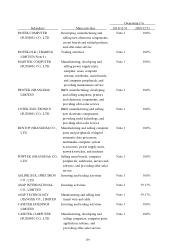

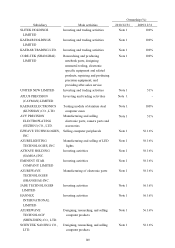

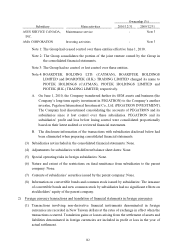

Asus 2010 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2010 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

149

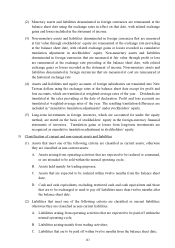

(2) Deferred income tax assets or liabilities are classified as current or non-current based on

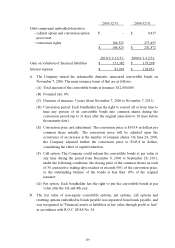

the classification of items that resulted in the deferred item or based on the timing of the

expected reversal, for certain transactions not directly related to an asset or liability.

When a change in the tax laws is enacted, the deferred tax liability or asset is recomputed

accordingly in the period of change. The difference between the new amount and the

original amount, that is, the effect of changes in the deferred tax liability or asset, is

recognized as an adjustment to current income tax expense (benefit).

(3) Over or under provision of prior years’ income tax liabilities is included in current year’s

income tax.

(4) The 10% additional income tax on unappropriated earnings is recorded as current income

tax expense when the shareholders resolve not to distribute the earnings.

(5) Current income tax is the higher of current income tax payable or the Alternative

Minimum Tax (“AMT”) calculated by applying the Income Basic Tax Act (“IBTA”). The

Company and domestic subsidiaries has taken into consideration the impact of the AMT

in the determination of its current income tax expense and its future impact when

estimating the realizable value of the deferred tax assets.

(6) The income tax for each consolidated entity is reported on an individual basis with the

relevant country and is not reported on a consolidated basis. The consolidated income

tax expense is the total of income tax expenses for all consolidated entities.

17) Treasury stock

(1) When the Company acquires its outstanding shares as treasury stock, the acquisition cost

should be debited to the treasury stock account (a contra account under stockholders’

equity) if the shares are purchased.

(2) When treasury stock is retired, the treasury stock account should be credited, and the

capital surplus-premium on stock account and capital stock account should be debited

proportionately according to the share ratio. An excess of the carrying value of treasury

stock over the sum of its par value and premium on stock should first be offset against

capital surplus from the same class of treasury stock transactions, and the remainder, if

any, debited to retained earnings. An excess of the sum of the par value and premium

on stock of treasury stock over its carrying value should be credited to additional paid-in

capital from the same class of treasury stock transactions.

(3) The cost of treasury stock is accounted for on a weighted-average basis.

18) Employees’ bonuses and directors’ and supervisors’ remuneration and share-based payment

Pursuant to Interpretation (96) 052 issued by the ARDF, the costs of employees’ bonuses and

directors’ and supervisors’ remuneration are accounted for as expenses and liabilities,

provided that such recognition is required under legal or constructive obligation and the

amounts can be estimated reasonably. However, if the accrued amounts for employees’

bonuses and directors’ and supervisors’ remuneration are significantly different from the

distributed amounts resolved by the Board of Directors, then the differences shall be adjusted

in current year’s gain or loss and, if the accrued amounts for employees’ bonus and directors’