Asus 2010 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2010 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

146

8) Long-term equity investments accounted for under equity method

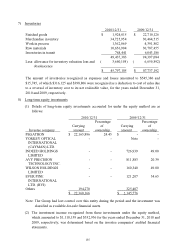

(1) Long-term investments are accounted for under the equity method when the percentage of

ownership held by the Group exceeds 20% or if the Company and its subsidiaries own

less than 20% of the investee’s common stock but have significant influence on the

investee’s operations. If an investee company accounted for under the equity method

issues new shares and the Company does not purchase new shares proportionately, then

the investment percentage, and therefore the equity in net assets of the investee, will be

changed. The effect of such change is adjusted against the additional paid-in capital

resulting from long-term equity investments or retained earnings.

(2) The difference between the cost of the investment and the amount of underlying equity in

net assets of an investee attributed to depreciable, depletable, or amortizable assets is

amortized over the estimated remaining economic years. The difference attributed to the

carrying amount in excess of or lower than the fair value of assets is written off entirely

when the difference disappear. The cost of investment in excess of the fair value of

identifiable net assets is recognized as goodwill and is no longer amortized. The

difference attributed to the fair value of identifiable net assets in excess of the cost of

investment causes a proportional decrease in the carrying amount of non-current assets.

When the carrying amount of non-current assets is reduced to zero, the remaining

difference is recorded as extraordinary gain or loss.

(3) When the equity of long-term equity investment under the equity method including

unrealized gain on financial instruments, foreign currency translation adjustments, net

loss not recognized as pension cost, and unrealized loss on cash flow hedges is changed,

the changes in percentage of ownership are reflected in those related accounts and

long-term equity investment under the equity method.

(4) Unrealized inter-company profit or loss resulting from transactions between the Group

and investees accounted for under the equity method are accounted in unrealized gain on

inter-affiliate accounts and are deferred until realized.

9) Investment – real estate

Investment – real estate is stated at cost, amortized by using the average method over the

contract period. If evidence of impairment exists the recovery from impairment is difficult,

impairment loss is recognized.

10) Property, plant and equipment, leased assets and idle assets

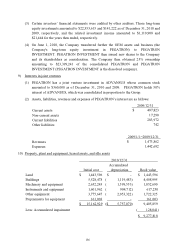

(1) Property, plant and equipment are stated at cost. Cost associated with significant

additions, improvements, and replacements to property, plant and equipment are

capitalized. Expenditures for regular repairs and maintenance are charged against

operating income.

(2) Property, plant and equipment leased to other parties under operating leases are classified

as leased assets. The related depreciation is provided under the straight-line method based

on the assets’ estimated useful lives and accounted for as a reduction of rental income.

Property, plant and equipment not currently used in operations are transferred to idle

assets. The cost, accumulated depreciation, and accumulated impairment of the original