IBM 2013 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2013 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

70 Management Discussion

International Business Machines Corporation and Subsidiary Companies

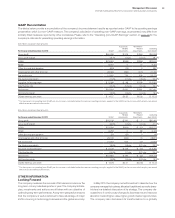

To the extent that actual collectibility differs from management’s

estimates currently provided for by 10 percent, Global Financing’s

segment pre-tax income and the company’s consolidated income

before income taxes would be higher or lower by an estimated $39

million (using 2013 data), depending upon whether the actual collect-

ibility was better or worse, respectively, than the estimates.

Residual Value

Residual value represents the estimated fair value of equipment

under lease as of the end of the lease. Residual value estimates

impact the determination of whether a lease is classified as operating

or capital. Global Financing estimates the future fair value of leased

equipment by using historical models, analyzing the current market

for new and used equipment, and obtaining forward-looking product

information such as marketing plans and technological innovations.

Residual value estimates are periodically reviewed and “other than

temporary” declines in estimated future residual values are recog-

nized upon identification. Anticipated increases in future residual

values are not recognized until the equipment is remarketed.

Factors that could cause actual results to materially differ from

the estimates include significant changes in the used-equipment

market brought on by unforeseen changes in technology innovations

and any resulting changes in the useful lives of used equipment.

To the extent that actual residual value recovery is lower than

management’s estimates by 10 percent, Global Financing’s segment

pre-tax income and the company’s consolidated income before

income taxes for 2013 would have been lower by an estimated

$94 million. If the actual residual value recovery is higher than man-

agement’s estimates, the increase in income will be realized at the

end of lease when the equipment is remarketed.

Currency Rate Fluctuations

Changes in the relative values of non-U.S. currencies to the U.S.

dollar affect the company’s financial results and financial position.

At December 31, 2013, currency changes resulted in assets and

liabilities denominated in local currencies being translated into fewer

dollars than at year-end 2012. The company uses financial hedging

instruments to limit specific currency risks related to financing trans-

actions and other foreign currency-based transactions. Further

discussion of currency and hedging appears in note D, “Financial

Instruments,” on pages 102 through 106.

Foreign currency fluctuations often drive operational responses

that mitigate the simple mechanical translation of earnings. During

periods of sustained movements in currency, the marketplace and

competition adjust to the changing rates. For example, when pricing

offerings in the marketplace, the company may use some of the

advantage from a weakening U.S. dollar to improve its position com-

petitively, and price more aggressively to win the business,

essentially passing on a portion of the currency advantage to

its customers. Competition will frequently take the same action.

Consequently, the company believes that some of the currency-

based changes in cost impact the prices charged to clients. The

company also maintains currency hedging programs for cash man-

agement purposes which mitigate, but do not eliminate, the volatility

of currency impacts on the company’s financial results.

The company translates revenue, cost and expense in its non-U.S.

operations at current exchange rates in the reported period.

References to “adjusted for currency” or “constant currency” reflect

adjustments based upon a simple constant currency mathematical

translation of local currency results using the comparable prior period’s

currency conversion rate. However, this constant currency method-

ology that the company utilizes to disclose this information does not

incorporate any operational actions that management may take in

reaction to fluctuating currency rates. Currency movements, particu-

larly the depreciation of the Yen, impacted the company’s year-to-year

revenue and earnings per share growth in 2013. Based on the currency

rate movements in 2013, total revenue decreased 4.6 percent as

reported and 2.5 at constant currency versus 2012. On a pre-tax

income basis, these translation impacts offset by the net impact of

hedging activities resulted in a theoretical maximum (assuming no

pricing or sourcing actions) decrease of approximately $400 million

in 2013. The same mathematical exercise resulted in a decrease of

approximately $100 million in 2012. The company views these amounts

as a theoretical maximum impact to its as-reported financial results.

Considering the operational responses mentioned above, movements

of exchange rates, and the nature and timing of hedging instruments,

it is difficult to predict future currency impacts on any particular period,

but the company believes it could be substantially less than the theo-

retical maximum given the competitive pressure in the marketplace.

For non-U.S. subsidiaries and branches that operate in U.S. dollars

or whose economic environment is highly inflationary, translation adjust-

ments are reflected in results of operations. Generally, the company

manages currency risk in these entities by linking prices and contracts

to U.S. dollars. The company continues to monitor the economic condi-

tions in Venezuela. On December 30, 2010, the official rate for essential

goods was eliminated, with no change to the SITME rate. The SITME

rate remained constant throughout 2012 and 2011. In February 2013, the

SITME rate was eliminated, and the official rate was set at 6.3 bolivares

fuerte (BsF) to the U.S. dollar. This devaluation did not have a material

impact given the size of the company’s operations in Venezuela (less

than 1 percent of total 2013 and 2012 revenue, respectively).

In addition, in March 2013, the Venezuelan government created

a new foreign exchange mechanism called the “Complimentary

System of Foreign Currency Aquirement.” This system operates

similar to an auction system and allows entities in specific sectors

to bid for U.S. dollars to be used for specific import transactions. In

December 2013, the Venezuelan regulation that created this mecha-

nism was amended to expand its use, and to require publication of

the average exchange rates implied by transactions settled in these

auctions. The company did not participate in this exchange mecha-

nism in 2013, and will consider its participation going forward.

In January 2014, the Argentinian government devalued its cur-

rency from 6 pesos to the U.S. dollar to 8 pesos to the U.S. dollar.

This devaluation will not have a material impact given the size of

the company’s operations in Argentina (less than 1 percent of total

2013 revenue).

Market Risk

In the normal course of business, the financial position of the

company is routinely subject to a variety of risks. In addition to the

market risk associated with interest rate and currency movements

on outstanding debt and non-U.S. dollar denominated assets and

liabilities, other examples of risk include collectibility of accounts

receivable and recoverability of residual values on leased assets.