Asus 2010 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2010 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

164

B. Dividends, stock warrants and other rights

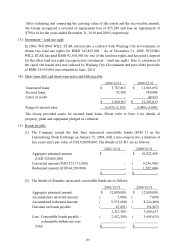

GDR holders and common share holders are all entitled to receive dividends. The

Depositary may issue new GDRs in proportion to GDRs holding ratios or raise the

number of shares of common stock represented by each unit of GDR or sell stock

dividends on behalf of GDR holders and distribute selling income to them in

proportion to their GDRs holding ratios.

19) Additional paid-in capital

The R.O.C. Securities and Exchange Act requires that capital reserve shall be exclusively used

to cover accumulated deficit or to increase capital and shall not be used for any other purpose.

However, capital reserve arising from paid-in capital in excess of par value on issuance of

common stock and donations can be capitalized once a year, provided that the Company has

no accumulated deficit and the amount to be capitalized does not exceed 10% of the paid-in

capital.

20) Retained earnings

(1) According to the Company’s articles of incorporation, annual net income after covering

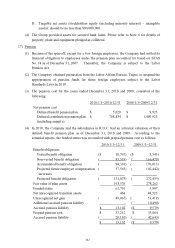

prior years’ losses, if any, should be distributed as follows: 10% as legal reserve, an

appropriate amount as special reserve according to relevant regulation or as required by

the government, 10% of capital stock as capital interest, no less than 1% as employees’

bonuses, and no more than 1% as directors’ and supervisors’ bonuses. When the

employees’ bonuses are distributed in stock, the recipients must include the employees of

subsidiaries. After the distribution of earnings, the remaining earnings, if any, may be

appropriated according to a resolution adopted in the stockholders’ meeting.

(2) The Company is facing a rapidly changing industrial environment, which is in the growth

phase. In light of the long-term financial plan of the Company and the demand for cash

by the stockholders, the Company should distribute cash dividends of no less than 10% of

the total dividends declared.

(3) Except for covering accumulated deficit or increasing capital, the legal reserve shall not

be used for any other purpose. Capitalization of the legal reserve is permitted, provided

that the balance of the reserve exceeds 50% of the Company’s paid-in capital and the

amount capitalized does not exceed 50% of the balance of the reserves.

(4) The appropriation of 2009 and 2008 earnings had been resolved at the stockholders’

meeting on April 22, 2010 and June 16, 2009, respectively. Details are summarized as

follows: