Volvo 2004 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2004 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

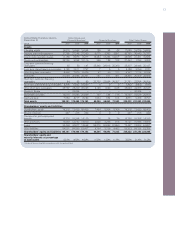

23

2004 compared with the year-earlier

period at a level of 27.1%. Volvo Trucks’

share of the market decreased to 15.2%

(15.7) and Renault Trucks’ share of the

market declined to 11.3% (11.4) in the

heavy-duty segment.

In North America, the Group’s com-

bined market share for heavy trucks

declined to 19.4% (19.8). Volvo Trucks’

market share amounted to 9.7% (9.4).

This increase was due to a high demand

for the new Volvo VN. Despite adding to

its leadership position in its core voca-

tional segments of construction and

refuse applications, Mack’s share of the

overall US retail market fell to 9.7% (10.4)

in 2004. This decline was due to the fact

that growth was disproportionately dom-

inated by the U.S. truck market’s long-

haul highway segment, which is not one

of Mack’s core segments.

In Brazil, Volvo’s market share was

unchanged at 13.1% (13.1).

Financial performance

Net sales for Volvo’s combined truck

operations amounted to SEK 136,879 M

in 2004. Adjusted for currency effects,

sales increased by 19.9% compared with

2003.

Operating income in 2004 amounted

to SEK 8,989 M (3,951). In Europe, Volvo

Trucks’ strong performance was further

enhanced and a considerable improve-

ment was recorded in markets outside

Europe. In North America both Mack

Trucks and Volvo Trucks showed signifi-

cant earnings improvements. Renault

Trucks also reported higher earnings. The

improvement in the truck operations was

largely attributable to higher sales vol-

umes and increased margins.

Production and investments

Production of trucks in 2004 amounted

to 97,300 Volvo Trucks (75,440), 60,755

Renault Trucks (52,400) and 25,637

Mack Trucks (18,519).

In 2004, the decision was taken to

optimize the industrial system within

Renault Trucks. Assembly of the Renault

Kerax will be relocated from Villaverde,

Spain to Bourg-en-Bresse, France, during

2006. The remaining activities in Villaverde

will be the manufacture of crankshafts.

A frame agreement was signed in

January 2004 between the Chinese com-

pany, Dong Feng Motors and Renault

Trucks that lays the foundation for a joint

venture.

In April 2004, Volvo Trucks opened the

assembly plant in Jinan, China together

with China National Heavy Truck Cor-

poration.

In September, the Group inaugurated a

new engine factory in Vénissieux, France,

for the assembly of 9 and 11 liter engines

and in October the Group announced

a comprehensive investment plan to

upgrade its existing engine and transmis-

sion plant in Hagerstown, USA, to supply

all business areas in the US with heavy

duty engines in the future.

Ambitions for 2005

The main focus in the truck sector will be

to manage the introduction and produc-

tion start of several new trucks within all

three truck brands. The high level of activ-

ity, in research and development on the

engine side, will also continue to prepare

for the launch of a new range that will

comply with the new emission standards

coming into force in Europe and North

America in 2006/2007. The focus on

developing stronger distribution networks

in Europe, North America and Asia will

continue. In production and purchasing,

the focus is on mitigating cost increases

on raw materials, balancing the effect of

currency fluctuation and on managing a

tight supply of certain parts and compon-

ents.