Xerox 2002 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2002 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

49

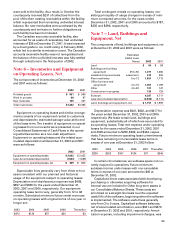

also other important criteria that are required to be

assessed, including whether collectibility of the lease

payments is reasonably predictable and whether

there are important uncertainties related to costs that

we have yet to incur with respect to the lease. In our

opinion, our sales-type lease portfolios contain only

normal credit and collection risks and have no impor-

tant uncertainties with respect to future costs. Our

leases in our Latin America operations have historical-

ly been recorded as operating leases since a majority

of these leases are terminated significantly prior to

the expiration of the contractual lease term. Specific-

ally, because we generally do not collect the receiv-

able from the initial transaction upon termination

or during any subsequent lease term, the recover-

ability of the lease investment is deemed not to be

predictable at lease inception. We continue to evalu-

ate economic, business and political conditions in the

Latin American region to determine if certain leases

will qualify as sales-type leases in future periods.

The critical estimates and judgments that we consid-

er with respect to our lease accounting are the deter-

mination of the economic life and the fair value

of equipment, including the residual value. Those esti-

mates are based upon historical experience with all our

products. For purposes of estimating the economic life,

we consider the most objective measure of historical

experience to be the original contract term, since most

equipment is returned by lessees at or near the end of

the contracted term. The estimated economic life of

most of our products is five years since this represents

the most frequent contractual lease term for our princi-

pal products and only a small percentage of our leases

have original terms longer than five years. We believe

that this is representative of the period during which

the equipment is expected to be economically usable,

with normal service, for the purpose for which it is

intended. We continually evaluate the economic life of

both existing and newly introduced products for pur-

poses of this determination. Residual values are estab-

lished at lease inception using estimates of fair value at

the end of the lease term. Our residual values are

established with due consideration to forecasted sup-

ply and demand for our various products, product

retirement and future product launch plans, end of

lease customer behavior, remanufacturing strategies,

used equipment markets if any, competition and tech-

nological changes.

The vast majority of our leases that qualify as

sales-type are non-cancelable and include cancella-

tion penalties approximately equal to the full value of

the leased equipment. Certain of our governmental

contracts may have cancellation provisions or renew-

al clauses that are required by law, such as (1) those

dependant on fiscal funding outside of a governmen-

tal unit’s control, (2) those that can be cancelled if

deemed in the taxpayer’s best interest or (3) those

that must be renewed each fiscal year, given limita-

tions that may exist on entering multi-year contracts

that are imposed by statute. In these circumstances

and in accordance with the relevant accounting litera-

ture, we carefully evaluate these contracts to assess

whether cancellation is remote or the renewal option

is reasonably assured of exercise because of the

existence of substantive economic penalties for the

customer’s failure to renew. Certain of our commer-

cial contracts for multiple units of equipment may

include clauses that allow for a return of a limited

portion of such equipment (up to 10 percent of the

value of equipment). These return clauses are only

available in very limited circumstances as negotiated

at lease inception. We account for our estimate of

equipment to be returned under these contracts as

operating leases.

Aside from the initial lease of equipment to our

customers, we may enter subsequent transactions

with the same customer whereby we extend the term.

We evaluate the classification of lease extensions of

sales-type leases using the originally determined eco-

nomic life for each product. There may be instances

where we have lease extensions for periods that are

within the original economic life of the equipment.

These are accounted for as sales-type leases only

when the extensions occur in the last three months of

the lease term and they otherwise meet the appropri-

ate criteria of SFAS No. 13. All other lease extensions

of this type are accounted for as direct financing leas-

es. We generally account for lease extensions that go

beyond the economic life as operating leases because

of important uncertainties as to the amount of servic-

ing and repair costs that we may incur.

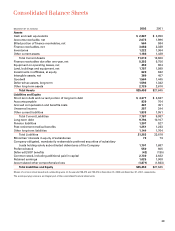

Cash and Cash Equivalents: Cash and cash

equivalents consist of cash on hand and investments

with original maturities of three months or less.

Restricted Cash and Investments: Due to our credit

ratings, many of our derivative contracts and several

other material contracts require us to post cash collat-

eral or maintain minimum cash balances in escrow.

These cash amounts are reported in our Consolidated

Balance Sheets within Other current assets or Other

long-term assets, depending on when the cash will be

contractually released. At December 31, 2002 and

2001, such restricted cash amounts were as follows: