IBM 2007 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2007 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

70

Notes to Consolidated Financial Statements

International Business Machines Corporation and Subsidiary Companies

Management Discussion ..................................14

Consolidated Statements ..................................58

Notes ........................................................... 64

A-F ............................................................. 64

A. Significant Accounting Policies ............ 64

B. Accounting Changes ...................................73

C. Acquisitions/Divestitures ............................76

D. Financial Instruments

(excluding derivatives).................................82

E. Inventories ...................................................83

F. Financing Receivables .................................83

G-M ..................................................................84

N-S ...................................................................94

T-W ................................................................102

expected to be paid upon retirement based on estimated future com-

pensation levels. For the nonpension postretirement benefit plans,

the benefit obligation is the accumulated postretirement benefit

obligation (APBO), which represents the actuarial present value of

postretirement benefits attributed to employee services already ren-

dered. The fair value of plan assets represents the current market

value of cumulative company and participant contributions made to

an irrevocable trust fund, held for the sole benefit of participants,

which are invested by the trust fund. Overfunded plans, with the fair

value of plan assets exceeding the benefit obligation, are aggregated

and recorded as a Prepaid pension asset equal to this excess.

Underfunded plans, with the benefit obligation exceeding the fair

value of plan assets, are aggregated and recorded as a Retirement and

nonpension postretirement benefit obligation equal to this excess.

The current portion of the Retirement and nonpension postre-

tirement benefit obligations represents the actuarial present value of

benefits payable in the next 12 months exceeding the fair value of

plan assets, measured on a plan-by-plan basis. This obligation is

recorded in Compensation and benefits in the Consolidated

Statement of Financial Position.

Net periodic pension and nonpension postretirement benefit cost/

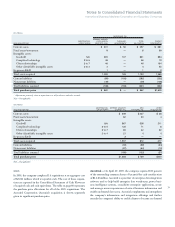

(income) is recorded in the Consolidated Statement of Earnings and

includes service cost, interest cost, expected return on plan assets,

amortization of prior service costs/(credits) and (gains)/losses previ-

ously recognized as a component of Gains and (losses) not affecting

retained earnings and amortization of the net transition asset remaining

in Accumulated gains and (losses) not affecting retained earnings.

Service cost represents the actuarial present value of participant ben-

efits earned in the current year. Interest cost represents the time value

of money cost associated with the passage of time. Certain events,

such as changes in employee base, plan amendments and changes in

actuarial assumptions, result in a change in the benefit obligation and

the corresponding change in the Gains and (losses) not affecting

retained earnings. The result of these events is amortized as a com-

ponent of net periodic cost/(income) over the service lives of the

participants, provided such amounts exceed thresholds which are

based upon the benefit obligation or the value of plan assets. The

average service lives of the participants in the IBM Personal Pension

Plan, a U.S. defined benefit pension plan, currently approximates 10

years and varies for participants in non-U.S. plans. Net periodic cost/

(income) is recorded in Cost, SG&A and RD&E in the Consolidated

Statement of Earnings based on the employees’ respective function.

(Gains)/losses and prior service costs/(credits) not recognized as

a component of net periodic cost/(income) in the Consolidated

Statement of Earnings as they arise are recognized as a component of

Gains and (losses) not affecting retained earnings in the Consolidated

Statement of Stockholders’ Equity, net of tax. Those (gains)/losses

and prior service costs/(credits) are subsequently recognized as a com-

ponent of net periodic cost/(income) pursuant to the recognition and

amortization provisions of applicable accounting standards. (Gains)/

losses arise as a result of differences between actual experience and

assumptions or as a result of changes in actuarial assumptions. Prior

service costs/(credits) represent the cost of benefit improvements

attributable to prior service granted in plan amendments.

The measurement of benefit obligations and net periodic cost/

(income) is provided by third-party actuaries based on estimates

and assumptions approved by the company’s management. These

valuations reflect the terms of the plans and use participant-specific

information such as compensation, age and years of service, as well as

certain assumptions, including estimates of discount rates, expected

return on plan assets, rate of compensation increases, interest credit-

ing rates and mortality rates.

Defined Contribution Plans

The company records expense for defined contribution plans for the

company’s contribution when the employee renders service to the com-

pany, essentially coinciding with the cash contributions to the plans.

The expense is recorded in Cost, SG&A and RD&E in the Consolidated

Statement of Earnings based on the employees’ respective function.

Stock-Based Compensation

Stock-based compensation represents the cost related to stock-based

awards granted to employees. The company measures stock-based

compensation cost at grant date, based on the estimated fair value of

the award and recognizes the cost on a straight-line basis (net of

estimated forfeitures) over the employee requisite service period.

The company estimates the fair value of stock options using a Black-

Scholes valuation model. The cost is recorded in Cost, SG&A, and

RD&E in the Consolidated Statement of Earnings based on the

employees’ respective function.

The company records deferred tax assets for awards that result in

deductions on the company’s income tax returns, based on the

amount of compensation cost recognized and the statutory tax rate in

the jurisdiction in which it will receive a deduction. Differences

between the deferred tax assets recognized for financial reporting

purposes and the actual tax deduction reported on the income tax

return are recorded in Additional Paid-In Capital (if the tax deduc-

tion exceeds the deferred tax asset) or in the Consolidated Statement

of Earnings (if the deferred tax asset exceeds the tax deduction and

no additional paid-in capital exists from previous awards).

See note T, “Stock-Based Compensation,” on pages 102 to 105

for additional information.