HP 2013 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2013 HP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

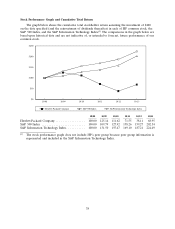

HEWLETT-PACKARD COMPANY AND SUBSIDIARIES

Management’s Discussion and Analysis of

Financial Condition and Results of Operations (Continued)

Our business continues to produce significant cash flow from operations, generating $11.6 billion in

fiscal 2013. During the year, we repaid $5.7 billion of debt, returned $1.1 billion to stockholders

through dividends and repurchased $1.5 billion worth of common stock. In addition, we purchased

$3.2 billion in capital assets. We ended fiscal 2013 with an investment portfolio of $12.5 billion,

consisting of cash and cash equivalents and short-term and long-term investments, which was an

increase of approximately $800 million from the end of fiscal 2012.

We entered fiscal 2013 having experienced a multi-quarter decline in revenue and operating

margins. That decline in financial performance reflected a series of challenges that were facing our

business. Some of those challenges related to structural and execution issues, such as aligning costs to

our revenue trajectory, addressing the need to rationalize our R&D investments and reinvest in IT

systems, and rebuilding our channel partner relationships. Other challenges related to dynamic market

trends, such as the growth of mobility, the increasing demand for hyperscale computing infrastructure,

the shift to software-as-a-service (‘‘SaaS’’), the transition towards cloud computing, and aggressive

pricing conditions. We also confronted a series of significant macroeconomic challenges in fiscal 2013,

such as a shift in consumer spending, weak demand in the SMB and enterprise sectors in Europe, and

declining growth in some emerging markets.

During fiscal 2013, we continued to address these challenges by driving innovation across the

company, improving operations, aligning our cost structure and rebuilding our balance sheet. As a

result of these efforts, revenue declines have begun to moderate as we reap the early benefits of our

investments in product innovation, as decreasing costs driven by our restructuring efforts have begun to

align to our revenue trajectory, as our enterprise services business has begun to become more

predictable, and as our business performance has begun to improve in our printing business due to our

focus on key initiatives such as Ink in the Office, Managed Print Services and Ink Advantage. In

addition, we made investments targeted at our channel partner relationships through improvements in

sales force and channel partner deal pricing tools and reporting infrastructure. Our strong cash flows

from operations in fiscal 2013 also have allowed us to further reduce our debt.

As we enter fiscal 2014, we continue to experience challenges that represent trends and

uncertainties that may affect our business and results of operations. One set of challenges relates to

continuing dynamic and accelerating market trends, such as the decline in the PC market, the growth

of multi-architecture devices running competing operating systems, the market shift towards tablets

within mobility, the market shift to cloud-related infrastructure, software, and services, and the growth

in SaaS business models. Another set of challenges relates to changes in the competitive landscape.

Our major competitors are expanding their product and service offerings with integrated products and

solutions, our business-specific competitors are exerting increased competitive pressure in targeted

areas and are going after new markets, our emerging competitors are introducing new technologies and

business models, and our alliance partners in some businesses are increasingly becoming our

competitors in others. A third set of challenges relates to business model and go-to-market execution.

In addition, we are continuing to experience macroeconomic weakness across many geographic regions,

particularly in Europe, the Middle East and Africa (‘‘EMEA’’), China and other high-growth markets.

A discussion of some of these challenges at the segment level is set forth below.

• In Personal Systems, we continue to be negatively impacted by the market shift towards tablet

products within mobility, which has reduced the demand for consumer and notebook products. If

benefits from our new product investments in this area do not materialize, we will continue to

be negatively impacted by this trend. Personal Systems is also being impacted by consumer

demand weakness, particularly in EMEA and a competitive pricing environment.

42