Rogers 2011 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2011 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS

increasingly fast tiers of Internet services, and telephony services.

These investments have enabled cable television companies to offer

increased speed and quality of service in their expanded digital

television packages, PVR, HDTV programming, higher speed Internet

and telephony services.

Increased Competition from Alternative Broadcasting Distribution

Undertakings

As fully described in the section entitled “Competition in our

Businesses”, Canadian cable television systems generally face legal

and illegal competition from several alternative multi-channel

broadcasting distribution systems.

Growth of Internet Protocol-Based Services

The availability of telephony over the Internet has become a direct

competitor to Canadian cable television systems. Voice-over-Internet

Protocol (“VoIP”) local services are being provided by non-facilities-

based providers, such as Skype and Vonage, who market VoIP local

services to the subscribers of local exchange carriers (“ILEC”), cable

and other companies’ high-speed Internet services. In addition and as

discussed below, certain television and movie content is increasingly

becoming available over the Internet. Traditional TV viewing has

been increasingly augmented by these and other emerging options

available to consumers such as over-the-top television (such as Apple

TV), online video offerings (such as Netflix) and Mobile TV.

In the enterprise market, there is a continuing shift to IP-based

services, in particular from asynchronous transfer mode (“ATM”) and

frame relay (two common legacy data networking technologies) to IP

delivered through virtual private networking (“VPN”) services. This

transition results in lower costs for both users and carriers.

Increasing Availability of Online Access to Cable TV Content

Cable and content providers in the U.S. and Canada continue to

create platforms and portals which provide for online access to

certain television content via broadband Internet connections instead

of traditional cable television access. These platforms, including one

launched in late 2009 by Cable called Rogers On Demand Online,

generally provide authentication features, which control and limit

access to content that is subscribed to at the user’s residence. The

launch and development of these online content platforms are in the

early stages and are subject to ongoing discussions between content

providers and cable companies with respect to how access to televised

and on-demand content is granted, controlled and monetized.

Facilities-Based Telephony Services Competitors

Competition has been ongoing for a number of years in the long-

distance telephony service markets with the average price per minute

continuing to decline year-over-year. Competition in the local

telephone market also continues between Cable, ILECs and various

VoIP providers.

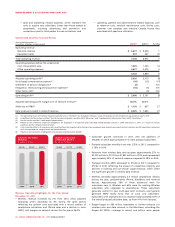

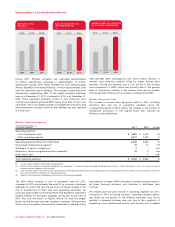

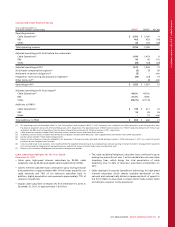

CABLE OPERATING AND FINANCIAL RESULTS

For purposes of this discussion, revenue has been classified according

to the following categories:

• Cable, which includes revenue derived from:

• analog cable service, consisting of basic cable service fees plus

extended basic (or tier) service fees, and access fees for use of

channel capacity by third and related parties; and

• digital cable service revenue, consisting of digital channel service

fees, including premium and specialty service subscription fees,

PPV service fees, VOD service fees, and revenue earned on the

sale and rental of digital cable set-top terminals;

• Internet, which includes monthly and additional use service

revenues from residential and small business Internet access service

and modem sale and rental fees;

• Home Phone, which includes revenues from residential and small

business local telephony service, calling features such as voice mail

and call-waiting, and long-distance;

• RBS, which includes telephony and data services revenue from

enterprise and government customers, as well as the sale of these

offerings on a wholesale basis to other telecommunications

carriers; and

• Video, which includes the sale and rental of DVDs and video

games.

Cable’s operating expenses are segregated into the following

categories for assessing business performance:

• Cost of equipment sales, which is comprised of cable equipment

costs; and

• Other operating expenses, which include all other expenses

incurred to operate the business on a day-to-day basis, service

existing subscriber relationships, as well as attract new subscribers.

These include:

• merchandise for resale, such as Video store merchandise and

depreciation of Video DVD and game rental assets;

• employee salaries and benefits, such as remuneration, bonuses,

pension, employee benefits and stock-based compensation; and

• other external purchases, such as:

• service costs, which includes the following:

• the monthly contracted payments for the acquisition of

programming paid directly to the programming suppliers,

copyright collectives and the Canadian Programming

Production Funds;

• Internet interconnectivity and usage charges and the cost

of operating Cable’s Internet service; and

• Inter-carrier payments for interconnection to the local

access and long-distance carriers related to cable and

circuit-switched telephony service;

• sales and marketing related expenses, which represent the

costs to acquire new subscribers, including advertising and

promotion, and commissions paid to third parties; and

• operating, general and administrative related expenses,

which includes the following:

• technical service expenses, which include the costs

of operating and maintaining cable networks as

well as certain customer service activities, such as

installations and repair;

• customer care expenses, which include the costs

associated with customer order-taking and billing

inquiries;

• community television expenses, which consist of

the costs to operate a series of local community-

based television stations per regulatory

requirements in Cable’s licenced systems;

• expenses related to the corporate management of

Video; and

• facility costs and other general and administrative

expenses.

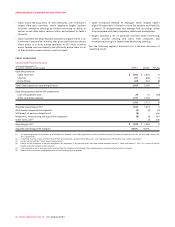

In the cable industry in Canada, the demand for services, particularly

Internet, digital television and cable telephony services, continues to

grow and the variable costs associated with this growth, such as the

cost of content, commissions for subscriber activations, as well as the

fixed costs of acquiring new subscribers, are material. As such,

fluctuations in the number of activations of new subscribers from

period-to-period result in fluctuations in sales, marketing, cost of sales

and field services expenses.

34 ROGERS COMMUNICATIONS INC. 2011 ANNUAL REPORT