Kodak 2009 Annual Report Download - page 227

Download and view the complete annual report

Please find page 227 of the 2009 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

83

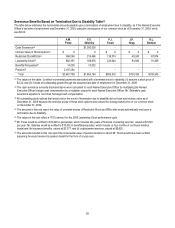

Severance Benefits Based on Termination Due to Death Table(1)

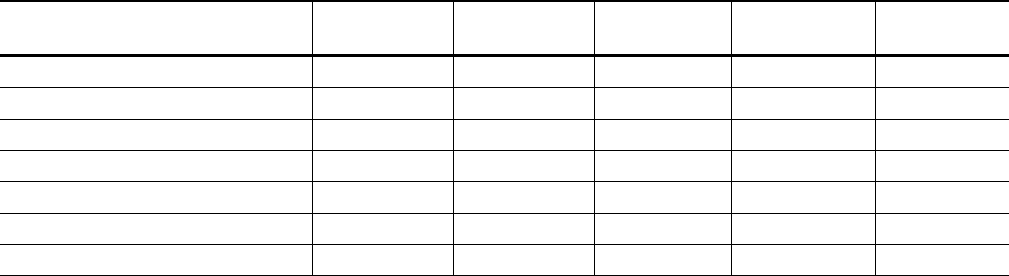

The table below estimates the incremental amounts payable upon a termination of employment due to death, as if the Named Executive

Officer’s last date of employment was December 31, 2009, using the closing price of our common stock as of December 31, 2009, which

was $4.22.

A.M.

Perez

F.S.

Sklarsky

P.J.

Faraci

J.P.

Haag

R.L.

Berman

Cash Severance

—

—

—

—

—

Intrinsic Value of Stock Options(2)

$ 0

$ 0

$ 0

$ 0

$ 0

Restricted Stock/RSUs(3)

568,084

216,486

139,374

49,240

67,874

Leadership Stock(4)

682,391

188,676

224,044

84,940

91,469

Benefits/Perquisites(5)

14,000

—

—

—

—

Pension (6)

2,197,284

—

—

—

—

Total

$3,461,759

$405,162

$363,418

$134,180

$159,343

(1) The values in this table: (i) reflect incremental payments associated with a termination due to death; (ii) assume a stock price of

$4.22; and (iii) include all outstanding grants through the assumed last date of employment of December 31, 2009.

(2) All outstanding stock options that would vest in the event of a termination due to death did not have any intrinsic value as of

December 31, 2009 because the exercise prices of these stock options were above the closing market price of our common stock

on December 31, 2009.

(3) The values in this row report the value of unvested shares of Restricted Stock and RSUs that would automatically vest upon a

termination due to death.

(4) The values in this row reflect a 170% earnout for the 2009 Leadership Stock performance cycle.

(5) Mr. Perez's estate would be entitled to $14,000 in perquisites, which represents two years of financial counseling services, valued

at $7,000 per year.

(6) The amounts included in this row report the incremental value of pension benefits to which Mr. Perez would have been entitled

assuming he would receive his pension benefit in the form of a lump sum.