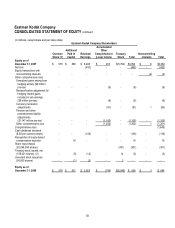

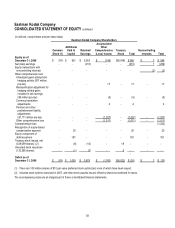

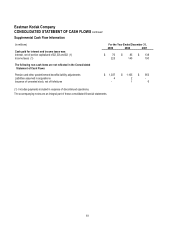

Kodak 2009 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2009 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

68

Recently Issued Accounting Pronouncements

In January 2010, the Financial Accounting Standards Board (FASB) issued Accounting Standards Updated (ASU) No. 2010-06,

“Improving Disclosures about Fair Value Measurements,” which amends the Accounting Standards Codification (ASC) Topic 820,

“Fair Value Measures and Disclosures.” ASU No. 2010-06 amends the ASC to require disclosure of transfers into and out of Level 1

and Level 2 fair value measurements, and also require more detailed disclosure about the activity within Level 3 fair value

measurements. The changes to the ASC as a result of this update are effective for annual and interim reporting periods beginning

after December 15, 2009 (January 1, 2010 for the Company), except for requirements related to Level 3 disclosures, which are

effective for annual and interim reporting periods beginning after December 15, 2010 (January 1, 2011 for the Company). This

guidance requires new disclosures only, and will have no impact on the Company’s Consolidated Financial Statements.

In October 2009, the FASB issued ASU No. 2009-13, "Multiple-Deliverable Revenue Arrangements," which amends ASC Topic 605,

"Revenue Recognition.” ASU No. 2009-13 amends the ASC to eliminate the residual method of allocation for multiple-deliverable

revenue arrangements, and requires that arrangement consideration be allocated at the inception of an arrangement to all

deliverables using the relative selling price method. The ASU also establishes a selling price hierarchy for determining the selling

price of a deliverable, which includes: (1) vendor-specific objective evidence if available, (2) third-party evidence if vendor-specific

objective evidence is not available, and (3) estimated selling price if neither vendor-specific nor third-party evidence is available.

Additionally, ASU No. 2009-13 expands the disclosure requirements related to a vendor's multiple-deliverable revenue

arrangements. The changes to the ASC as a result of this update are effective prospectively for revenue arrangements entered into

or materially modified in fiscal years beginning on or after June 15, 2010 (January 1, 2011 for the Company), and the Company is

currently evaluating the potential impact, if any, of the adoption on its Consolidated Financial Statements.

In October 2009, the FASB issued ASU No. 2009-14, "Certain Revenue Arrangements That Include Software Elements," which

amends ASC Topic 985, "Software.” ASU No. 2009-14 amends the ASC to change the accounting model for revenue arrangements

that include both tangible products and software elements, such that tangible products containing both software and non-software

components that function together to deliver the tangible product's essential functionality are no longer within the scope of software

revenue guidance. The changes to the ASC as a result of this update are effective prospectively for revenue arrangements entered

into or materially modified in fiscal years beginning on or after June 15, 2010 (January 1, 2011 for the Company), and the Company

is currently evaluating the potential impact, if any, of the adoption on its Consolidated Financial Statements.

In June 2009, the FASB issued revised authoritative guidance related to variable interest entities, which requires entities to perform a

qualitative analysis to determine whether a variable interest gives the entity a controlling financial interest in a variable interest entity.

The guidance also requires an ongoing reassessment of variable interests and eliminates the quantitative approach previously

required for determining whether an entity is the primary beneficiary. This guidance, which was reissued by the FASB in December

2009 as ASU No. 2009-17, “Improvements to Financial Reporting by Enterprises Involved with Variable Interest Entities,” amends

ASC Topic 810, “Consolidation,” and will be effective as of the beginning of an entity’s first annual reporting period that begins after

November 15, 2009 (January 1, 2010 for the Company). The Company does not expect that the adoption of this guidance will have a

significant impact on its Consolidated Financial Statements.

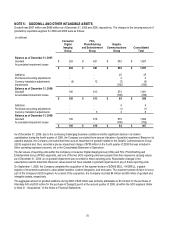

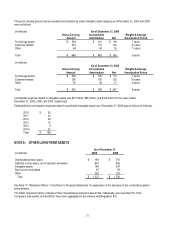

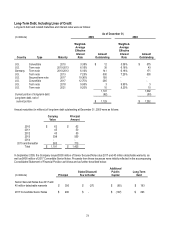

NOTE 2: RECEIVABLES, NET

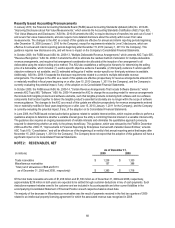

As of December 31,

(in millions) 2009 2008

Trade receivables $ 1,238 $ 1,330

Miscellaneous receivables 157 386

Total (net of allowances of $98 and $113

as of December 31, 2009 and 2008, respectively) $ 1,395 $ 1,716

Of the total trade receivable amounts of $1,238 million and $1,330 million as of December 31, 2009 and 2008, respectively,

approximately $218 million in both years are expected to be settled through customer deductions in lieu of cash payments. Such

deductions represent rebates owed to the customer and are included in Accounts payable and other current liabilities in the

accompanying Consolidated Statement of Financial Position at each respective balance sheet date.

The majority of the decrease in Miscellaneous receivables was the result of payments received in the first two quarters of 2009

related to an intellectual property licensing agreement for which the associated revenue was recognized in 2008.