The Hartford 2009 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2009 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

|

|

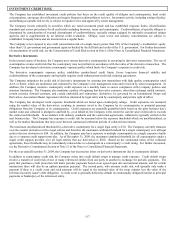

112

PROPERTY & CASUALTY UNDERWRITING RISK MANAGEMENT STRATEGY

The Hartford's property and casualty operations have processes to manage risk related to natural disasters, such as hurricanes and

earthquakes, and other perils, such as terrorism. The Hartford's risk management processes include, but are not limited to, disciplined

underwriting protocols, exposure controls, sophisticated risk modeling, risk transfer, and capital management strategies.

In managing risk, The Hartford's management processes involve establishing underwriting guidelines for both individual risks, including

individual policy limits, and in aggregate, including aggregate exposure limits by geographic zone and peril. The Company establishes

risk limits and actively monitors the risk exposures as a percent of Property & Casualty statutory surplus. For natural catastrophe perils,

the Company generally limits its estimated loss to natural catastrophes from a single 250-year event prior to reinsurance to less than

30% of statutory surplus of the Property & Casualty operations and its estimated loss to natural catastrophes from a single 250-year

event after reinsurance to less than 15% of statutory surplus of the Property & Casualty operations. From time to time, the estimated

loss to natural catastrophes from a single 250-year event prior to reinsurance may fluctuate above or below 30% of statutory surplus due

to changes in modeled loss estimates, exposures, or statutory surplus. Currently, the Company's estimated pre-tax loss to a single 250-

year natural catastrophe event prior to reinsurance is less than 30% of the statutory surplus of the Property & Casualty operations and

the Company’ s estimated pre-tax loss net of reinsurance is less than 15% of statutory surplus of the Property & Casualty operations. For

terrorism, the Company monitors its exposure in major metropolitan areas to a single-site conventional terrorism attack scenario, and

manages its potential estimated loss, including exposures resulting from the Company's Group Life operations, to less than $1.3 billion.

Among the landmark locations specifically monitored by the Company as of December 31, 2009, the largest estimated modeled loss

arising from a single event is approximately $1.1 billion. The Company monitors exposures monthly and employs both internally

developed and vendor-licensed loss modeling tools as part of its risk management discipline.

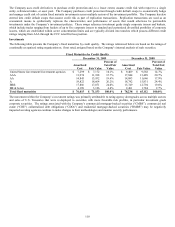

Use of Reinsurance

In managing risk, The Hartford utilizes reinsurance to transfer risk to well-established and financially secure reinsurers. Reinsurance is

used to manage aggregations of risk as well as to transfer certain risks to reinsurance companies based on specific geographic or risk

concentrations. All treaty purchases related to the Company’ s property and casualty operations are administered by a centralized

function to support a consistent strategy and ensure that the reinsurance activities are fully integrated into the organization’ s risk

management processes.

A variety of traditional reinsurance products are used as part of the Company’ s risk management strategy, including excess of loss

occurrence-based products that protect property and workers’ compensation exposures, and individual risk or quota share arrangements,

that protect specific classes or lines of business. The Company has no significant finite risk contracts in place and the statutory surplus

benefit from all such prior year contracts is immaterial. Facultative reinsurance is used by the Company to manage policy-specific risk

exposures based on established underwriting guidelines. The Hartford also participates in governmentally administered reinsurance

facilities such as the Florida Hurricane Catastrophe Fund (“FHCF”), the Terrorism Risk Insurance Program established under The

Terrorism Risk Insurance Program Reauthorization Act of 2007 (“TRIPRA”) and other reinsurance programs relating to particular risks

or specific lines of business.

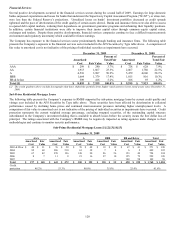

The Company has several catastrophe reinsurance programs, including reinsurance treaties that cover property and workers’

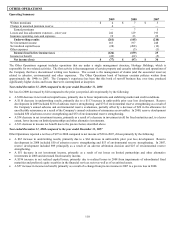

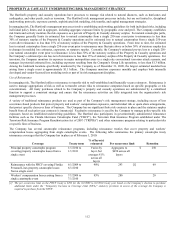

compensation losses aggregating from single catastrophe events. The following table summarizes the primary catastrophe treaty

reinsurance coverages that the Company has in place as of February 1, 2010:

Coverage

Treaty term

% of layer(s)

reinsured

Per occurrence limit

Retention

Principal property catastrophe program

covering property catastrophe losses from a

single event

1/1/2010 to

1/1/2011

Varies by

layer, but

averages 81%

across all

layers

Aggregates to

$690 across all

layers

$250

Reinsurance with the FHCF covering Florida

Personal Lines property catastrophe losses

from a single event

6/1/2009 to

6/1/2010

90% 293 [1] 69

Workers’ compensation losses arising from a

single catastrophe event

7/1/2009 to

7/1/2010

95% 280 20

[1] The per occurrence limit on the FHCF treaty is $293 for the 6/1/2009 to 6/1/2010 treaty year based on the Company’s election to purchase

additional limits under the “Temporary Increase in Coverage Limit (TICL)” statutory provision in excess of the coverage the Company is

required to purchase from the FHCF.