Priceline 2010 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2010 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

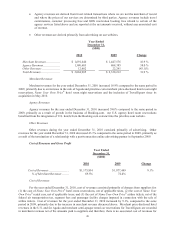

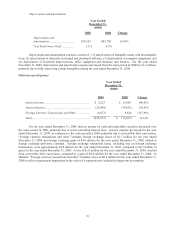

53

the year ended December 31, 2010, as compared to the same period in 2009, primarily due to an increase in the

average outstanding debt. “Foreign currency transactions and other” includes foreign exchange gains of $3.0

million and losses of $2.7 million for the years ended December 31, 2010 and 2009, respectively, related to foreign

exchange derivative contracts. Foreign exchange transaction losses including fees on foreign exchange transactions

were approximately $6.1 million and $2.9 million for the years ended December 31, 2010 and 2009, respectively.

The early conversion of convertible debt resulted in losses of $11.3 million and $1.0 million for the years ended

December 31, 2010 and 2009, respectively.

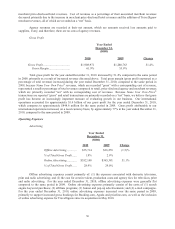

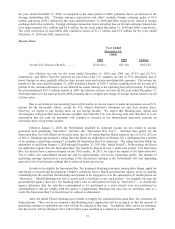

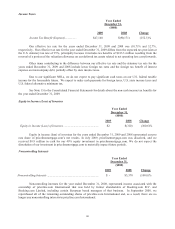

Income Taxes

Year Ended

December 31,

($000)

2010 2009 Change

Income Tax (Expense) Benefit ................ ($218,141) $47,168 (562.5)%

Our effective tax rate for the years ended December 31, 2010 and 2009 was 29.2% and (10.7)%,

respectively, and differs from the expected tax provision at the U.S. statutory tax rate of 35%, principally due to

lower foreign tax rates, partially offset by state income taxes and certain non-deductible expenses. The income tax

benefit for the year ended December 31, 2009 included a benefit of $183.3 million, resulting from the reversal of a

portion of the valuation allowance on our deferred tax assets relating to net operating loss carryforwards. Excluding

the aforementioned $183.3 million benefit in 2009, the effective income tax rates for the year ended December 31,

2010 decreased over the same period in 2009, primarily due to a higher percentage of foreign income which is taxed

at lower rates.

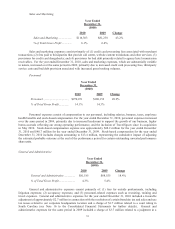

Due to our domestic net operating loss carryforwards, we do not expect to make tax payments on our U.S.

income for the foreseeable future, except for U.S. federal alternative minimum tax and state income taxes.

However, we expect to pay foreign taxes on our foreign income. We expect that Booking.com, Agoda and

TravelJigsaw will grow their pretax income at higher rates than the U.S. over the long term and, therefore, it is our

expectation that our cash tax payments will continue to increase as our international operations generate an

increasing share of our pretax income.

Effective January 1, 2010, the Netherlands modified its corporate income tax law related to income

generated from qualifying “innovative” activities (the “Innovation Box Tax”). Earnings that qualify for the

Innovation Box Tax will effectively be taxed at the rate of 5% rather than the Dutch statutory rate of 25.5% (25% as

of 2011). Booking.com obtained a ruling from the Dutch tax authorities in February 2011 confirming that a portion

of its earnings (“qualifying earnings”) is eligible for Innovation Box Tax treatment. The ruling from the Dutch tax

authorities is valid from January 1, 2010 through December 31, 2013 (the “Initial Period”). In this ruling, the Dutch

tax authorities require that the Innovation Box Tax benefit be phased in over a multi-year period. The Innovation

Box Tax did not have a material impact on our 2010 results. In 2011, we expect the impact of the Innovation Box

Tax to reduce our consolidated income tax rate by approximately one to two percentage points. The amount of

qualifying earnings expressed as a percentage of the total pretax earnings in the Netherlands will vary depending

upon the level of total pretax earnings that is achieved in any given year.

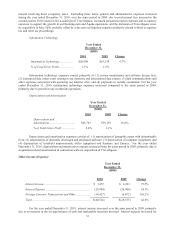

In order to be eligible for Innovation Box Tax treatment, Booking.com must, among other things, apply for

and obtain a research and development (“R&D”) certificate from a Dutch governmental agency every six months

confirming that the activities that Booking.com intends to be engaged in over the subsequent six month period are

“innovative.” Should Booking.com fail to secure such a certificate in any such period -- for example, because the

governmental agency does not view Booking.com’s new or anticipated activities as “innovative” -- or should this

agency determine that the activities contemplated to be performed in a prior period were not performed as

contemplated or did not comply with the agency’s requirements, Booking.com may lose its certificate and, as a

result, the Innovation Box Tax benefit may be reduced or eliminated.

After the Initial Period, Booking.com intends to reapply for continued Innovation Box Tax treatment for

future periods. There can be no assurance that Booking.com’s application will be accepted, or that the amount of

qualifying earnings or applicable tax rates will not be reduced at that time. In addition, there can be no assurance

that the tax law will not change in 2011 and/or future years resulting in a reduction or elimination of the tax benefit.