Neiman Marcus 2004 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2004 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

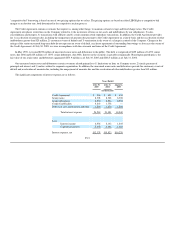

Certificate, the Class C Certificate, the Seller's Certificate and the IO Strip were subordinated to the rights of the holders of the Class A Certificates. As a

result, the credit quality of the Class A Certificates was enhanced, thereby lowering the interest cost paid by the Trust on the Class A Certificates. Recourse to

the Company with respect to the sale of assets was limited to our Retained Interests.

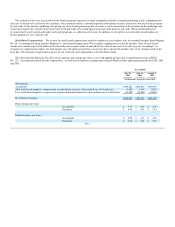

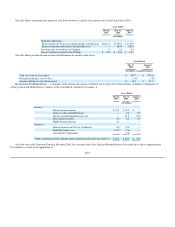

Under the Credit Card Facility, we serviced the credit card receivables for a contractually defined servicing fee. We earned servicing fees of $5.4 million

in 2005 and $6.3 million in both 2004 and 2003.

In connection with Off-Balance Sheet Accounting, our Retained Interests were shown as "Undivided interests in NMG Credit Card Master Trust" on our

consolidated balance sheets. The certificates representing the Retained Interests were securities that we intended to "hold to maturity" and were carried at

amortized cost of $231.6 million at August 2, 2003. The IO Strip was treated as an "available-for-sale" security and was carried at its estimated fair value of

$11.5 million at August 2, 2003. In determining the fair value of the Retained Interests at August 2, 2003, the key economic assumptions used were 1) a

weighted average life of receivables of 4 months, 2) expected annual credit losses of 0.79%, 3) a net interest spread of 16.36% and 4) a weighted average

discount rate of 5.95%. Changes in the fair value of the IO Strip were reflected as a component of other comprehensive income. Income was recorded on the

Retained Interests and the IO Strip on the basis of their estimated effective yield to maturity and was recorded as a reduction of selling, general and

administrative expenses.

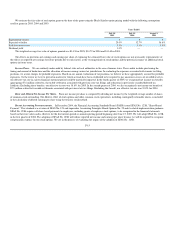

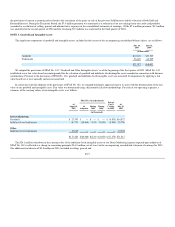

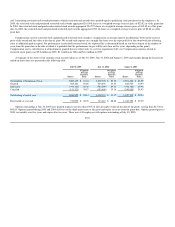

Transfers to the Trust ceased to qualify for Off-Balance Sheet Accounting beginning in December 2003 since the receivables transferred after

November 2003 were subject to our future repurchase based upon the provisions of the Credit Card Facility. Rather, these transfers were recorded as secured

borrowings (Financing Accounting). As a consequence, the credit card receivables generated after November 2003 remained on our balance sheet as assets

and the portions of Class A Certificates that funded such receivables were reflected as a liability. The transition period from Off-Balance Sheet Accounting to

Financing Accounting (Transition Period) lasted approximately four months (December 2003 to March 2004). During the Transition Period, cash collections

of receivables were allocated to the previous Sold Interests and Retained Interests until such time as those balances were reduced to zero. By the end of the

Transition Period, our entire credit card portfolio was included in accounts receivable in our consolidated balance sheet and the $225.0 million repayment

obligation was shown as a liability.

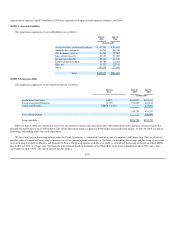

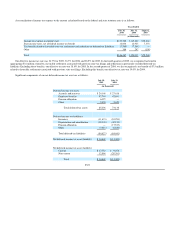

Beginning in April 2005, cash collections were used by the Trust to repay the $225.0 million principal balance of the Class A Certificates in six monthly

installments of $37.5 million (Amortization Period). Prior to the Credit Card Sale, we had repaid $112.5 million of the principal balance of the Class A

Certificates and had placed $40.7 million on deposit with the Trust to fund future repayment obligations. In connection with the Credit Card Sale, HSBC

assumed the remaining obligations related to the outstanding Class A Certificates.

F-17