Xerox 2002 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2002 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

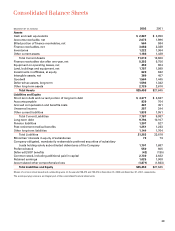

36

in Note 5 to the Consolidated Financial Statements.

We also utilized SPEs in our Trust Preferred Securities

transactions. Refer to Note 16 to the Consolidated

Financial Statements for a description of the Trust

Preferred Securities transactions.

Financial Risk Management:

We are exposed to market risk from changes in for-

eign currency exchange rates and interest rates that

could affect our results of operations and financial

condition. Our current below investment-grade credit

ratings effectively constrain our ability to fully use

derivative contracts as part of our risk management

strategy described below, especially with respect to

interest rate management. Accordingly, our results of

operations are exposed to increased volatility. As fur-

ther discussed in Note 1 to the Consolidated Financial

Statements, we adopted SFAS No. 133 as of January

1, 2001. The adoption of SFAS No. 133 has increased

the volatility of reported earnings and other compre-

hensive income. In general, the amount of volatility

will vary with the level of derivative and hedging

activities and the market volatility during any period.

We have historically entered into certain derivative

contracts, including interest rate swap agreements,

foreign currency swap agreements, forward exchange

contracts and purchased foreign currency options, to

manage interest rate and foreign currency exposures.

The fair market values of all our derivative contracts

change with fluctuations in interest rates and/or cur-

rency rates and are designed so that any change in

their values is offset by changes in the values of the

underlying exposures. Our derivative instruments are

held solely to hedge economic exposures; we do not

enter into derivative instrument transactions for trad-

ing or other speculative purposes and we employ

long-standing policies prescribing that derivative

instruments are only to be used to achieve a very lim-

ited set of objectives.

Our primary foreign currency market exposures

include the Japanese Yen, Euro, Brazilian Real, British

Pound Sterling and Canadian Dollar. Historically, for

each of our legal entities, we have generally hedged

foreign currency denominated assets and liabilities,

primarily through the use of derivative contracts.

Despite our current credit ratings, we have been able

to restore significant hedging activities with currency-

related derivative contracts during 2002. Although we

are still unable to hedge all our currency exposures,

we are currently utilizing the re-established capacity

primarily to hedge currency exposures related to our

foreign-currency denominated debt.

We typically enter into simple unleveraged deriva-

tive transactions. Our policy is to use only counterpar-

ties with an investment-grade or better rating and to

monitor market risk and exposure for each counter-

party. We also utilize arrangements allowing us to net

gains and losses on separate contracts with all coun-

terparties to further mitigate the credit risk associated

with our financial instruments. Based upon our ongo-

ing evaluation of the replacement cost of our deriva-

tive transactions and counterparty credit-worthiness,

we consider the risk of a material default by a counter-

party to be remote.

Due to our credit ratings, many of our derivative

contracts and several other material contracts at

December 31, 2002 require us to post cash collateral

or maintain minimum cash balances in escrow. These

cash amounts are reported in our Consolidated

Balance Sheets within Other current assets or other

long-term assets, depending on when the cash will be

contractually released. Such restricted cash amounts

totaled $77 million at December 31, 2002.

Assuming a 10 percent appreciation or deprecia-

tion in foreign currency exchange rates from the quot-

ed foreign currency exchange rates at December 31,

2002, the potential change in the fair value of foreign

currency-denominated assets and liabilities in each

entity would be insignificant because all material cur-

rency asset and liability exposures were hedged as of

December 31, 2002. A 10 percent appreciation or

depreciation of the U.S. Dollar against all currencies

from the quoted foreign currency exchange rates at

December 31, 2002, would have a $349 million impact

on our Cumulative Translation Adjustment portion of

equity. The amount permanently invested in foreign

subsidiaries and affiliates – primarily Xerox Limited,

Fuji Xerox and Xerox do Brasil – and translated into

dollars using the year-end exchange rates, was

$3.5 billion at December 31, 2002, net of foreign cur-

rency-denominated liabilities designated as a hedge

of our net investment.