The Hartford 2009 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2009 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

|

|

129

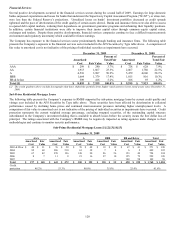

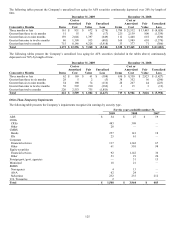

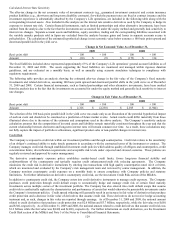

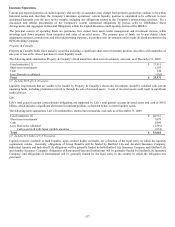

Calculated Interest Rate Sensitivity

The after-tax change in the net economic value of investment contracts (e.g., guaranteed investment contracts) and certain insurance

product liabilities (e.g., short-term and long-term disability contracts), for which the payment rates are fixed at contract issuance and the

investment experience is substantially absorbed by the Company’ s Life operations, are included in the following table along with the

corresponding invested assets. Also included in this analysis are the interest rate sensitive derivatives used by the Company to hedge its

exposure to interest rate risk. Certain financial instruments, such as limited partnerships and other alternative investments, have been

omitted from the analysis due to the fact that the investments are accounted for under the equity method and generally lack sensitivity to

interest rate changes. Separate account assets and liabilities, equity securities, trading and the corresponding liabilities associated with

the variable annuity products sold in Japan are excluded from the analysis because gains and losses in separate accounts accrue to

policyholders. The calculation of the estimated hypothetical change in net economic value below assumes a 100 basis point upward and

downward parallel shift in the yield curve.

Change in Net Economic Value As of December 31,

2009 2008

Basis point shift - 100 + 100 - 100 + 100

Amount $ (30) $ (9) $ (173) $ 114

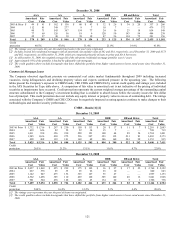

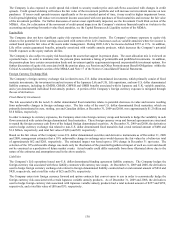

The fixed liabilities included above represented approximately 63% of the Company’ s Life operations’ general account liabilities as of

December 31, 2009 and 2008. The assets supporting the fixed liabilities are monitored and managed within rigorous duration

guidelines, and are evaluated on a monthly basis, as well as annually using scenario simulation techniques in compliance with

regulatory requirements.

The following table provides an analysis showing the estimated after-tax change in the fair value of the Company’ s fixed maturity

investments and related derivatives, assuming 100 basis point upward and downward parallel shifts in the yield curve as of December

31, 2009 and 2008. Certain financial instruments, such as limited partnerships and other alternative investments, have been omitted

from the analysis due to the fact that the investments are accounted for under the equity method and generally lack sensitivity to interest

rate changes.

Change in Fair Value As of December 31,

2009 2008

Basis point shift - 100 + 100 - 100 + 100

Amount $ 2,326 $ (2,230) $ 2,015 $ (1,944)

The selection of the 100 basis point parallel shift in the yield curve was made only as an illustration of the potential hypothetical impact

of such an event and should not be construed as a prediction of future market events. Actual results could differ materially from those

illustrated above due to the nature of the estimates and assumptions used in the above analysis. The Company’ s sensitivity analysis

calculation assumes that the composition of invested assets and liabilities remain materially consistent throughout the year and that the

current relationship between short-term and long-term interest rates will remain constant over time. As a result, these calculations may

not fully capture the impact of portfolio re-allocations, significant product sales or non-parallel changes in interest rates.

Credit Risk

The Company is exposed to credit risk within our investment portfolio and through counterparties. Credit risk relates to the uncertainty

of an obligor’ s continued ability to make timely payments in accordance with the contractual terms of the instrument or contract. The

Company manages credit risk through established investment credit policies which address quality of obligors and counterparties, credit

concentration limits, diversification requirements and acceptable risk levels under expected and stressed scenarios. These policies are

regularly reviewed and approved by senior management.

The derivative counterparty exposure policy establishes market-based credit limits, favors long-term financial stability and

creditworthiness of the counterparty and typically requires credit enhancement/credit risk reducing agreements. The Company

minimizes the credit risk in derivative instruments by entering into transactions with high quality counterparties rated A2/A or better,

which are monitored and evaluated by the Company’ s risk management team and reviewed by senior management. In addition, the

Company monitors counterparty credit exposure on a monthly basis to ensure compliance with Company policies and statutory

limitations. For further information on derivative counterparty credit risk, see the Investment Credit Risk section of the MD&A.

In addition to counterparty credit risk, the Company enters into credit derivative instruments to manage credit exposure. The Company

purchases credit protection through credit default swaps to economically hedge and manage credit risk of certain fixed maturity

investments across multiple sectors of the investment portfolio. The Company has also entered into credit default swaps that assume

credit risk to synthetically replicate the characteristics and performance of assets that would otherwise be permissible investments under

the Company’ s investment policies. Credit spread widening will generally result in an increase in fair value of derivatives that purchase

credit protection and a decrease in fair value of derivatives that assume credit risk. These derivatives do not receive hedge accounting

treatment and, as such, changes in fair value are reported through earnings. As of December 31, 2009 and 2008, the notional amount

related to credit derivatives that purchase credit protection was $2.6 billion and $3.7 billion, respectively, while the fair value was $(50)

and $340, respectively. As of December 31, 2009 and 2008, the notional amount related to credit derivatives that assume credit risk was

$1.2 billion, while the fair value was $(240) and $(403), respectively. For further information on credit derivatives, see the Investment

Credit Risk section of the MD&A and Note 5 of the Notes to Consolidated Financial Statements.