Symantec 2013 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2013 Symantec annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

|

|

Under current law, long-term capital gains are generally subject to lower tax rates than ordinary income. If the

fair market value of the stock on the date of the disposition is less than the purchase price paid for the shares,

there will be no ordinary income, and any loss recognized will be a capital loss.

If the stock is sold or disposed of before the expiration of either of the holding periods described above, then

the excess of the fair market value of the stock on the Purchase Date for the shares over the purchase price will

be treated as ordinary income at the time of the sale or disposition. The balance of any gain will be treated as

capital gain. Even if the stock is disposed of for less than its Purchase Date fair market value, the same amount of

ordinary income is attributed to the participant, and a capital loss is recognized equal to the difference between

the sales price and the fair market value of the stock on such Purchase Date. Any capital gain or loss will be

short-term or long-term, depending on how long the stock has been held.

There are no U.S. federal income tax consequences to Symantec by reason of the grant or exercise of options under

the ESPP. Symantec is entitled to a deduction to the extent amounts are taxed as ordinary income to a participant.

Symantec may also grant options under Non-Statutory Plans to employees of our designated subsidiaries

and affiliates that do not participate in the Statutory Plan. The specific terms of such Non-Statutory Plans are not

yet known; accordingly, it is not possible to discuss with certainty the relevant tax consequences of these Non-

Statutory Plans. The Non-Statutory Plans will be sub-plans of the ESPP that are generally not intended to qualify

under the provisions of Sections 421 and 423 of the Code. Therefore, it is likely that at the time of the exercise of

an option under a Non-Statutory Plan, an employee subject to tax under the Code would recognize ordinary

income equal to the excess of the fair market value of the stock on the date of exercise and the purchase price,

Symantec would be able to claim a tax deduction equal to this difference, and Symantec would be required to

withhold employment taxes and income tax at the time of the purchase.

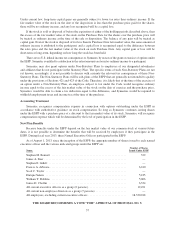

Accounting Treatment

Symantec recognizes compensation expense in connection with options outstanding under the ESPP in

accordance with authoritative guidance on stock compensation. So long as Symantec continues issuing shares

under the ESPP with a purchase price at a discount to the fair market value of its stock, Symantec will recognize

compensation expense which will be determined by the level of participation in the ESPP.

New Plan Benefits

Because benefits under the ESPP depend on the fair market value of our common stock at various future

dates, it is not possible to determine the benefits that will be received by employees if they participate in the

ESPP. During fiscal year 2013, three Named Executive Officers participated in the ESPP.

As of August 1, 2013, since the inception of the ESPP, the aggregate number of shares issued to each named

executive officer and the various indicated groups under the ESPP are:

Name:

Number of Shares

Issued Under ESPP

Stephen M. Bennett ................................................... 522

James A. Beer ........................................................ —

Stephen E. Gillett ..................................................... —

Francis A. deSouza .................................................... 6,240

Scott C. Taylor ....................................................... —

Enrique Salem ....................................................... 5,185

William T. Robbins ................................................... 5,006

Janice D. Chaffin ..................................................... 6,334

All current executive officers as a group (6 persons) .......................... 12,491

All current non-employee directors as a group (7 persons) ..................... —

All employees, excluding current executive officers .......................... 18,330,018

THE BOARD RECOMMENDS A VOTE “FOR” APPROVAL OF PROPOSAL NO. 5.

37