MoneyGram 2013 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2013 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

Table of Contents

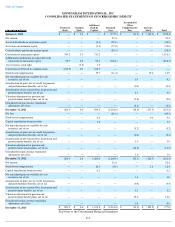

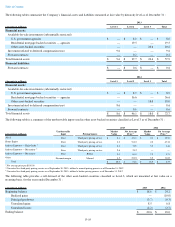

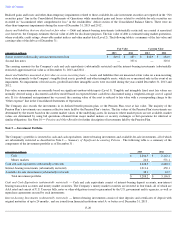

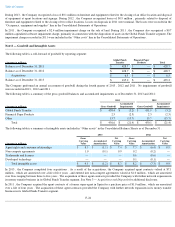

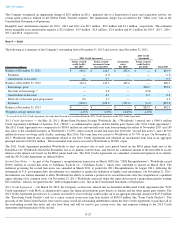

Assets and liabilities that are measured at fair value on a recurring basis

—

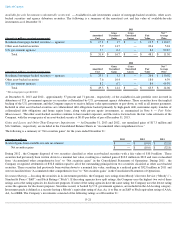

For other asset–

backed securities and investments in limited partnerships, market quotes are generally not available. If available, the

Company will utilize a fair value measurement from a pricing service. The pricing service utilizes a pricing model based on market

observable data and indices, such as quotes for comparable securities, yield curves, default indices, interest rates and historical

prepayment speeds. If a fair value measurement is not available from the pricing service, the Company will utilize a broker quote, if

available. Because the inputs and assumptions that brokers use to develop prices are unknown, most valuations that are based on

brokers' quotes are classified as Level 3. If no broker quote is available, or if such quote cannot be corroborated by market data or

internal valuations, the Company may perform internal valuations utilizing externally developed cash flow models. These pricing

models are based on market observable spreads and, when available, observable market indices. The pricing models also use inputs

such as the rate of future prepayments and expected default rates on the principal, which are derived by the Company based on the

characteristics of the underlying structure and historical prepayment speeds experienced at the interest rate levels projected for the

underlying collateral. The pricing models for certain asset-backed securities also include significant non-

observable inputs such as

internally assessed credit ratings for non-

rated securities combined with externally provided credit spreads. Observability of market

inputs to the valuation models used for pricing certain of the Company's investments has deteriorated with the disruption to the credit

markets as overall liquidity and trading activity in these sectors has been substantially reduced. Accordingly, securities valued using a

pricing model are classified as Level 3 financial instruments.

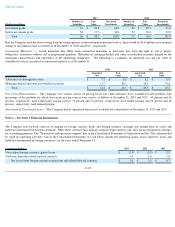

F-18

•

Available

-for-sale investments — For U.S. government agencies and residential mortgage-

backed securities collateralized by U.S.

government agency securities, fair value measures are generally obtained from independent sources, including a pricing service.

Because market quotes are generally not readily available or accessible for these specific securities, the pricing service generally

measures fair value through the use of pricing models and observable inputs for similar assets and market data. Accordingly, these

securities are classified as Level 2 financial instruments. The Company periodically corroborates the valuations provided by the pricing

service through internal valuations utilizing externally developed cash flow models, comparison to actual transaction prices for any sold

securities and any broker quotes received on the same security.

•

Derivative financial instruments

—

Derivatives consist of forward contracts to manage income statement exposure to foreign currency

exchange risk arising from the Company’s assets and liabilities denominated in foreign currencies. The Company’

s forward contracts

are well-established products, allowing the use of standardized models with market-

based inputs. These models do not contain a high

level of subjectivity and the inputs are readily observable. Accordingly, the Company has classified its forward contracts as Level 2

financial instruments. See Note 6 — Derivative Financial Instruments for additional disclosure on the Company's forward contracts.

•

Deferred compensation

—

The assets associated with the deferred compensation plan that are funded through voluntary contributions

by the Company consist of investments in money market securities and mutual funds. These investments were classified as Level 1 as

there are quoted market prices for these funds.