BMW 2010 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2010 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

|

|

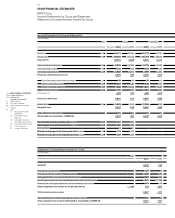

71 GROUP MANAGEMENT REPORT

Motorcycle markets in 2011

Despite the economic recovery in many countries, motor-

cycle markets contracted sharply again in 2010. We ex-

pect the situation to stabilise in some regions in 2011 and

market performance as a whole is likely to display a lateral

movement. For the 500 cc plus segment, however, we

forecast a low single-digit growth rate.

Financial Services market in 2011

There are favourable signs that the global economic

up-

swing will continue in 2011, although probably at a less

pronounced rate than in 2010. Given the substantial spare

capacities and moderate inflation rates currently prevail-

ing in the major industrial countries, central banks are

likely to continue their expansionary monetary policies

for the time being.

The US Reserve Bank has extended the range of expan-

sionary monetary policy measures taken. Given the over-

cast economic outlook, the zero-interest-rate policy

being pursued in the USA is unlikely to be abandoned

before the beginning of 2012. The European Central

Bank will not raise its refinancing interest rate before the

fourth quarter 2011 as long as there is a risk of a renewed

debt crisis. During the first half of the year the European

Central Bank could reduce excess liquidity step by step,

which could well cause interest rates in the medium-term

maturity segment to rise.

Providers of financial services are exposed on the one

hand to risks arising from uncertainties and volatility on

financial markets. On the other hand, however, measures

to reduce public spending could result in tax increases

worldwide and hence force down domestic demand.

The process of consolidating dealer organisations will

continue in a number of markets in 2011. As a result of

the related increase in risk, further credit-related losses

for the sector cannot be entirely ruled out for 2011.

It is currently very difficult to predict how used car

markets

will develop. Prices for pre-owned cars are likely

to stagnate during the coming twelve months. If the

economy falters, prices could fall again.

Outlook for the BMW Group in 2011

We expect macro-economic conditions to remain stable

in 2011. However, the threat of temporary setbacks

caused by knock-on effects from the recent crisis cannot

be ignored. International car markets are likely to con-

tinue

performing well and the Group’s growth markets

are expected to expand rapidly. Economic recovery should

continue to make progress in the USA and give our sales

volumes another boost. Taking all of these factors

into

consideration, the BMW Group will continue to perform

well in 2011.

Over the past year new models, innovative technologies

and attractive design have additionally driven customer

demand, which was already at a high level. Following on

from the introduction of new BMW 5 Series Sedan, the

new BMW 5 Series Touring has been available since mid-

autumn 2010

.

The BMW X1 isproving to be exceedingly

popular worldwide. The MINI range has been expanded

since autumn 2010 to include a fourth model, the MINI

Countryman. The Rolls-Royce Ghost is also experiencing

a high level of customer demand. On the heels of the

models introduced over the past year, we will be continu-

ing our new product initiative throughout 2011. In this

context we are currently rejuvenating the BMW 6 Series:

the Convertible will be available in Europe and Asia in

the spring, followed by the USA and other markets at the

beginning of May. The 6 Series Coupé will be launched

inautumn 2011. The new BMW X3, currently enjoying

great success in its class, will be launched worldwide over

the course of the year. The BMW 1 Series M Coupé will

come on to the markets in May, followed by the new

BMW M5 in autumn after its world debut at the IAA. The

new generation of the BMW 1 Series will also go on sale

from autumn 2011 onwards. The MINI Coupé will become

the fifth MINI model variant to join the family.

Engagement on growth markets, particularly Latin

America and Asia, and a wider international production

network resulting from the expansion of our plants in

the USA and China are helping us strengthen the BMW

Group in competitive terms. We are therefore laying the

foundation for profitable growth in the future.

We will continue to pursue a policy of rigorous cost

management in 2011, centred on the management of

fixed costs and working capital. The strategy also includes

the efficient utilisation of resources. The use of modular

and industrial standards is helping us to generate bene-

fits of scale and reduce production costs, an important

element in our new efficient development strategy, and

reflected in our R & D ratio of 4.6% (2009: 4.8%).

Our Strategy Number ONE remains the basis for the

BMW Group’s strategic realignment. Improvements