Volvo 2004 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2004 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

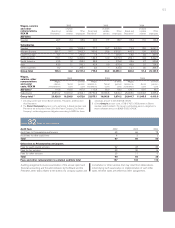

73

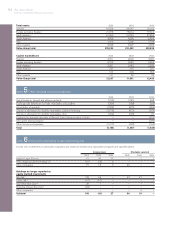

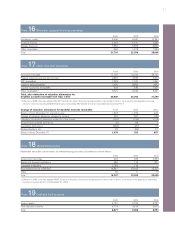

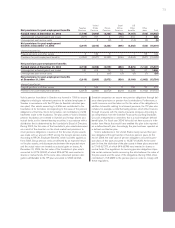

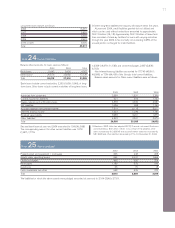

Pension costs 2002 2003 2004

Current service costs 646 616

Interest costs 1,377 1,306

Expected return on plan assets (828) (931)

Actuarial gains and losses1–(4)

Past service costs

– Unvested –7

– Vested 46 38

Curtailments and settlements 3(28)

Termination benefits 169 729

Pension costs for defined benefit plans 1,413 1,733

Pension costs for defined contribution plans 2,461 2,681

Total pension costs 4,472 3,874 4,414

1 For each plan, actuarial gains and losses are reported as income or expenses, when the accumulated amount exceeds the so called corridor. The income or

expenses are then recognized over the expected average remaining service period of the employees.

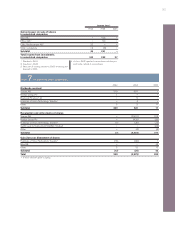

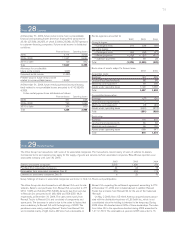

Costs for post-employment benefits other than pensions 2003 2004

Current service costs 107 196

Interest costs 415 349

Expected return on plan assets 0 (12)

Actuarial gains and losses 1–6

Past service costs

– Unvested –(1)

– Vested –5

Curtailments and settlements (4) –

Termination benefits 32 47

Total costs for post-employment benefits other than pensions 550 590

1 Actuarial gains and losses are for each plan reported as income or expenses, when the accumulated amount exceed the so called corridor. The income or

expenses are then recognized over the expected average remaining service period of the employees.

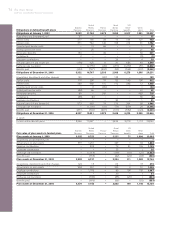

An increase of one percentage point per year in healthcare costs

would change the accumulated post-employment benefit obligation

as of December 31, 2004 by approximately 170, and the post-

employment benefit expense by approximately 15. A decrease of 1%

would decrease the accumulated value of obligations by about 145

and reduce costs by approximately 12.

Calculations made as of December 31, 2004 show an annual

increase of 10.0% in the weighted average per capita costs of

covered healthcare benefits; it is assumed that the percentage will

decline gradually to 5% and then remain at that level.