Rogers 2010 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2010 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

ROGERS COMMUNICATIONS INC. 2010 ANNUAL REPORT 25

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

WIRELESS STRATEGY

Wireless’ objective is to drive profitable growth within the Canadian

wireless communications industry, and its strategy is designed to

maximize subscriber share, cash flow and return on invested capital.

The key elements of its strategy are as follows:

• Continually enhancing its scale and competitive position in the

Canadian wireless communications market;

• Focusingonofferinginnovativevoiceandwirelessdataservices

into the targeted youth, family, and small and medium-sized

business segments, and specifically to drive increased penetration of

smartphones and other advanced wireless devices;

• Enhancing the customer experience through ongoing focus

principally in the areas of wireless devices, network quality and

customer service in order to maximize service revenue and minimize

customer deactivations, or churn;

• Increasingrevenuefromexistingcustomersbycrosssellingandup

selling wireless data and other enhanced and converged services to

wireless voice customers;

• Enhancingandexpandingownedandthirdpartysalesdistribution

channels to deliver products, services and support to customers;

• Maintainingthemosttechnologicallyadvanced,high-qualityand

national wireless network possible with global coverage enabled by

widely adopted global standard network technologies; and

• Leveraging relationships across the Rogers group of companies

to provide bundled product and service offerings at attractive

prices to common customers, in addition to implementing cross-

selling, distribution and branding initiatives as well as leveraging

infrastructure sharing opportunities.

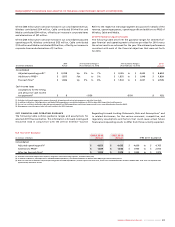

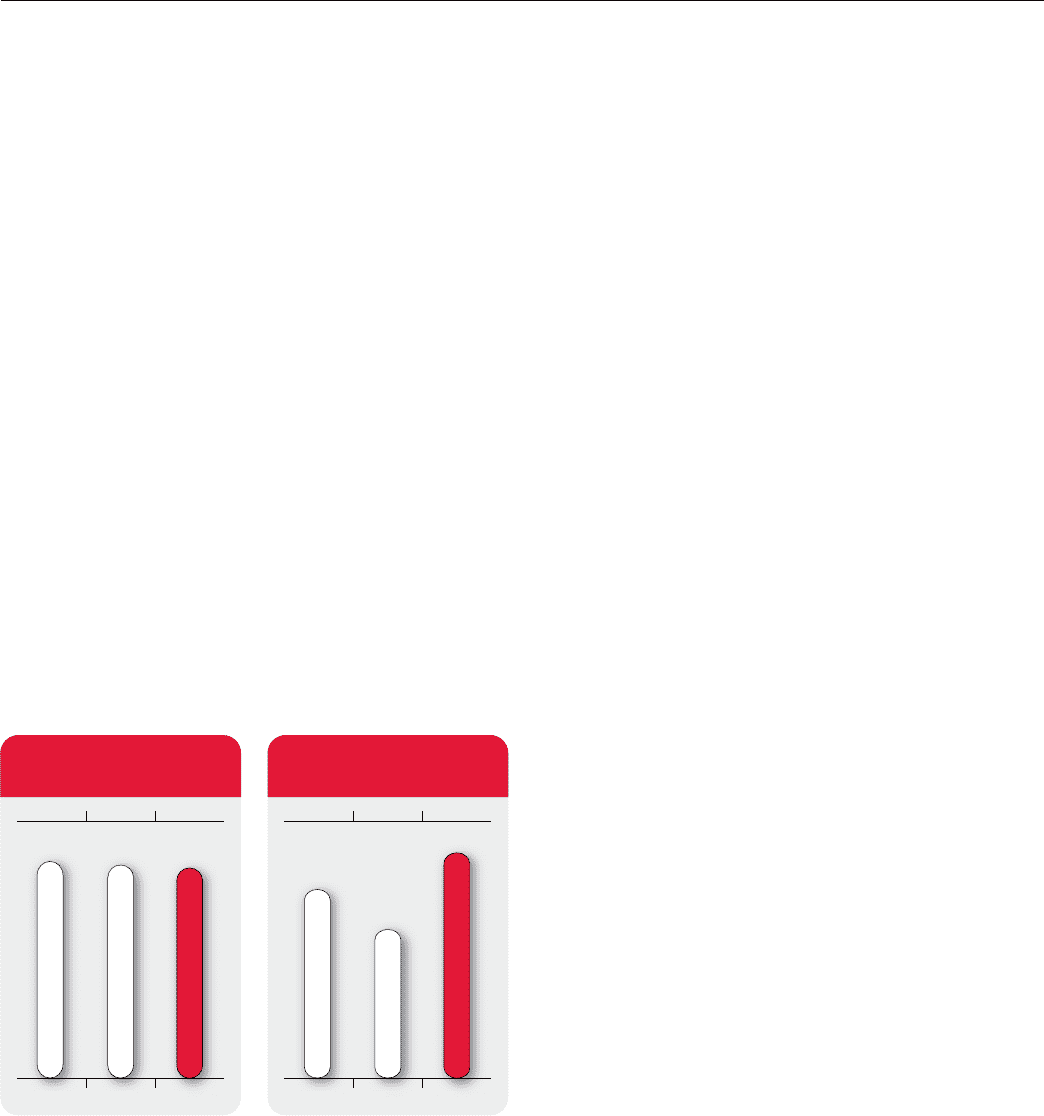

20102009

2008

2009

200

8

201

0

$73.12$73.93$75.41

WIRELESS POSTPAID

MONTHLY ARPU

20102009

2008

2009

200

8

201

0

1.18%1.06%1.10%

WIRELESS POSTPAID

MONTHLY CHURN

RECENT WIRELESS INDUSTRY TRENDS

Focus on Customer Retention

The wireless communications industry’s current market penetration in

Canada is estimated to be 74% of the population, compared to

approximately96%intheU.S.andapproximately121%intheUnited

Kingdom, and Wireless expects the Canadian wireless industry to

continue to grow by approximately 4 to 5 percentage points of

penetration each year for the next several years. As penetration

deepens, it requires an increasing focus on customer satisfaction, the

promotion of new data and voice services to existing customers, and

customer retention.

Demand for Sophisticated Data Applications

The ongoing development of wireless data transmission technologies

has led wireless device developers, such as handsets and portable

computing devices, to develop more sophisticated smartphone type

devices with increasingly advanced capabilities, including access to

e-mail and other corporate information technology platforms, news,

sports, financial information and services, shopping services, photos,

music, applications, and streaming video clips, mobile television and

other functions. Wireless believes that the introduction of such new

devices and applications will drive continued growth of wireless data

services. Along with the acceleration of smartphone penetration comes

the higher costs of equipment subsidies.

Increased Competition from Other Wireless Operators

Wireless faces increased competition from incumbent wireless

operators as well as new entrants, which is fully described in the section

of this MD&A entitled “Competition in our Businesses”. Some new

entrants are introducing new unlimited pricing plans which have

resulted in downward price adjustments and lower ARPU.

Migration to Next Generation Wireless Technology

The ongoing development of wireless data transmission technologies

and the increased demand for sophisticated wireless services, especially

data communications services, have led wireless providers to migrate

towards the next generation of digital voice and data broadband

wireless networks such as HSPA+ and LTE. These networks are intended

to provide wireless communications with wireline quality sound, far

higher data transmission speeds with increased efficiency, and

enhanced streaming video capabilities. These networks support a

variety of increasingly advanced data applications, including broadband

Internet access, multimedia services and seamless access to corporate

information systems, including desktop, client and server-based

applications that can be accessed on a local, national or international

basis. Wireless has been progressing towards next generation

technology with LTE technical trials being conducted in the Ottawa

area. Capital intensity is expected to increase with continuing network

investments.

Development of Additional Technologies

In addition to the two main technology paths of the mobile/broadband

wireless industry, namely GSM/HSPA and Code Division Multiple Access/

Evolution Data Optimized (“CDMA/EVDO”), three other significant

broadband wireless technologies are in the process of development:

WiFi, WiMAX and LTE. These technologies may accelerate the

widespread adoption of digital voice and broadband wireless data

networks.

WiFi (the IEEE 802.11 industry standard) allows suitably equipped

devices, such as laptop computers and personal digital assistants, to

connect to a local area wireless access point. These access points utilize

unlicenced spectrum and the wireless connection is only effective

within a local area radius of approximately 50–100 metres of the access

point, and provide speeds similar to a wired local area network (“LAN”)

environment (most recently the version designated as 802.11n). As the

technology is primarily designed for in-building wireless access, many

access points must be deployed to cover the selected local geographic

area, and must also be interconnected with a broadband network to

supply the connectivity to the Internet. Future enhancements to the

range of WiFi service and the networking of WiFi access points may

provide additional opportunities for wireless operators or municipal

WiFi network operators, each providing capacity and coverage under

the appropriate circumstances.

LTE, the worldwide GSM community’s new fourth generation (“4G”)

broadband wireless technology evolution path, is being deployed in

certain parts of the world. LTE is planned to be an all IP-based wireless

data technology based on a new modulation scheme (orthogonal

frequency-division multiplexing) that is specifically designed to improve