MetLife 2004 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2004 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

|

|

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

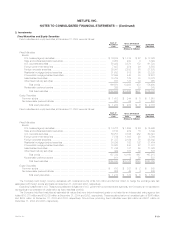

Liability for Future Policy Benefits and Policyholder Account Balances

Future policy benefit liabilities for participating traditional life insurance policies are equal to the aggregate of (i) net level premium reserves for death

and endowment policy benefits (calculated based upon the non-forfeiture interest rate, ranging from 3% to 11%, and mortality rates guaranteed in

calculating the cash surrender values described in such contracts), (ii) the liability for terminal dividends, and (iii) premium deficiency reserves, which are

established when the liabilities for future policy benefits plus the present value of expected future gross premiums are insufficient to provide for expected

future policy benefits and expenses after DAC is written off. Future policy benefits for non-participating traditional life insurance policies are equal to the

aggregate of (i) the present value of future benefit payments and related expenses less the present value of future net premiums and (ii) premium

deficiency reserves. Assumptions as to mortality and persistency are based upon the Company’s experience when the basis of the liability is established.

Interest rates for the aggregate future policy benefit liabilities range from 5.0% to 6.5%.

Participating business represented approximately 14% and 14% of the Company’s life insurance in-force, and 56% and 57% of the number of life

insurance policies in-force, at December 31, 2004 and 2003, respectively. Participating policies represented approximately 35% and 34%, 38% and

38%, and 39% and 41% of gross and net life insurance premiums for the years ended December 31, 2004, 2003 and 2002, respectively. The

percentages indicated are calculated excluding the business of the Reinsurance segment.

Future policy benefit liabilities for individual and group traditional fixed annuities after annuitization are equal to the present value of expected future

payments and premium deficiency reserves. Interest rates used in establishing such liabilities range from 2% to 11%.

Future policy benefit liabilities for non-medical health insurance are calculated using the net level premium method and assumptions as to future

morbidity, withdrawals and interest, which provide a margin for adverse deviation. Interest rates used in establishing such liabilities range from 2% to 11%.

Future policy benefit liabilities for disabled lives are estimated using the present value of benefits method and experience assumptions as to claim

terminations, expenses and interest. Interest rates used in establishing such liabilities range from 3% to 11%.

Liabilities for unpaid claims and claim expenses for property and casualty insurance are included in future policyholder benefits and are estimated

based upon the Company’s historical experience and other actuarial assumptions that consider the effects of current developments, anticipated trends

and risk management programs, reduced for anticipated salvage and subrogation. The effects of changes in such estimated liabilities are included in the

results of operations in the period in which the changes occur.

Policyholder account balances relate to investment-type contracts and universal life-type policies. Investment-type contracts principally include

traditional individual fixed annuities in the accumulation phase and non-variable group annuity contracts. Policyholder account balances are equal to the

policy account values, which consist of an accumulation of gross premium payments plus credited interest, ranging from 1% to 13%, less expenses,

mortality charges, and withdrawals.

The Company issues fixed and floating rate obligations under its guaranteed investment contract (‘‘GIC’’) program. During the years ended

December 31, 2004, 2003 and 2002, the Company issued $3,941 million, $4,341 million and $500 million, respectively, in such obligations. There have

been no repayments of any of the contracts. Accordingly, the GICs outstanding, which are included in policyholder account balances in the

accompanying consolidated balance sheets, were $8,978 and $4,862, respectively, at December 31, 2004 and 2003. Interest credited on the

contracts for the years ended December 31, 2004, 2003 and 2002 was $139 million, $56 million and $12 million, respectively.

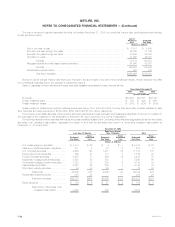

The Company establishes liabilities for minimum death and income benefit guarantees relating to certain annuity contracts and secondary and paid

up guarantees relating to certain life policies. Annuity guaranteed death benefit liabilities are determined by estimating the expected value of death

benefits in excess of the projected account balance and recognizing the excess ratably over the accumulation period based on total expected

assessments. The Company regularly evaluates estimates used and adjusts the additional liability balance, with a related charge or credit to benefit

expense, if actual experience or other evidence suggests that earlier assumptions should be revised. The assumptions used in estimating the liabilities

are consistent with those used for amortizing DAC, including the mean reversion assumption. The assumptions of investment performance and volatility

are consistent with the historical experience of the Standard & Poor’s 500 Index (‘‘S&P’’). The benefits used in calculating the liabilities are based on the

average benefits payable over a range of scenarios.

Guaranteed annuitization benefit liabilities are determined by estimating the expected value of the annuitization benefits in excess of the projected

account balance at the date of annuitization and recognizing the excess ratably over the accumulation period based on total expected assessments. The

Company regularly evaluates estimates used and adjusts the additional liability balance, with a related charge or credit to benefit expense, if actual

experience or other evidence suggests that earlier assumptions should be revised. The assumptions used for calculating such guaranteed annuitization

benefit liabilities are consistent with those used for calculating the guaranteed death benefit liabilities. In addition, the calculation of guaranteed

annuitization benefit liabilities incorporates a percentage of the potential annuitizations that may be elected by the contractholder.

Liabilities for universal and variable life secondary guarantees and paid-up guarantees are determined by estimating the expected value of death

benefits payable when the account balance is projected to be zero and recognizing those benefits ratably over the accumulation period based on total

expected assessments. The Company regularly evaluates estimates used and adjusts the additional liability balances, with a related charge or credit to

benefit expense, if actual experience or other evidence suggests that earlier assumptions should be revised. The assumptions used in estimating the

secondary and paid up guarantee liabilities are consistent with those used for amortizing DAC. The assumptions of investment performance and volatility

for variable products are consistent with historical S&P experience. The benefits used in calculating the liabilities are based on the average benefits

payable over a range of scenarios.

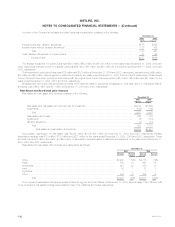

Recognition of Insurance Revenue and Related Benefits

Premiums related to traditional life and annuity policies with life contingencies are recognized as revenues when due. Benefits and expenses are

provided against such revenues to recognize profits over the estimated lives of the policies. When premiums are due over a significantly shorter period

than the period over which benefits are provided, any excess profit is deferred and recognized into operations in a constant relationship to insurance in-

force or, for annuities, the amount of expected future policy benefit payments.

Premiums related to non-medical health and disability contracts are recognized on a pro rata basis over the applicable contract term.

Deposits related to universal life-type and investment-type products are credited to policyholder account balances. Revenues from such contracts

consist of amounts assessed against policyholder account balances for mortality, policy administration and surrender charges and are recognized in the

MetLife, Inc.

F-14