Rogers 2010 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2010 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

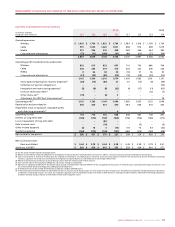

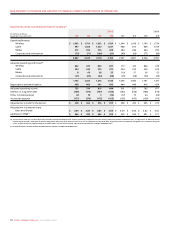

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

70 ROGERS COMMUNICATIONS INC. 2010 ANNUAL REPORT

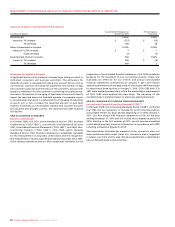

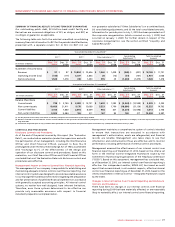

Other impacts

Private investments: Under IFRS, the Company’s investments in equity

instruments that do not have a quoted market price must be measured

at fair value. Under Canadian GAAP, these instruments are measured at

historical cost. The impact on transition is expected to increase the

carrying value of investments by $1 million with a corresponding

increase to the available-for-sale equity reserve. Comprehensive income

for the year ended December 31, 2010 is expected to decrease by

$2 million.

Deferred Income Tax: We have not identified any differences in the

recognition and measurement of deferred income taxes under IFRS;

however, we have determined the deferred tax impact of each of the

above accounting changes. Per the requirements of IFRS 1, the deferred

tax adjustment will be recorded in opening retained earnings upon

transition to IFRS. We expect the impact of the change at January1,2010

will be to decrease the net deferred tax liability by $34 million. Income

tax expense for the year ended December 31, 2010 is expected to

increase by $2 million and income tax expense related to other

comprehensive income for the year ended December 31, 2010 is

expected to decrease by $20 million.

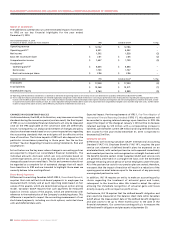

First-Time Adoption of International Financial Reporting Standards

Our adoption of IFRS will require the application of IFRS 1, which

provides guidance for an entity’s initial adoption of IFRS. IFRS 1

generally requires that an entity apply all IFRS effective at the end of its

first IFRS reporting period retrospectively. However, IFRS 1 does include

certain mandatory exceptions and limited optional exemptions in

specified areas of certain standards from this general requirement. The

following are the significant optional exemptions available under

IFRS1 that we expect to apply in preparing our first financial statements

under IFRS.

Business

Combinations

We expect to elect to not restate any Business

Combinations that have occurred prior to

January 1, 2010.

Borrowing

Costs

We expect to elect to apply the requirements

of IAS 23 Borrowing Costs prospectively from

January 1, 2010.

The information above is provided to allow investors and others to

obtain a better understanding of our IFRS changeover plan and the

resulting possible effects on, for example, our financial statements and

operating performance measures. These are estimates based on our

current understandings, and readers are cautioned that it may not be

appropriate to use such information for any other purpose. This

information also reflects our most recent assumptions and expectations;

circumstances may arise, such as changes in IFRS, regulations or

economic conditions, which could change these assumptions or

expectations.

The following unaudited consolidated financial statements show the

expected impacts of the above noted differences between IFRS and

Canadian GAAP as at the date of transition (January 1, 2010) and as at

and for the year ended December 31, 2010.

Expected impact: Per the requirements of IFRS 1, this adjustment will be

recorded in opening retained earnings upon transition to IFRS. We

expect the impact of the change at January 1, 2010 will be to increase

retained earnings by $4 million. Additionally, the liability balance will

be reclassified to unearned revenue from accounts payable and accrued

liabilities. Net income for the year ended December 31, 2010 is expected

to decrease by $3 million.

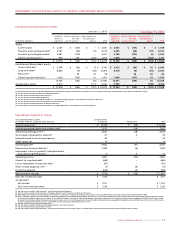

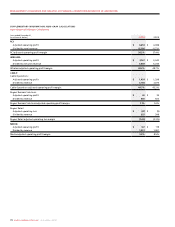

Impairment of Assets

Differences from existing Canadian GAAP: IAS 36, Impairment of Assets

(“IAS 36”), uses a one-step approach for both testing for and

measurement of impairment, with asset carrying values compared

directly with the higher of fair value less costs to sell and value in use

(which uses discounted future cash flows). Canadian GAAP however,

uses a two-step approach to impairment testing: first comparing asset

carrying values with undiscounted future cash flows to determine

whether impairment exists; and then measuring any impairment by

comparing asset carrying values with fair values.

Additionally, under Canadian GAAP assets are grouped at the lowest

level for which identifiable cash flows are largely independent of the

cash flows of other assets and liabilities for impairment testing

purposes. IFRS requires that assets be tested for impairment at the level

of cash generating units, which is the lowest level of assets that

generate largely independent cash inflows. This lower-level grouping

could result in identification of impairment more frequently under

IFRS, but of potentially smaller amounts.

However, with the exception of goodwill, any impairment losses may

potentially be offset by the requirement under IAS 36 to reverse any

previous impairment losses where circumstances have changed.

Canadian GAAP prohibits reversal of impairment losses.

Expected impact: Our impairment testing for the January 1, 2010

opening balance sheet under IFRS did not result in the recognition of

any additional impairment losses or reversals of previously recorded

impairment losses. Based on our impairment testing for the year ended

December 31, 2010, we expect to recognize an additional $5 million

impairment over the amount recognized under Canadian GAAP.

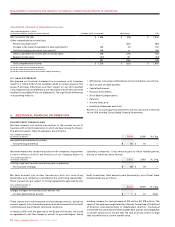

Provisions for Onerous Contracts

Differences from existing Canadian GAAP: IAS 37 Provisions, Contingent

Liabilities and Contingent Assets (“IAS 37”), requires an entity to

recognize a provision when a contract becomes onerous, that is when it

has a contract in which the unavoidable costs of meeting the obligations

under the contract exceed the economic benefits expected to be

received under it. The unavoidable costs under a contract reflect the

least net cost of exiting from the contract, which is the lower of the cost

of fulfilling it and any compensation or penalties arising from failure to

fulfill it. If an entity has a contract that is onerous, the present

obligation under the contract shall be recognized and measured as a

provision. Canadian GAAP only requires the recognition of such a

liability in certain situations (e.g. for operating leases that the entity

has ceased to use). This difference could result in recognition of an

obligation under IFRS that was not previously recognized under

Canadian GAAP.

Expected impact: Our review of significant contracts at January 1, 2010

identified one contract that must be provided for under IFRS. Per the

requirements of IFRS 1, this adjustment will be recorded in opening

retained earnings upon transition to IFRS. The impact of the change at

January 1, 2010 is expected to decrease retained earnings by $29

million. During the fourth quarter of 2010, a second contract became

onerous. The impact of both contracts on the December 31, 2010

balance sheet was to recognize a total onerous contract provision of

$35 million. Net income for the year ended December 31, 2010 is

expected to decrease by $6 million, which includes both partial

utilization of the opening provision as well as the recognition of

additional provisions.