HP 2013 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2013 HP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

HEWLETT-PACKARD COMPANY AND SUBSIDIARIES

Management’s Discussion and Analysis of

Financial Condition and Results of Operations (Continued)

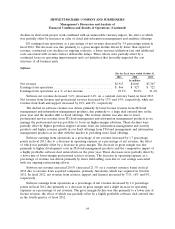

Our debt-equity ratio is calculated as the carrying value of debt divided by the carrying value of

equity. Our debt-equity ratio decreased by 0.43x in fiscal 2013, due to a decrease in total debt balances

of $5.8 billion coupled with an increase in stockholders equity by $4.8 billion at the end of fiscal 2013.

Our debt-equity ratio increased by 0.46x in fiscal 2012, due primarily to a decrease in stockholders

equity of $16.2 billion at the end of fiscal 2012.

Our weighted-average interest rate reflects the average effective rate on our borrowings prevailing

during the period and reflects the impact of interest rate swaps. For more information on our interest

rate swaps, see Note 9 to the Consolidated Financial Statements in Item 8, which is incorporated

herein by reference.

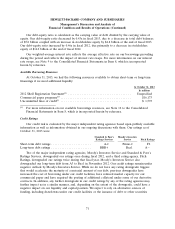

Available Borrowing Resources

At October 31, 2013, we had the following resources available to obtain short-term or long-term

financings if we need additional liquidity:

At October 31, 2013

In millions

2012 Shelf Registration Statement(1) .................................... Unspecified

Commercial paper programs(1) ........................................ $16,173

Uncommitted lines of credit(1) ........................................ $ 1,593

(1) For more information on our available borrowings resources, see Note 12 to the Consolidated

Financial Statements in Item 8, which is incorporated herein by reference.

Credit Ratings

Our credit risk is evaluated by the major independent rating agencies based upon publicly available

information as well as information obtained in our ongoing discussions with them. Our ratings as of

October 31, 2013 were:

Standard & Poor’s Moody’s Investors

Ratings Services Service Fitch Ratings

Short-term debt ratings ....................... A-2 Prime-2 F2

Long-term debt ratings ....................... BBB+ Baa1 Aǁ

Two of the major independent rating agencies, Moody’s Investors Service and Standard & Poor’s

Ratings Services, downgraded our ratings once during fiscal 2012, and a third rating agency, Fitch

Ratings, downgraded our ratings twice during that fiscal year. Moody’s Investors Service also

downgraded our long-term debt from A3 to Baa1 in November 2012. Our credit ratings remain under

negative outlook by Moody’s Investors Service. While we do not have any rating downgrade triggers

that would accelerate the maturity of a material amount of our debt, previous downgrades have

increased the cost of borrowing under our credit facilities, have reduced market capacity for our

commercial paper and have required the posting of additional collateral under some of our derivative

contracts. In addition, any further downgrade in our credit ratings by any of the rating agencies may

further impact us in a similar manner, and, depending on the extent of the downgrade, could have a

negative impact on our liquidity and capital position. We expect to rely on alternative sources of

funding, including drawdowns under our credit facilities or the issuance of debt or other securities

71