Volvo 2004 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2004 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

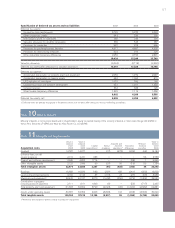

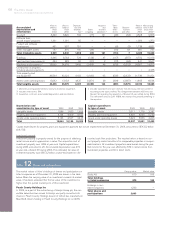

58 The Volvo Group

Notes to consolidated financial statements

production systems and software before 2001 was expensed as

incurred and in accordance with the transition rules no retroactive

application of RR 15 was made.

Warranty expenses

Estimated costs for product warranties are charged to operating

expenses when the products are sold. Estimated costs include both

expected contractual warranty obligations as well as expected good-

will warranty obligations. Estimated costs are determined based upon

historical statistics with consideration of known changes in product

quality, repair costs or similar. Costs for campaigns in connection

with specific quality problems are charged to operating expenses

when the campaign is decided and announced.

Restructuring costs

Restructuring costs are reported as a separate line item in the income

statement if they relate to a considerable change of the Group struc-

ture. Other restructuring costs are included in Other operating income

and expenses. A provision for decided restructuring measures is

reported when a detailed plan for the implementation of the measures

is complete and when this plan is communicated to those who are

affected.

Depreciation, amortization and impairments of tangible and

intangible non-current assets

Depreciation is based on the historical cost of the assets, adjusted in

appropriate cases by write-downs, and estimated useful lives.

Capitalized type-specific tools are generally depreciated over 2 to 8

years. The depreciation period for assets under operating leases is

normally 3 to 5 years. Machinery is generally depreciated over 5 to

20 years, and buildings over 25 to 50 years, while the greater part of

land improvements are depreciated over 20 years. In connection with

its participation in aircraft engine projects with other companies,

Volvo Aero in certain cases pays an entrance fee. These entrance

fees are capitalized and amortized over 5 to 10 years. Product and

software development is normally amortized over 3 to 8 years.

The difference between depreciation noted above and deprecia-

tion allowable for tax purposes is reported by the parent company

and in the individual Group companies as accumulated accelerated

depreciation, which is included in untaxed reserves. Consolidated

reporting of these items is described below under the heading

Deferred taxes, allocations and untaxed reserves.

Goodwill is included in intangible assets and amortized over its

estimated useful life. The amortization period is 5 to 20 years. The

goodwill amounts pertaining to Renault Trucks, Mack Trucks, Volvo

Construction Equipment, Champion Road Machinery, Volvo Aero

Services, Prévost, Nova BUS, Volvo Bus de Mexico, Volvo

Construction Equipment Korea, Volvo Aero Norge and Kommersiella

Fordon Europa are being amortized over 20 years due to the hold-

ings’ long-term and strategic importance.

If, at a balance sheet date, there is an indication that a tangible or

intangible non-current asset has been impaired, the recoverable

amount of the asset is estimated. If the recoverable amount is less

than the carrying amount, an impairment loss is recognized and the

carrying amount of the asset is reduced to the recoverable amount.

Inventories

Inventories are stated at the lower of cost, in accordance with the

first-in, first-out method (FIFO), or net realizable value.

Liquid funds

Liquid funds include cash and bank balances and marketable secur-

ities. Marketable securities are stated at the lower of cost or market

value in accordance with the portfolio method. Marketable securities

consist of interest-bearing securities, to some extent with maturities

exceeding three months. However, these securities have high liquid-

ity and can easily be converted to cash.

Post-employment benefits

Effective in 2003, Volvo has adopted RR 29 Employee benefits in

accounting for post-employment benefits. In accordance with RR 29,

actuarial calculations under the projected unit credit method should

be made for all defined benefit plans in order to determine the pres-

ent value of obligations for benefits vested by its current and former

employees. The actuarial calculations are being prepared annually

and are based upon actuarial assumptions that are determined close

to the balance sheet date each year. Changes in the present value of

obligations due to revised actuarial assumptions are treated as actu-

arial gains or losses which are amortized over the employees’ aver-

age remaining service period to the extent these exceed the corridor

value for each plan. Deviations between expected return on plan

assets and actual return are treated as actuarial gains or losses.

Provisions for post-employment benefits in Volvo’s balance sheet

correspond to the present value of obligations at year-end, less fair

value of plan assets, unrecognized actuarial gains or losses and

unrecognized unvested past service costs. Up to and including 2002,

defined benefit plans were accounted for in accordance with local

rules and directives in the respective country of Volvo’s subsidiaries.

For post-employment benefits that are financed through defined

contribution plans, Volvo’s annual contributions to such plans are

expensed as incurred. The accounting for defined contribution plans

has not been affected by the adoption of RR 29 in 2003.

By applying RR 29 all defined-benefit pension plans and health-

care benefit plans are accounted for by use of consistent principles,

in all the Group’s subsidiaries. In accordance with the transition rules

of the new standard, a transitional liability was established as at

January 1, 2003, determined in accordance with RR 29. This transi-

tional liability exceeded the liability recognized as per December 31,

2002, in accordance with earlier principles by approximately SEK 2.3

billion. The excess liability consequently was recognized as at

January 1, 2003, as an increase in provisions for pensions and other

post-employment benefits and a corresponding decrease in share-

holders’ equity. No additional deferred tax asset was recognized in

the Group’s balance sheet as at January 1, 2003, attributable to the

transition liability. In accordance with the transition rules of the new

standard, Volvo has not restated figures for earlier years in accord-

ance with the new accounting standard. Because the Group’s sub-

sidiaries up to 2002 have been applying local rules in each country,

the impact of adopting RR 29 as of 2003 differs for different coun-

tries of operations. Compared with earlier accounting principles in

Sweden, the adoption of RR 29 has mainly had the effect that plan

assets invested in Volvo’s Swedish pension foundation as from 2003

are accounted for at a long-term expected return instead of being

revalued each closing date to fair value. For Volvo’s subsidiaries in

the US, differences relate to accounting for past service costs and

the fact that RR 29 does not include rules about minimum liability

adjustments.

Provisions for residual value risks

Residual value risks are attributable to operational lease contracts

and sales transactions combined with buy-back agreements or residu-

al value guarantees. Residual value risks are the risks that Volvo in

the future would have to dispose used products at a loss if the price

development of these products is worse than what was expected

when the contracts were entered. Provisions for residual value risks

are made on a continuing basis based upon estimations of the used

products’ future net realizable values. The estimations of future net

realizable values are made with consideration of current prices,