IBM 2013 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2013 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

67

Management Discussion

International Business Machines Corporation and Subsidiary Companies

earnings is not practicable. While the company currently does

not have a need to repatriate funds held by its foreign subsidiaries,

if these funds are needed for operations and obligations in the U.S.,

the company could elect to repatriate these funds which could

result in a reassessment of the company’s policy and increased

tax expense.

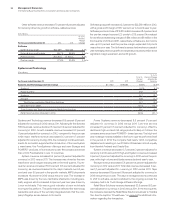

Contractual Obligations

($ in millions)

Total Contractual

Payment Stream

Payments Due In

2014 2015-16 2017-18 After 2018

Long-term debt obligations $36,978 $3,839 $ 8,656 $ 8,035 $16,448

Interest on long-term debt obligations 10,614 1,084 1,943 1,564 6,023

Capital (finance) lease obligations 58 16 25 12 5

Operating lease obligations 5,991 1,492 2,302 1,419 778

Purchase obligations 1,394 593 633 106 62

Other long-term liabilities:

Minimum defined benefit plan pension funding (mandated)* 3,300 600 1,300 1,400

Excess 401(k) Plus Plan 1,757 84 178 192 1,303

Long-term termination benefits 1,519 238 227 178 876

Tax reserves** 2,904 101

Other 1,052 44 93 80 836

To t a l $65,567 $8,091 $15,357 $12,986 $26,331

* As funded status on plans will vary, obligations for mandated minimum pension payments after 2018 could not be reasonably estimated.

**

These amounts represent the liability for unrecognized tax benefits. The company estimates that approximately $101 million of the liability is expected to be settled within the next

12 months. The settlement period for the noncurrent portion of the income tax liability cannot be reasonably estimated as the timing of the payments will depend on the progress

of tax examinations with the various tax authorities; however, it is not expected to be due within the next 12 months.

Total contractual obligations are reported in the table above excluding

the effects of time value and therefore, may not equal the amounts

reported in the Consolidated Statement of Financial Position. Certain

noncurrent liabilities are excluded from the table above as their future

cash outflows are uncertain. This includes deferred taxes, derivatives,

deferred income, disability benefits and other sundry items.

Purchase obligations include all commitments to purchase

goods or services of either a fixed or minimum quantity that meet

any of the following criteria: (1) they are noncancelable, (2) the com-

pany would incur a penalty if the agreement was canceled, or

(3) the company must make specified minimum payments even if

it does not take delivery of the contracted products or services

(take-or-pay). If the obligation to purchase goods or services is non-

cancelable, the entire value of the contract is included in the table

above. If the obligation is cancelable, but the company would incur

a penalty if canceled, the dollar amount of the penalty is included

as a purchase obligation. Contracted minimum amounts specified

in take-or-pay contracts are also included in the table as they rep-

resent the portion of each contract that is a firm commitment.

In the ordinary course of business, the company enters into con-

tracts that specify that the company will purchase all or a portion of

its requirements of a specific product, commodity or service from

a supplier or vendor. These contracts are generally entered into in

order to secure pricing or other negotiated terms. They do not

specify fixed or minimum quantities to be purchased and, therefore,

the company does not consider them to be purchase obligations.

Interest on floating-rate debt obligations is calculated using the

effective interest rate at December 31, 2013, plus the interest rate

spread associated with that debt, if any.

Off-Balance Sheet Arrangements

From time to time, the company may enter into off-balance sheet

arrangements as defined by SEC Financial Reporting Release 67

(FRR-67), “Disclosure in Management’s Discussion and Analysis

about Off-Balance Sheet Arrangements and Aggregate Con tractual

Obligations.”

At December 31, 2013, the company had no off-balance sheet

arrangements that have, or are reasonably likely to have, a material

current or future effect on financial condition, changes in financial

condition, revenues or expenses, results of operations, liquidity, capi-

tal expenditures or capital resources. See the table above for the

company’s contractual obligations, and note M, “Contingencies and

Commitments,” on page 121, for detailed information about the com-

pany’s guarantees, financial commitments and indemnification

arrangements. The company does not have retained interests in

assets transferred to unconsolidated entities or other material off-

balance sheet interests or instruments.

Critical Accounting Estimates

The application of GAAP requires the company to make estimates

and assumptions about certain items and future events that directly

affect its reported financial condition. The accounting estimates

and assumptions discussed in this section are those that the com-

pany considers to be the most critical to its financial statements.

An accounting estimate is considered critical if both (a) the nature

of the estimate or assumption is material due to the levels of