Shaw 2011 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2011 Shaw annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

|

|

Shaw Communications Inc.

MANAGEMENT’S DISCUSSION AND ANALYSIS

August 31, 2011

flows are based on the Company’s estimates of future operating results, economic conditions and

the competitive environment. The terminal value is estimated using both a perpetuity growth

assumption and a multiple of operating income before amortization. The discount rates used in

the analysis are based on the Company’s weighted average cost of capital and an assessment of

the risk inherent in the projected cash flows. In analyzing the fair value determined by the DCF

analysis the Company also considers a market approach determining a fair value for each unit and

total entity value determined using a market capitalization approach.

The Company tests goodwill and indefinite-lived intangible assets for impairment annually

during the third quarter, or more frequently if events or changes in circumstances warrant. The

annual impairment test for the current year was conducted as at March 1, 2011 and the fair

value of each of the reporting units exceeded their carrying value by a significant amount.

The Company conducted an impairment test on its wireless spectrum utilizing the Greenfield

Approach as at March 1, 2011. The fair value of the assets exceeded their carrying amount.

During August 2011 the Company discontinued construction of a traditional wireless network

and considered if this would result in an impairment to the spectrum carrying value. The

Company concluded that the carrying value of the AWS licenses continues to be appropriate

and intends to hold these assets while it reviews all options. A hypothetical decline of 10% in

the fair value of the wireless spectrum as at March 1, 2011 and August 31, 2011 would not

result in any impairment loss.

A hypothetical decline of 10% and 20% in the fair value of the broadcast rights for each reporting

unit as at March 1, 2011 would not result in any impairment loss. Further, any changes in

economic conditions since the impairment testing conducted as at March 1, 2011 do not represent

events or changes in circumstance that would be indicative of impairment at August 31, 2011.

Significant estimates inherent to this analysis include discount rates and the terminal value. At

March 1, 2011, the estimates that have been utilized in the impairment tests reflect any

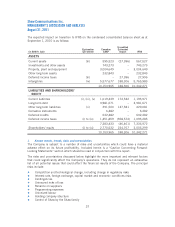

changes in market conditions and are as follows:

Terminal Value

Discount Rate Terminal Growth Rate

Terminal Operating Income

before Amortization

Multiple

Cable systems 9.0% 1.75% 5.5x

DTH and satellite services 11.0% 1.50% 5.0x

Media 9.0% 1.00% 7.0x

Wireless 11.5% 0.50% 5.5x

A sensitivity analysis of significant estimates is conducted as part of every impairment

test. With respect to the impairment tests performed in the third quarter, the estimated decline

in fair value for the sensitivity of significant estimates is as follows:

Estimated decline in fair value

Terminal Value

1% Increase in

Discount Rate

1% Decrease in

Terminal Growth Rate

0.5 Times Decrease in

Terminal Operating

Income before Amortization

Multiple

Cable systems 8% 4% 3%

DTH and satellite services 7% 3% 3%

Media 8% 22% 2%

Wireless 45% 16% 21%

28