Rogers 2011 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2011 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

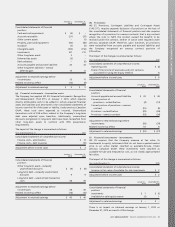

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Development expenditures are capitalized if they meet the

criteria for recognition as an asset. The assets are amortized over

their expected useful lives once they are available for use.

Research expenditures, as well as maintenance and training

costs, are expensed as incurred.

(r) Impairment:

(i) Goodwill and indefinite-life intangible assets:

The carrying values of identifiable intangible assets with

indefinite lives and goodwill are tested annually for impairment.

A cash generating unit (“CGU”) is the smallest identifiable group

of assets that generates cash inflows that are largely

independent of the cash inflows from other assets or groups of

assets. Goodwill and indefinite life intangible assets are

allocated to CGUs for the purpose of impairment testing based

on the level at which management monitors them, which is not

higher than an operating segment. The allocation is made to

those CGUs that are expected to benefit from the business

combination in which the goodwill arose.

(ii) Non-financial assets with finite useful lives:

The carrying values of non-financial assets with finite useful

lives, such as PP&E and intangible assets with finite useful lives,

are assessed for impairment whenever events or changes in

circumstances indicate that their carrying amounts may not be

recoverable. If any such indication exists, the recoverable

amount of the asset must be determined. Such assets are

impaired if their recoverable amount is lower than their carrying

amount. If it is not possible to estimate the recoverable amount

of an individual asset, the recoverable amount of the CGU to

which the asset belongs is tested for impairment.

(iii) Recognition of impairment charge:

The recoverable amount is the higher of an asset’s or CGU’s fair

value less costs to sell or its value in use. If the recoverable

amount of an asset or CGU is estimated to be less than its

carrying amount, the carrying amount of the asset or CGU is

reduced to its recoverable amount. The resulting impairment loss

is recognized in the consolidated statements of income. An

impairment loss is reversed if there has been a change in the

estimates used to determine the recoverable amount. When an

impairment loss is subsequently reversed, the carrying amount of

the asset or CGU is increased to the revised estimate of its

recoverable amount so that the increased carrying amount does

not exceed the carrying amount that would have been recorded

had no impairment losses been recognized for the asset or CGU

in prior years. Impairment losses recognized for goodwill are not

reversed.

In assessing value in use, the estimated future cash flows are

discounted to their present value using a pre-tax rate that

reflects current market assessments of the time value of money

and the risks specific to that asset. The cash flows used reflect

management assumptions and are supported by external sources

of information.

(s) Use of estimates:

The preparation of financial statements requires management to

make judgements, estimates and assumptions that affect the

application of accounting policies and the reported amounts of

assets, liabilities, revenue and expenses. Actual results could differ

from these estimates.

Key areas of estimation, where management has made difficult,

complex or subjective judgements, often as a result of matters that

are inherently uncertain are as follows:

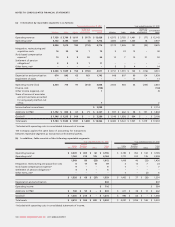

(i) Business combinations:

The amount of goodwill initially recognized as a result of a

business combination and the determination of the fair value of

the identifiable assets acquired and the liabilities assumed is

based, to a considerable extent, on management’s judgement.

(ii) Income taxes:

Income tax liabilities must be estimated for the Company,

including an assessment of temporary differences. Any

temporary differences will generally result in the recognition of

deferred tax assets and liabilities in the financial statements.

Management’s judgement is required for the calculation of

current and deferred taxes.

(iii) Property, plant and equipment:

Measurement of PP&E involves the use of estimates for

determining the expected useful lives of depreciable assets.

Management’s judgement is also required to determine

depreciation methods and an asset’s residual value, the rate of

capitalization of internal labour costs and whether an asset is a

qualifying asset for the purposes of capitalizing borrowing costs.

(iv) Impairment of non-financial assets:

The impairment test on CGUs is carried out by comparing the

carrying amount of CGUs and their recoverable amount. The

recoverable amount of a CGU is the higher of its fair value, less

costs to sell and its value in use. This complex valuation process

used to determine fair value less costs to sell and/or value in use

entails the use of methods such as the discounted cash flow

method which uses assumptions to estimate cash flows. The

recoverable amount depends significantly on the discount rate

used in the discounted cash flow model as well as the expected

future cash flows.

(v) Provisions:

Considerable judgement is used in measuring and recognizing

provisions and the exposure to contingent liabilities. Judgement

is necessary to determine the likelihood that a pending litigation

or other claim will succeed, or a liability will arise and to

quantify the possible range of the final settlement.

(vi) Financial risk management and financial instruments:

The fair value of derivative instruments, investments in publicly

traded and private companies, and equity instruments is

determined on the basis of either prices in regulated markets or

quoted prices provided by financial counterparties, or using

valuation models which also take into account subjective

measurements such as, cash flow estimates or expected volatility

of prices.

(vii) Pensions:

Pension benefit costs are determined in accordance with

actuarial valuations, which rely on assumptions including

discount rates, life expectancies and expected return on plan

assets. In the event that changes in assumptions are required

with respect to discount rates and expected returns on invested

assets, the future amounts of the pension benefit cost may be

affected materially.

(viii) Stock options, share units and share purchase plans:

Assumptions, such as volatility, expected life of an award, risk-

free interest rate, forfeiture rate, and dividend yield, are used in

the underlying calculation of fair values of the Company’s stock

options. Fair value is determined using the Company’s Class B

Non-Voting share price, and the Black-Scholes or trinomial

option pricing models, depending on the nature of the share

based award. Details of the assumptions used are included in

note 22.

Significant changes in the assumptions, including those with respect

to future business plans and cash flows, could materially change the

recorded carrying amounts.

90 ROGERS COMMUNICATIONS INC. 2011 ANNUAL REPORT