Xcel Energy 2010 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2010 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

71

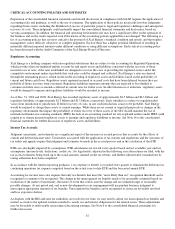

Derivatives, Risk Management and Market Risk

In the normal course of business, Xcel Energy and its subsidiaries are exposed to a variety of market risks. Market risk is the

potential loss or gain that may occur as a result of changes in the market or fair value of a particular instrument or commodity. All

financial and commodity-related instruments, including derivatives, are subject to market risk. See Note 11 to the consolidated

financial statements for further discussion of market risks associated with derivatives.

Xcel Energy is exposed to the impact of changes in price for energy and energy related products, which is partially mitigated by

Xcel Energy’s use of commodity derivatives. Though no material non-performance risk currently exists with the counterparties to

Xcel Energy’s commodity derivative contracts, distress in the financial markets may in the future impact that risk to the extent it

impacts those counterparties. Distress in the financial markets may also impact the fair value of the debt and equity securities in

the nuclear decommissioning fund and master pension trust, as well as Xcel Energy’s ability to earn a return on short-term

investments of excess cash.

Commodity Price Risk — Xcel Energy’s utility subsidiaries are exposed to commodity price risk in their electric and natural gas

operations. Commodity price risk is managed by entering into long- and short-term physical purchase and sales contracts for

electric capacity, energy and energy-related products and for various fuels used in generation and distribution activities.

Commodity price risk is also managed through the use of financial derivative instruments. Xcel Energy’s risk management policy

allows it to manage commodity price risk within each rate-regulated operation to the extent such exposure exists.

Short-Term Wholesale and Commodity Trading Risk — Xcel Energy’s utility subsidiaries conduct various short-term wholesale

and commodity trading activities, including the purchase and sale of electric capacity, energy and energy-related instruments.

Xcel Energy’s risk management policy allows management to conduct these activities within guidelines and limitations as

approved by its risk management committee, which is made up of management personnel not directly involved in the activities

governed by this policy.

Changes in the fair value of commodity trading contracts before the impacts of margin-sharing mechanisms for the years ended

Dec. 31, were as follows:

(Thousands of Dollars) 2010 2009

Fair value of commodity trading net contract assets outstanding at Jan. 1 ............................ $ 9,628 $ 4,169

Contracts realized or settled during the period ....................................................... (4,449) (21,740)

Commodity trading contract additions and changes during period.................................

.

15,070 27,199

Fair value of commodity trading net contract assets outstanding at Dec. 31 ........................

.

$ 20,249 $ 9,628

At Dec. 31, 2010, the fair values by source for the commodity trading net asset balance were as follows:

Futures / Forwards

(Thousands of Dollars) Source of

Fair Value

Maturity

Less Than

1 Year Maturity

1 to 3 Years Maturity

4 to 5 Years

Maturity

Greater Than

5 Years

Total

Futures/

Forwards

Fair Value

N

SP-Minnesota ....................

.

1 $ 5,914 $ 11,523 $ 976 $

—

$ 18,413

PSCo ..............................

.

1 573 1,245

—

—

1,818

$ 6,487 $ 12,768 $ 976 $

—

$ 20,231

Options

(Thousands of Dollars) Source of

Fair Value

Maturity

Less Than

1 Year Maturity

1 to 3 Years Maturity

4 to 5 Years

Maturity

Greater Than

5 Years Total Options

Fair Value

N

SP-Minnesota ....................

.

2 $ 18 $

—

$

—

$

—

$18

$18 $

—

$

—

$

—

$18

1 — Prices actively quoted or based on actively quoted prices.

2 — Prices based on models and other valuation methods. These represent the fair value of positions calculated using internal

models when directly and indirectly quoted external prices or prices derived from external sources are not available. Internal

models incorporate the use of options pricing and estimates of the present value of cash flows based upon underlying contractual

terms. The models reflect management’s estimates, taking into account observable market prices, estimated market prices in the

absence of quoted market prices, the risk-free market discount rate, volatility factors, estimated correlations of commodity prices

and contractual volumes. Market price uncertainty and other risks also are factored into the models.