Priceline 2010 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2010 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

65

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

We manage our exposure to interest rate risk and foreign currency risk through internally established

policies and procedures and, when deemed appropriate, through the use of derivative financial instruments. We use

foreign exchange derivative contracts to manage short-term foreign currency risk.

The objective of our policies is to mitigate potential income statement, cash flow and fair value exposures

resulting from possible future adverse fluctuations in rates. We evaluate our exposure to market risk by assessing the

anticipated near-term and long-term fluctuations in interest rates and foreign exchange rates. This evaluation

includes the review of leading market indicators, discussions with financial analysts and investment bankers

regarding current and future economic conditions and the review of market projections as to expected future rates.

We utilize this information to determine our own investment strategies as well as to determine if the use of

derivative financial instruments is appropriate to mitigate any potential future market exposure that we may face.

Our policy does not allow speculation in derivative instruments for profit or execution of derivative instrument

contracts for which there are no underlying exposures. We do not use financial instruments for trading purposes and

are not a party to any leveraged derivatives.

We did not experience any material changes in interest rate exposures during the year ended December 31,

2010. Based upon economic conditions and leading market indicators at December 31, 2010, we do not foresee a

significant adverse change in interest rates in the near future.

However, we performed a sensitivity analysis to determine the impact a change in interest rates would have

on the fair value of our available for sale investments assuming an adverse change of 100 basis points. A

hypothetical 100 basis points (1.0%) increase in interest rates would have resulted in a decrease in the fair values of

our investments as of December 31, 2010 of approximately $3.8 million. These hypothetical losses would only be

realized if we sold the investments prior to their maturity.

As of December 31, 2010, the outstanding principal amount of our debt is approximately $575 million. We

estimate that the market value of such debt was approximately $0.9 billion as of December 31, 2010. A substantial

portion of the market value of our debt in excess of the carrying value is related to the conversion premium on the

bonds.

As a result of the acquisitions of Booking.com, Agoda and TravelJigsaw, we are conducting a significant

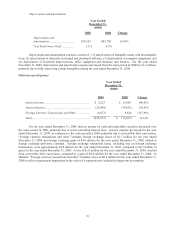

and growing portion of our business outside the United States through subsidiaries with functional currencies other

than the U.S. Dollar (primarily Euros). As a result, we face exposure to adverse movements in currency exchange

rates as the financial results of our international operations are translated from local currency into U.S. Dollars upon

consolidation. If the U.S. Dollar weakens against the local currency, the translation of these foreign-currency-

denominated balances will result in increased net assets, net revenues, operating expenses, and net income or loss.

Similarly, our net assets, net revenues, operating expenses, and net income or loss will decrease if the U.S. Dollar

strengthens against local currency. Additionally, foreign exchange rate fluctuations on transactions denominated in

currencies other than the functional currency result in gains and losses that are reflected in the Consolidated

Statement of Operations. Booking.com, Agoda and TravelJigsaw are subject to risks typical of international

business, including, but not limited to, differing economic conditions, changes in political climate, differing tax

structures, other regulations and restrictions, and foreign exchange rate volatility.

From time to time, we enter into foreign exchange derivative contracts to minimize the impact of short-

term foreign currency fluctuations on our consolidated operating results. Our derivative contracts principally address

foreign exchange fluctuation risk for the Euro. As of December 31, 2010, derivatives with a notional value of 30

million Euros that are not designated as hedging instruments for accounting purposes resulting in a liability of $0.2

million are recorded in “Accrued expenses and other current liabilities” in the Consolidated Balance Sheet. Foreign

exchange derivatives outstanding as of December 31, 2010 associated with foreign currency transaction risks that

are not designated as hedging instruments for accounting purposes resulted in an asset of $1.0 million, recorded in

“Prepaid expenses and other current assets” in the Consolidated Balance Sheet. As of December 31, 2009, there

were no outstanding contracts for derivatives not designated as hedging instruments. Foreign exchange gains of

$3.0 million and $4.0 million for the years ended December 31, 2010 and 2008, respectively, and foreign exchange

losses of $2.7 million for the year ended December 31, 2009, were recorded in “Foreign currency transactions and

other” related to foreign exchange derivative contracts. A hypothetical 10% strengthening of the foreign exchange

rates relative to the U.S. Dollar, with all other variables held constant, would have resulted in a derivative liability

balance of approximately $6 million as of December 31, 2010.