Lenovo 2010 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2010 Lenovo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

2009/10 Annual Report Lenovo Group Limited

64

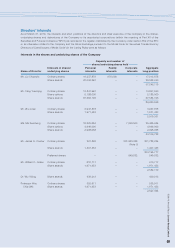

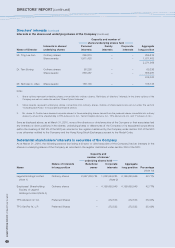

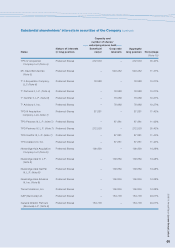

DIRECTORS’ REPORT (continued)

64

Defined benefit pensions plans (continued)

Japan – Pension Plan

The Company operates a hybrid plan that consists of a defined contribution up to the annual tax-deductible limit (Yen 306,000)

plus a cash balance plan with contributions of 7% of pay. The plan is funded by company contributions to a qualified pension

fund, which is held for the sole benefit of participants and beneficiaries.

For the year ended March 31, 2010, an amount of Yen 390,489,759 was charged to the income statement with respect to this

plan.

The principal results of the most recent actuarial valuation of the plan at March 31, 2010 were the following:

• The actuarial valuation was prepared by JP Actuary Consulting Co., Ltd. The actuaries involved are fully qualified under

the requirements of Japanese law.

• The actuarial method used was the Projected Unit Credit Cost method and the principal actuarial assumptions were:

– Discount rate: 2.25%

– Expected return on plan assets: 3.25%

– Future salary increases: Age-group based

• The plan was 65% funded at the actuarial valuation date.

• There was a deficit of Yen 3,011,088,702 under this plan at the actuarial valuation date.

Germany – Pension Plan

The Company operates a hybrid plan that provides a defined contribution for some participants and a final pay defined benefit

for other participants, depending on which former IBM plan they were in.

Employees hired by IBM before January 1, 1992 have a defined benefit based on a final pay formula. Employees hired from

1992 to 1999 have a combination of a defined benefit based on a final pay formula and a defined contribution plan with

employee required contributions of 7% of pay above the social security ceiling and a 100% company match. Employees hired in

or after 2000 have a combination of a cash balance plan with an employer contribution of 2.95% of pay below the social security

ceiling, and a voluntary defined contribution plan where employees can contribute specific amounts through salary sacrifice.

The plan is partially funded by company and employee contributions to an insured support fund with DBV-Winterthur up to the

maximum tax-deductible limits. In line with standard practice in Germany, the remainder is unfunded (book reserve).

For the year ended March 31, 2010, an amount of EUROS 1,546,000 was charged to the income statement with respect to this

plan.

The principal results of the most actuarial valuation of the plan at March 31, 2010 were the following:

• The actuarial valuation was prepared by Kern, Mauch & Kollegen. The actuaries involved are fully qualified under German

law.

• The actuarial method used was the Projected Unit Credit Cost method and the principal actuarial assumptions were:

– Discount rate: 4.00%

– Future salary increases: 2.20%

– Future pension increases: 1.75%

• The plan was 63% funded at the actuarial valuation date.

• There was a deficit of EUROS 8,296,000 under this plan at the actuarial valuation date.