Travelers 2015 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2015 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

|

|

• Litigation trends

• Frequency of claims with payment capped by policy limits

• Change in average severity of accidents, or proportion of severe accidents

• Subrogation opportunities

• Degree of patient responsiveness to treatment

• Changes in claim handling philosophies

No-fault risk factors (for selected states and time periods)

• Effectiveness of no-fault laws

• Frequency of visits to health providers

• Number of medical procedures given during visits to health providers

• Types of health providers used

• Types of medical treatments received

• Changes in cost of medical treatments

• Degree of patient responsiveness to treatment

Personal automobile book of business risk factors

• Changes in policy provisions (e.g., deductibles, policy limits, endorsements, etc.)

• Changes in underwriting standards

• Changes in the use of credit data for rating and underwriting

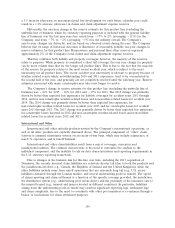

Unanticipated changes in risk factors can affect reserves. As an indicator of the causal effect that a

change in one or more risk factors could have on reserves for personal automobile, a 1% increase

(decrease) in incremental paid loss development for each future calendar year could result in a 1.1%

increase (decrease) in claims and claim adjustment expense reserves.

Historically, the one-year change in the reserve estimate for this product line over the last nine

years has varied from 5% to 3% (averaging 0%) for the Company, and from 4% to 0%

(averaging 2%) for the industry overall. The Company’s year-to-year changes are driven by, and are

based on, observed events during the year. The Company believes that its range of historical outcomes

is illustrative of reasonably possible one-year changes in reserve estimates for this product line.

Personal automobile reserves represent approximately 5% of the Company’s total claims and claim

adjustment expense reserves.

The Company’s change in reserve estimate for this product line was 4% for 2015, 1% for 2014

and 1% for 2013. The change for 2015 was primarily driven by better than expected loss experience for

liability coverages for accident years 2012 through 2014.

Homeowners and Personal Lines Other

Homeowners is generally considered a short tail coverage. Most payments are related to the

property portion of the policy, where the claim reporting and settlement process is generally restricted

to the insured and the insurer. Claims on property coverage are typically reported soon after the actual

damage occurs, although delays of several months are not unusual. The resulting settlement process is

typically fairly short term, although exceptions do exist.

148