The Hartford 2009 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2009 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

|

|

106

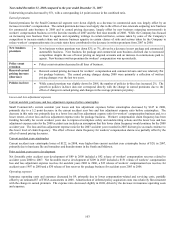

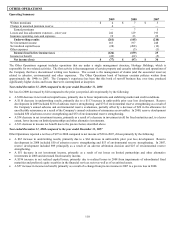

Year ended December 31, 2008 compared to the year ended December 31, 2007

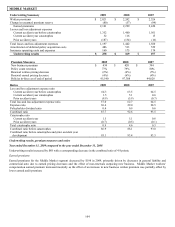

Underwriting results increased by $12 with a corresponding 0.9 point decrease in the combined ratio.

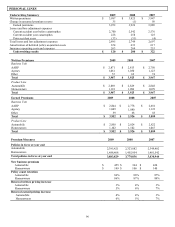

Earned premiums

Earned premiums for the Middle Market segment decreased by $121, or 5%, driven primarily by decreases in commercial auto,

workers’ compensation and general liability. Earned premium decreases were primarily due to a decline in earned pricing in 2008 and

the effect of non-renewals outpacing new business in commercial auto and general liability over the last nine months of 2007 and the

first nine months of 2008, partially offset by the effect of new business written premium outpacing non-renewals in workers’

compensation since the fourth quarter of 2007.

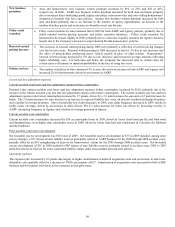

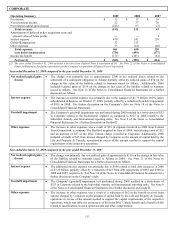

New business

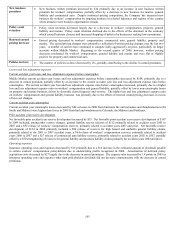

premium

• New business written premium increased by $26, or 7%, in 2008 as an increase in new business written

premium for workers’ compensation was partially offset by a decrease in new business for general liability,

marine and commercial auto. While continued price competition and the effect of some state-mandated rate

reductions in workers' compensation has lessened the attractiveness of new business in certain lines and

regions, the Company has increased new business for workers’ compensation due, in part, to the effect of

targeting business in selected industries and regions of the country.

Policy count

retention

• Policy count retention decreased due largely to a decrease in retention for general liability.

Renewal earned

pricing decrease

• Renewal earned pricing decreased in workers’ compensation, commercial auto, general liability, property

and marine. The earned pricing decreases in 2008 were primarily a reflection of written pricing changes

over the last two years. A number of carriers have continued to compete fairly aggressively on price,

particularly on larger accounts within Middle Market, which has contributed to mid-single digit price

decreases across the industry.

Policies in-force • The number of policies in-force increased by 3%, due largely to growth on smaller accounts.

Losses and loss adjustment expenses

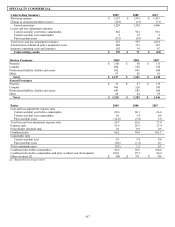

Current accident year losses and loss adjustment expenses before catastrophes

Middle Market current accident year losses and loss adjustment expenses before catastrophes decreased by $101 due largely to a

decrease in earned premium. Before catastrophes, the current accident year loss and loss adjustment expense ratio decreased by 1.0

point, primarily due to a lower loss and loss adjustment expense ratio on workers’ compensation and general liability business, largely

offset by higher non-catastrophe losses on property and marine business and the effect of earned pricing decreases. The higher non-

catastrophe losses on property business were driven by increased severity, including a number of large individual claims, and the higher

non-catastrophe losses on marine business were primarily driven by increased frequency.

Current accident year catastrophes

Current accident year catastrophe losses of $116 in 2008 were higher than current accident year catastrophe losses of $15 in 2007,

primarily due to losses from hurricane Ike and tornadoes and thunderstorms in the South and Midwest.

Prior accident year development

Net favorable prior accident year reserve development increased by $118 in 2008. Net favorable reserve development of $134 in 2008

primarily included a $90 release of reserves for high hazard and umbrella general liability claims, primarily related to the 2001 to 2007

accident years, a $64 release of workers’ compensation reserves, primarily related to accident years 2000 to 2007 and a $27 release of

commercial auto liability reserves, primarily related to accident years 2002 to 2007, partially offset by a $50 strengthening of reserves

for general liability and products liability claims primarily for accident years 2004 and prior.

Net favorable reserve development of $16 in 2007 primarily included a $49 release of general liability loss and loss adjustment expense

reserves for accident years 2003 to 2006 and an $18 release of commercial auto liability reserves for accident years 2003 and 2004,

partially offset by a $40 strengthening of workers’ compensation reserves for accident years 1973 & prior and a $14 strengthening of

general liability reserves for accident years more than 20 years old.

Operating expenses

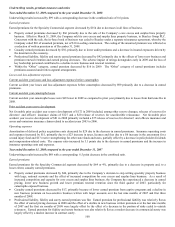

The $16 decrease in the amortization of deferred policy acquisition costs was largely due to the decrease in earned premium, partially

offset by the amortization of higher underwriting costs. Insurance operating costs and expenses included policyholder dividends of $21

in 2008 and $14 in 2007 which increased primarily due to a $6 increase in the estimated amount of dividends payable to certain

workers’ compensation policyholders due to underwriting profits. Apart from policyholder dividends, insurance operating costs and

expenses decreased by $6 as the effect of lower compensation-related costs was partially offset by higher IT costs and an estimated $3

of TWIA assessments in 2008. The expense ratio increased by 0.5 points due to the amortization of higher underwriting costs, the

TWIA assessments in 2008 and the effect of lower earned premiums, partially offset by the effect of lower compensation-related costs.