MetLife 2004 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2004 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

|

|

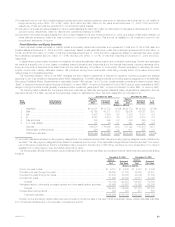

Commercial Mortgage Loans. The Company diversifies its commercial mortgage loans by both geographic region and property type. The following

table presents the distribution across geographic regions and property types for commercial mortgage loans at:

December 31, 2004 December 31, 2003

Carrying % of Carrying % of

Value Total Value Total

(Dollars in millions)

Region

South Atlantic******************************************************************* $ 5,696 22.8% $ 4,978 24.5%

Pacific ************************************************************************* 6,075 24.3 5,005 24.7

Middle Atlantic ****************************************************************** 4,057 16.2 3,455 17.0

East North Central *************************************************************** 2,550 10.2 1,821 9.0

New England ******************************************************************* 1,412 5.6 1,278 6.3

West South Central ************************************************************** 2,024 8.1 1,370 6.8

Mountain*********************************************************************** 778 3.1 740 3.6

West North Central ************************************************************** 667 2.7 619 3.0

International ******************************************************************** 1,364 5.5 836 4.1

East South Central ************************************************************** 268 1.1 198 1.0

Other************************************************************************** 99 0.4 — —

Total******************************************************************* $24,990 100.0% $20,300 100.0%

Property Type

Office ************************************************************************* $11,500 46.0% $ 9,170 45.2%

Retail ************************************************************************** 5,698 22.8 5,006 24.7

Apartments ********************************************************************* 3,264 13.1 2,832 13.9

Industrial *********************************************************************** 2,499 10.0 1,911 9.4

Hotel ************************************************************************** 1,245 5.0 1,032 5.1

Other************************************************************************** 784 3.1 349 1.7

Total******************************************************************* $24,990 100.0% $20,300 100.0%

The following table presents the scheduled maturities for the Company’s commercial mortgage loans at:

December 31, 2004 December 31, 2003

Carrying % of Carrying % of

Value Total Value Total

(Dollars in millions)

Due in one year or less ********************************************************** $ 939 3.7% $ 708 3.5%

Due after one year through two years*********************************************** 1,800 7.2 1,065 5.2

Due after two years through three years********************************************* 2,372 9.5 2,020 10.0

Due after three years through four years********************************************* 2,943 11.8 2,362 11.6

Due after four years through five years ********************************************** 4,578 18.3 3,157 15.6

Due after five years ************************************************************** 12,358 49.5 10,988 54.1

Total******************************************************************* $24,990 100.0% $20,300 100.0%

Restructured, Potentially Delinquent, Delinquent or Under Foreclosure. The Company monitors its mortgage loan investments on an ongoing basis,

including reviewing loans that are restructured, potentially delinquent, delinquent or under foreclosure. These loan classifications are consistent with those

used in industry practice.

The Company defines restructured mortgage loans as loans in which the Company, for economic or legal reasons related to the debtor’s financial

difficulties, grants a concession to the debtor that it would not otherwise consider. The Company defines potentially delinquent loans as loans that, in

management’s opinion, have a high probability of becoming delinquent. The Company defines delinquent mortgage loans, consistent with industry

practice, as loans in which two or more interest or principal payments are past due. The Company defines mortgage loans under foreclosure as loans in

which foreclosure proceedings have formally commenced.

The Company reviews all mortgage loans on an ongoing basis. These reviews may include an analysis of the property financial statements and rent

roll, lease rollover analysis, property inspections, market analysis and tenant creditworthiness.

The Company records valuation allowances for loans that it deems impaired. The Company’s valuation allowances are established both on a loan

specific basis for those loans where a property or market specific risk has been identified that could likely result in a future default, as well as for pools of

loans with similar high risk characteristics where a property specific or market risk has not been identified. Such valuation allowances are established for

the excess carrying value of the mortgage loan over the present value of expected future cash flows discounted at the loan’s original effective interest

rate, the value of the loan’s collateral or the loan’s market value if the loan is being sold. The Company records valuation allowances as investment losses.

The Company records subsequent adjustments to allowances as investment gains (losses).

MetLife, Inc. 33