Volvo 2004 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2004 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

89

US GAAP, the acquired operations have been consolidated and

accruals were made for intercompany profits in the year-end 2003

inventory of the L.B. Smith business. During 2004 the major part of

L.B. Smith has been divested and there are no GAAP difference

regarding L.B Smith, due to that the remaining part has been consol-

idated under Swedish GAAP in the year end closing of 2004.

Consolidation of the L.B. Smith distribution business under US

GAAP affected Volvo's income after financial items with 142 (nega-

tively 138). The Group's total assets are no longer effected

(SEK 1.1 billion).

In 2003, Volvo exchanged the main part of its shareholding in

Bilia AB versus 98% of the shares in Kommersiella Fordon Europa

AB (KFAB). In accordance with Swedish GAAP, the acquisition cost

of the shares in KFAB was determined to SEK 0.9 billion and the

goodwill attributable to this transaction amounted to SEK 0.6 billion.

In accordance with US GAAP, the acquisition cost of the shares

amounted to SEK 0.7 billion and the goodwill was determined to

SEK 0.5 billion. As a consequence, Volvo’s capital gain on the divest-

ment of Bilia shares was 179 lower under US GAAP than under

Swedish GAAP.

In 2001, AB Volvo acquired 100% of the shares in Renault V.I.

and Mack Trucks Inc. from Renault SA in exchange for 15% of the

shares in AB Volvo. Under Swedish GAAP, the goodwill attributable

to this acquisition was set at SEK 8.4 billion while under US GAAP

the corresponding goodwill was set at SEK 11.5 billion. The differ-

ence was mainly attributable to determination of the purchase con-

sideration. In accordance with Swedish GAAP, when a subsidiary is

acquired through the issue of own shares, the purchase consider-

ation is determined to be based on the market price of the issued

shares at the time of the transaction is completed. In accordance

with US GAAP, such a purchase consideration is determined to be

based on the market price of the underlying shares for a reasonable

period before and after the terms of the transaction are agreed and

publicly announced. The goodwill has been reduced with EUR 108 M

due to the settlement of the dispute between AB Volvo and Renault

SA regarding the final value of acquired assets and liabilities in

Renault V.I. and Mack Trucks.

In 1995, AB Volvo acquired the outstanding 50% of the shares in

Volvo Construction Equipment Corporation (formerly VME) from

Clark Equipment Company, in the US. In conjunction with the acquisi-

tion, goodwill of SEK 2.8 billion was reported. The shareholding was

written down by SEK 1.8 billion, which was estimated to correspond

to the portion of the goodwill that was attributable at the time of

acquisition to the Volvo trademark. In accordance with US GAAP, the

goodwill of SEK 2.8 billion was amortized over its estimated useful

life (20 years) until 2002 when Volvo adopted SFAS 142 (see

above).

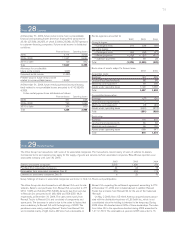

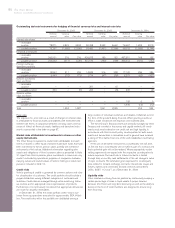

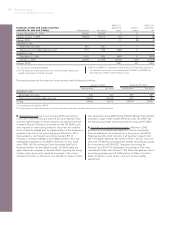

Net income Shareholders’ equity

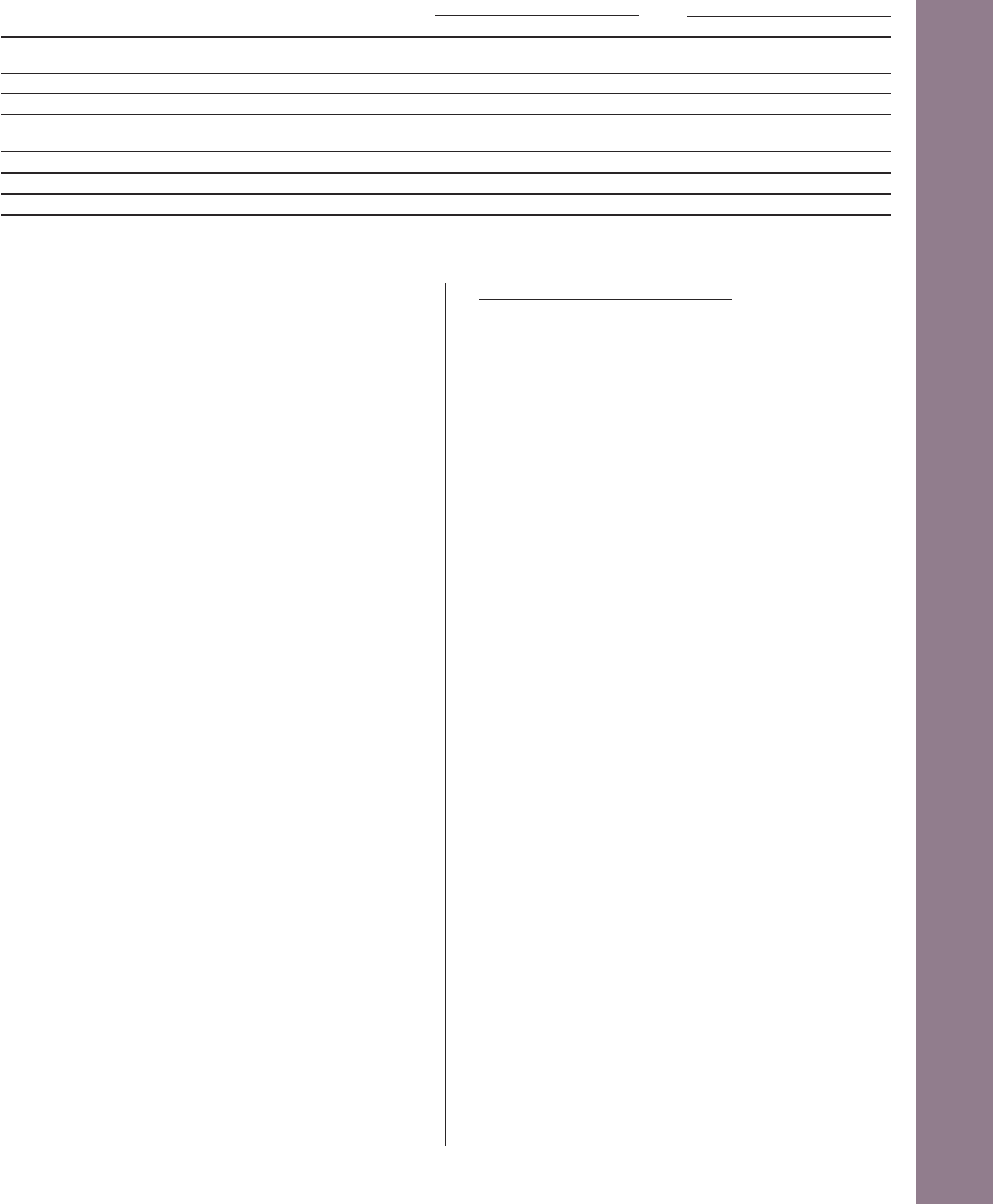

Goodwill 2002 2003 2004 2002 2003 2004

Goodwill in accordance with

Swedish GAAP (1,094) (873) (684) 11,297 11,151 9,655

Items affecting reporting of goodwill:

Acquisition of Renault V.I. and Mack Trucks Inc. 430 415 223 13,329 3,744 3,967

Acquisition of Volvo Construction

Equipment Corporation 51 51 51 1,277 1,328 1,379

Other acquisitions 613 407 410 613 841 1,251

Net change in accordance with US GAAP 1,094 873 684 5,219 5,913 6,597

Goodwill in accordance with US GAAP 0 0 0 16,516 17,064 16,252

1Lower amortization due to adjusted goodwill value resulting from the settlement of dispute between AB Volvo and Renault SA.

C. Investments in debt and equity securities. In accordance with US

GAAP, Volvo applies SFAS 115: “Accounting for Certain Investments

in Debt and Equity Securities.” SFAS 115 addresses the accounting

and reporting for investments in equity securities that have readily

determinable fair market values, and for all debt securities. These

investments are to be classified as either “held-to-maturity” securities

that are reported at amortized cost, “trading” securities that are

reported at quoted market prices with unrealized gains or losses

included in earnings, or “available-for-sale” securities, reported at

quoted market prices, with unrealized gains or losses being credited

or debited to Other comprehensive income and thereby included in

shareholders’ equity.

As of December 31, 2004, unrealized losses after deduction of

unrealized gains in “available-for-sale” securities amounted to 494

(2,315; 9,763). Sale of “available-for-sale” shares in 2004 provided

SEK 21.4 bilion (– ; –) and the capital gain, before income tax, on

sales of these shares amounted to SEK 24 (– ; –).

As set out above, all “available-for-sale” securities are valued at

quoted market price at the end of each fiscal year with the change

in value being credited or debited to Other comprehensive income.

However, if a security’s quoted market price has been below the

carrying value for an extended period of time, US GAAP include a

presumption that the decline in value is “other than temporary”. Under

such circumstances, US GAAP require that the value adjustment

must be recorded in Net income with a corresponding credit to

Other comprehensive income. Accordingly, value adjustments

amounting to 0 (62; 9,683), have been charged to Volvo’s net

income under US GAAP. During 2004 Volvo has divested the invest-

ment in Scania AB and a restructuring of Henlys Group plc has been

made. Henlys Group Plc. Earlier recorded value adjustments in the

income statement under US GAAP have been reversed with corre-

sponding adjustment in Other comprehensive income. After these

reversals, the remaining value of unrealized gains before tax credited

to Other comprehensive income amounted to 72 as of December

31, 2004.