IBM 2013 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2013 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

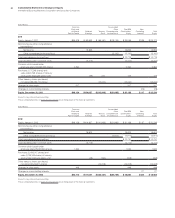

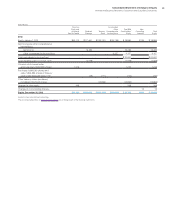

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies

89

Capitalized software costs incurred or acquired after technologi-

cal feasibility has been established are amortized over periods

ranging up to 3 years. Capitalized costs for internal-use software

are amortized on a straight-line basis over periods ranging up to 2

years. Other intangible assets are amortized over periods between

1 and 7 years.

Environmental

The cost of internal environmental protection programs that are

preventative in nature are expensed as incurred. When a cleanup

program becomes likely, and it is probable that the company will

incur cleanup costs and those costs can be reasonably estimated,

the company accrues remediation costs for known environmental

liabilities. The company’s maximum exposure for all environmental

liabilities cannot be estimated and no amounts are recorded for

environmental liabilities that are not probable or estimable.

Asset Retirement Obligations

Asset retirement obligations (ARO) are legal obligations associated

with the retirement of long-lived assets. These liabilities are initially

recorded at fair value and the related asset retirement costs are

capitalized by increasing the carrying amount of the related assets

by the same amount as the liability. Asset retirement costs are

subsequently depreciated over the useful lives of the related assets.

Subsequent to initial recognition, the company records period-to-

period changes in the ARO liability resulting from the passage of

time in interest expense and revisions to either the timing or the

amount of the original expected cash flows to the related assets.

Defined Benefit Pension and

Nonpension Postretirement Benefit Plans

The funded status of the company’s defined benefit pension plans

and nonpension postretirement benefit plans (retirement-related

benefit plans) is recognized in the Consolidated Statement of Finan-

cial Position. The funded status is measured as the difference

between the fair value of plan assets and the benefit obligation at

December 31, the measurement date. For defined benefit pension

plans, the benefit obligation is the projected benefit obligation (PBO),

which represents the actuarial present value of benefits expected

to be paid upon retirement based on employee services already

rendered and estimated future compensation levels. For the non-

pension postretirement benefit plans, the benefit obligation is the

accumulated postretirement benefit obligation (APBO), which rep-

resents the actuarial present value of postretirement benefits

attributed to employee services already rendered. The fair value of

plan assets represents the current market value of cumulative com-

pany and participant contributions made to an irrevocable trust

fund, held for the sole benefit of participants, which are invested by

the trust fund. Overfunded plans, with the fair value of plan assets

exceeding the benefit obligation, are aggregated and recorded as

a prepaid pension asset equal to this excess. Underfunded plans,

with the benefit obligation exceeding the fair value of plan assets,

are aggregated and recorded as a retirement and nonpension post-

retirement benefit obligation equal to this excess.

The current portion of the retirement and nonpension postretire-

ment benefit obligations represents the actuarial present value of

benefits payable in the next 12 months exceeding the fair value of

plan assets, measured on a plan-by-plan basis. This obligation is

recorded in compensation and benefits in the Consolidated State-

ment of Financial Position.

Net periodic pension and nonpension postretirement benefit

cost/(income) is recorded in the Consolidated Statement of Earnings

and includes service cost, interest cost, expected return on plan

assets, amortization of prior service costs/(credits) and (gains)/

losses previously recognized as a component of OCI and amortiza-

tion of the net transition asset remaining in accumulated other

comprehensive income/(loss) (AOCI). Service cost represents the

actuarial present value of participant benefits earned in the current

year. Interest cost represents the time value of money cost associ-

ated with the passage of time. Certain events, such as changes in

the employee base, plan amendments and changes in actuarial

assumptions, result in a change in the benefit obligation and

the corresponding change in OCI. The result of these events is

amortized as a component of net periodic cost/(income) over

the service lives or life expectancy of the participants, depending

on the plan, provided such amounts exceed thresholds which are

based upon the benefit obligation or the value of plan assets. Net

periodic cost/(income) is recorded in Cost, SG&A and RD&E in the

Consolidated Statement of Earnings based on the employees’

respective functions.

(Gains)/losses and prior service costs/(credits) not recognized

as a component of net periodic cost/(income) in the Consolidated

Statement of Earnings as they arise are recognized as a component

of OCI in the Consolidated Statement of Comprehensive Income.

Those (gains)/losses and prior service costs/(credits) are subse-

quently recognized as a component of net periodic cost/(income)

pursuant to the recognition and amortization provisions of appli

-

cable accounting guidance. (Gains)/losses arise as a result of

differences between actual experience and assumptions or as a

result of changes in actuarial assumptions. Prior service costs/

(credits) represent the cost of benefit changes attributable to prior

service granted in plan amendments.

The measurement of benefit obligations and net periodic cost/

(income) is based on estimates and assumptions approved by the

company’s management. These valuations reflect the terms of the

plans and use participant-specific information such as compensation,

age and years of service, as well as certain assumptions, including

estimates of discount rates, expected return on plan assets, rate of

compensation increases, interest crediting rates and mortality rates.