Pizza Hut 2008 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2008 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

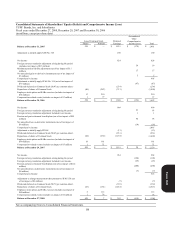

|

|

67

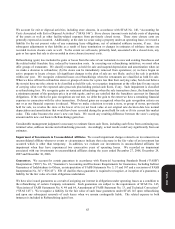

The recognition and disclosure requirements of SFAS 158 required the Company to recognize the funded status of its

pension and post-retirement plans in the December 30, 2006 Consolidated Balance Sheet, with a corresponding

adjustment to Accumulated other comprehensive income (loss), net of tax. The impact of adopting these provisions of

SFAS 158 was an after tax reduction of Shareholders’ Equity (Deficit) of $67 million in 2006. Subsequent to the adoption

of SFAS 158, gains or losses and prior service costs or credits are being recognized as they arise as a component of other

comprehensive income (loss) to the extent they have not been recognized as a component of net periodic benefit cost

pursuant to SFAS No. 87, “Employers’ Accounting for Pensions,” or SFAS No. 106, “Employers’ Accounting for

Postretirement Benefits Other Than Pensions”. In the fourth quarter of 2008, we adopted the measurement date

provisions of SFAS 158 and recorded a decrease to Retained Earnings of $9 million, or $6 million after tax, for our

pension plans and $2 million, or $1 million after tax, for our post-retirement medical plan, respectively.

Quantification of Misstatements. In September 2006, the Securities and Exchange Commission (the “SEC”) issued

Staff Accounting Bulletin No. 108, “Considering the Effects of Prior Year Misstatements when Quantifying

Misstatements in Current Year Financial Statements” (“SAB 108”). SAB 108 provides interpretive guidance on how the

effects of the carryover or reversal of prior year misstatements should be considered in quantifying a current year

misstatement for the purpose of a materiality assessment. SAB 108 requires that registrants quantify a current year

misstatement using an approach that considers both the impact of prior year misstatements that remain on the balance

sheet and those that were recorded in the current year income statement (the “Dual Method”). Historically, we quantified

misstatements and assessed materiality based on a current year income statement approach. We were required to adopt

SAB 108 in the fourth quarter of 2006.

The transition provisions of SAB 108 permitted uncorrected prior year misstatements that were not material to any prior

periods under our historical income statement approach but that would have been material under the dual method of SAB

108 to be corrected in the carrying amounts of assets and liabilities at the beginning of 2006 with the offsetting adjustment

to retained earnings for the cumulative effect of misstatements. We have adjusted certain balances in the accompanying

Consolidated Financial Statements at the beginning of 2006 to correct the misstatements discussed below which we

considered to be immaterial in prior periods under our historical approach. The impact of the January 1, 2006 cumulative

effect adjustment, net of any income tax effect, was an increase to retained earnings as follows:

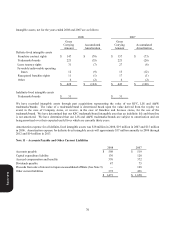

Deferred Tax Liabilities Adjustments $ 79

Reversal of Unallocated Reserve 6

Non-GAAP Conventions 15

Net Increase to January 1, 2006 Retained Earnings $ 100

Deferred Taxes Our opening Consolidated Balance Sheet at Spin-off included significant deferred tax assets and

liabilities. Over time we have determined that deferred tax liability amounts were recorded in excess of those necessary to

reflect our temporary differences.

Unallocated Reserves A reserve was established in 1999 equal to certain out of year corrections recorded during that year

such that there was no misstatement under our historical approach. No adjustments have been recorded to this reserve

since its establishment and we do not believe the reserve is required.

Non-GAAP Accounting Conventions Prior to 2006, we used certain non-GAAP conventions to account for capitalized

interest on restaurant construction projects, the leases of our then Pizza Hut United Kingdom (“U.K.”) unconsolidated

affiliate and certain state tax benefits. The net income statement impact on any given year from the use of these non-

GAAP conventions was immaterial both individually and in the aggregate under our historical approach. Below is a

summary of the accounting policies we adopted effective the beginning of 2006 and the impact of the cumulative effect

adjustment under SAB 108, net of any income tax effect.

Interest Capitalization SFAS No. 34, “Capitalization of Interest Cost” requires that interest be capitalized as part of an

asset’s acquisition cost. We traditionally have not capitalized interest on individual restaurant construction projects. We

increased our 2006 beginning retained earnings balance by approximately $12 million for the estimated capitalized

interest on existing restaurants, net of accumulated depreciation.

Form 10-K