HP 2013 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2013 HP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

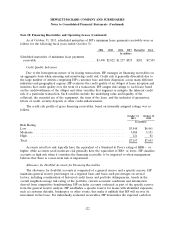

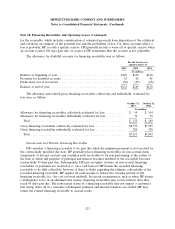

HEWLETT-PACKARD COMPANY AND SUBSIDIARIES

Notes to Consolidated Financial Statements (Continued)

Note 9: Financial Instruments (Continued)

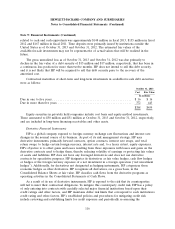

creditworthiness of counterparties. Master agreements with counterparties include master netting

arrangements as further mitigation of credit exposure to counterparties. These arrangements permit HP

to net amounts due from HP to a counterparty with amounts due to HP from the same counterparty.

HP does not offset the fair value of its derivative instruments against the fair value of cash collateral

receivable or payable under its master netting arrangements.

To further mitigate credit exposure to counterparties, HP has collateral security arrangements that

cover the vast majority of its counterparty risk. These arrangements require HP to post collateral or to

hold collateral from counterparties when derivative fair values exceed contractually established

thresholds which are generally based on the credit ratings of HP and its counterparties. If HP’s or the

counterparty’s credit rating falls below a specified credit rating, either party has the right to request full

collateralization on the derivatives’ net liability position. Such funds are generally transferred within two

business days of the due date. As of October 31, 2013, HP held $30 million of collateral and posted

$283 million under these collateralized arrangements, of which $30 million was through re-use of

counterparty cash collateral and $253 million was in cash. As of October 31, 2012, HP held

$198 million of collateral and posted $72 million under these collateralized arrangements, of which

$49 million was through re-use of counterparty cash collateral and $23 million in cash.

Further, under HP’s agreements with its counterparties, the counterparty can terminate all

outstanding trades following a covered change of control event affecting HP that results in the surviving

entity being rated below a specified credit rating. This credit contingent provision did not affect HP’s

financial position as of October 31, 2013 and October 31, 2012.

Fair Value Hedges

HP enters into fair value hedges to reduce the exposure of its debt portfolio to interest rate risk.

HP issues long-term debt in U.S. dollars based on market conditions at the time of financing. HP uses

interest rate swaps to mitigate the market risk exposures in connection with the debt to achieve a

primarily U.S. dollar LIBOR-based floating interest expense. The swap transactions generally involve

principal and interest obligations for U.S. dollar-denominated amounts. Alternatively, HP may choose

not to swap fixed for floating interest payments or may terminate a previously executed swap if it

believes a larger proportion of fixed-rate debt would be beneficial.

When investing in fixed-rate instruments, HP may enter into interest rate swaps that convert the

fixed interest payments into variable interest payments and would classify these swaps as fair value

hedges.

For derivative instruments that are designated and qualify as fair value hedges, HP recognizes the

gain or loss on the derivative instrument, as well as the offsetting loss or gain on the hedged item, in

Interest and other, net in the Consolidated Statements of Earnings in the period of change.

Cash Flow Hedges

HP uses a combination of forward contracts and options designated as cash flow hedges to protect

against the foreign currency exchange rate risks inherent in its forecasted net revenue and, to a lesser

extent, cost of sales, operating expenses, and intercompany loans denominated in currencies other than

the U.S. dollar. HP’s foreign currency cash flow hedges mature generally within twelve months.

However, certain leasing revenue-related forward contracts and intercompany loan forward contracts

extend for the duration of the lease or loan term, which can be up to five years.

117