Rogers 2010 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2010 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

ROGERS COMMUNICATIONS INC. 2010 ANNUAL REPORT 49

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

relieves us of primary responsibility for, and eliminates significant risk

associated with, the accrued benefit obligation for the retired

employees. The non-cash settlement loss arising from this settlement

of pension obligations was $30 million and was recorded in 2009. The

Company did not make any additional lump-sum contributions to its

pension plans in the year ended December 31, 2010.

INTEREST RATE AND FOREIGN EXCHANGE MANAGEMENT

Economic Hedge Analysis

For the purposes of our discussion on the hedged portion of long-term

debt, we have used non-GAAP measures in that we include all

Derivatives, whether or not they qualify as hedges for accounting

purposes, since all such Derivatives are used for risk management

purposes only and are designated as a hedge of specific debt

instruments for economic purposes. As a result, the Canadian dollar

equivalent of U.S. dollar-denominated long-term debt reflects the

contracted foreign exchange rate for all of our Derivatives regardless of

qualifications for accounting purposes as a hedge.

As discussed above in the section entitled “Debt Redemptions and

Termination of Derivatives”, in August 2010, RCI redeemed all of its

US$490 million 9.625% Senior Notes due 2011 and terminated the

related US$500 million notional principal amount of Derivatives. As a

result,onDecember31,2010,100%ofourU.S.dollar-denominated

debtwashedgedonaneconomicbasiswhile93%ofourU.S.dollar-

denominated debt was hedged on an accounting basis. The Derivatives

hedgingourUS$350million7.50%SeniorNotesdue2038donotqualify

as hedges for accounting purposes.

Mark-to-Market Value of Derivatives

In accordance with Canadian GAAP, we have recorded our Derivatives

using an estimated credit-adjusted mark-to-market valuation which is

determined by increasing the treasury-related discount rates used to

calculate the risk-free estimated mark-to-market valuation by an

estimated bond spread (“Bond Spread”) for the relevant term and

counterparty for each Derivative. In the case of Derivatives accounted

for as assets (i.e. those Derivatives for which the counterparties owe

Rogers), the Bond Spread for the bank counterparty was added to the

risk-free discount rate to determine the estimated credit-adjusted value

whereas, in the case of Derivatives accounted for as liabilities (i.e. those

instruments for which we owe the counterparties), Rogers’ Bond

Spread was added to the risk-free discount rate. The estimated credit-

adjusted values of the Derivatives are subject to changes in credit

spreads of Rogers and its counterparties.

The effect of estimating the credit-adjusted fair value of Derivatives at

December 31, 2010 versus the unadjusted risk-free mark-to-market

value of Derivatives is illustrated in the table below. As at December 31,

2010, the credit-adjusted estimated net liability value of Rogers’

Derivatives portfolio was $900 million, which is $17 million less than the

unadjusted risk-free mark-to-market net liability value.

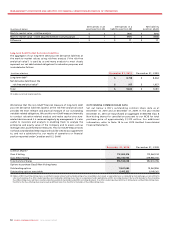

Consolidated Hedged Position

(In millions of dollars, except percentages) December 31, 2010 December 31, 2009

U.S. dollar-denominated long-term debt US $ 5,050 US $ 5,540

Hedged with Derivatives US $ 5,050 US $ 5,540

Hedged exchange rate 1.1697 1.2043

Percent hedged(1) 100.0% 100.0%

Amount of long-term debt(2) at fixed rates:

Total long-term debt Cdn $ 9,607 Cdn $ 9,307

Total long-term debt at fixed rates Cdn $ 9,607 Cdn $ 9,307

Percent of long-term debt fixed 100.0% 100.0%

Weighted average interest rate on long-term debt 6.68% 7.27%

(1) Pursuant to the requirements for hedge accounting under Canadian Institute of Chartered Accountants (“CICA”) Handbook Section 3865, Hedges, on December 31, 2010, RCI accounted for 93.1% of its

Derivatives as hedges against designated U.S. dollar-denominated debt. As a result, 93.1% of our U.S. dollar-denominated debt is hedged for accounting purposes versus 100% on an economic basis.

(2) Long-term debt includes the effect of the Derivatives.

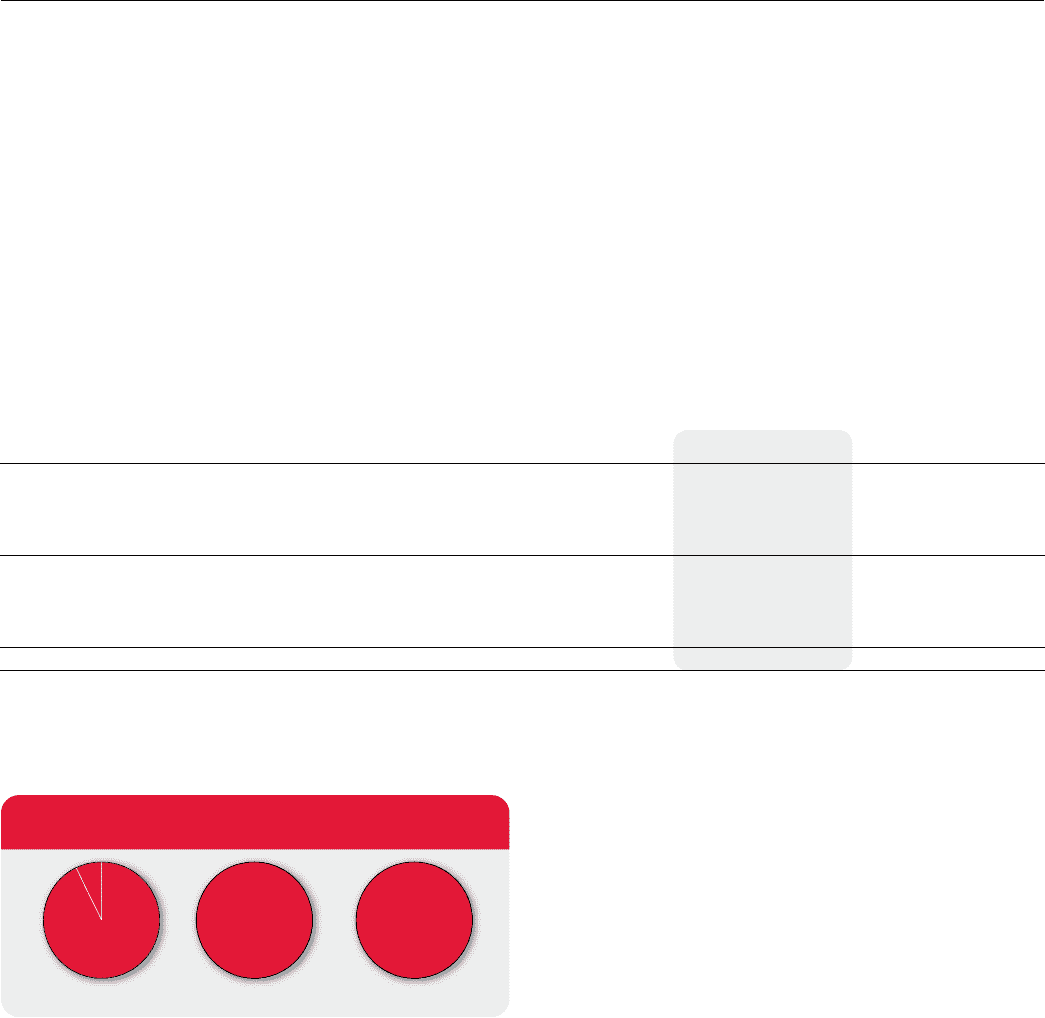

Fixed 100% Floating 0%Fixed 100% Floating 0%Fixed 93% Floating 7%

FIXED VERSUS FLOATING DEBT COMPOSITION

(% at December 31)

201020092008