended December 31, 2010.

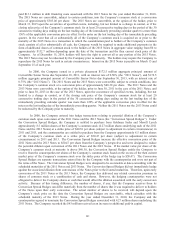

The 2015 Notes are convertible, subject to certain conditions, into the Company’s common stock at a conversion

price of approximately $303.06 per share. The 2015 Notes are convertible, at the option of the holder, prior to

March 15, 2015 upon the occurrence of specified events, including, but not limited to a change in control, or if the

closing sales price of the Company’s common stock for at least 20 consecutive trading days in the period of the 30

consecutive trading days ending on the last trading day of the immediately preceding calendar quarter is more than

150% of the applicable conversion price in effect for the notes on the last trading day of the immediately preceding

quarter. In the event that all or substantially all of the Company’s common stock is acquired on or prior to the

maturity of the 2015 Notes in a transaction in which the consideration paid to holders of the Company’s common

stock consists of all or substantially all cash, the Company would be required to make additional payments in the

form of additional shares of common stock to the holders of the 2015 Notes in aggregate value ranging from $0 to

approximately $132.7 million depending upon the date of the transaction and the then current stock price of the

Company. As of December 15, 2014, holders will have the right to convert all or any portion of the 2015 Notes.

The 2015 Notes may not be redeemed by the Company prior to maturity. The holders may require the Company to

repurchase the 2015 Notes for cash in certain circumstances. Interest on the 2015 Notes is payable on March 15 and

September 15 of each year.

In 2006, the Company issued in a private placement $172.5 million aggregate principal amount of

Convertible Senior Notes due September 30, 2011, with an interest rate of 0.50% (the “2011 Notes”), and $172.5

million aggregate principal amount of Convertible Senior Notes due September 30, 2013, with an interest rate of

0.75% (the “2013 Notes”). The 2011 Notes and the 2013 Notes were convertible, subject to certain conditions, into

the Company’s common stock at a conversion price of approximately $40.38 per share. The 2011 Notes and the

2013 Notes were convertible, at the option of the holder, prior to June 30, 2011 in the case of the 2011 Notes, and

prior to June 30, 2013 in the case of the 2013 Notes, upon the occurrence of specified events, including, but not

limited to a change in control, or if the closing sale price of the Company’s common stock for at least 20

consecutive trading days in the period of the 30 consecutive trading days ending on the last trading day of the

immediately preceding calendar quarter was more than 120% of the applicable conversion price in effect for the

notes on the last trading day of the immediately preceding quarter. Neither the 2011 Notes nor the 2013 Notes could

be redeemed by the Company prior to maturity.

In 2006, the Company entered into hedge transactions relating to potential dilution of the Company’s

common stock upon conversion of the 2011 Notes and the 2013 Notes (the “Conversion Spread Hedges”). Under

the Conversion Spread Hedges, the Company is entitled to purchase from Goldman Sachs and Merrill Lynch

approximately 8.5 million shares of the Company’s common stock (4.27 million shares underlying each of the 2011

Notes and the 2013 Notes) at a strike price of $40.38 per share (subject to adjustment in certain circumstances) in

2011 and 2013, and the counterparties are entitled to purchase from the Company approximately 8.5 million shares

of the Company’s common stock at a strike price of $50.47 per share (subject to adjustment in certain

circumstances) in 2011 and 2013. The Conversion Spread Hedges increase the effective conversion price of the

2011 Notes and the 2013 Notes to $50.47 per share from the Company’s perspective and were designed to reduce

the potential dilution upon conversion of the 2011 Notes and the 2013 Notes. If the market value per share of the

Company’s common stock at maturity is above $40.38, the Conversion Spread Hedges entitle the Company to

receive from the counterparties net shares of the Company’s common stock based on the excess of the then current

market price of the Company’s common stock over the strike price of the hedge (up to $50.47). The Conversion

Spread Hedges are separate transactions entered into by the Company with the counterparties and were not part of

the terms of the Notes. The Conversion Spread Hedges were designed to be exercisable at dates coinciding with the

scheduled maturities of the 2011 Notes and 2013 Notes. The Conversion Spread Hedges did not immediately hedge

against the associated dilution from conversions of the Notes prior to their stated maturities. Therefore, upon early

conversion of the 2011 Notes or the 2013 Notes, the Company has delivered any related conversion premium in

shares of common stock or a combination of cash and shares. However, the hedging counterparties were not

obligated to deliver the Company shares or cash that would offset the dilution associated with the early conversion

activity. Because of this timing difference, the number of shares, if any, that the Company receives from its

Conversion Spread Hedges can differ materially from the number of shares that it was required to deliver to holders

of the Notes upon their early conversion. The actual number of shares to be received will depend upon the

Company’s stock price on the date the Conversion Spread Hedges are exercisable, which coincides with the

scheduled maturity of the 2013 Notes. During the year ended December 31, 2010, the Company and the

counterparties agreed to terminate the Conversion Spread Hedges associated with 4.27 million shares underlying the

2011 Notes. The Company recorded the $43 million received as an increase to additional paid-in capital.