Holiday Inn 2012 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2012 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

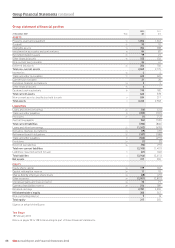

92 IHG Annual Report and Financial Statements 2012

Cash and cash equivalents

Cash comprises cash in hand and demand deposits.

Cash equivalents are short-term highly liquid investments with an

original maturity of three months or less that are readily convertible

to known amounts of cash and subject to insignificant risk of

changes in value.

In the statement of cash flows, cash and cash equivalents are shown

net of short-term overdrafts which are repayable on demand and

form an integral part of the Group’s cash management.

Assets held for sale

Non-current assets and associated liabilities are classified as held

for sale when their carrying amount will be recovered principally

through a sale transaction rather than continuing use and a sale

is highly probable.

Assets designated as held for sale are held at the lower of carrying

amount at designation and fair value less costs to sell.

Depreciation is not charged against property, plant and equipment

classified as held for sale.

Financial liabilities

Financial liabilities are measured at amortised cost using the effective

interest rate method. A financial liability is derecognised when the

obligation under the liability expires, is discharged or cancelled.

Trade payables

Trade payables are non-interest-bearing and are stated at their

nominal value.

Bank and other borrowings

Bank and other borrowings are initially recognised at the fair value

of the consideration received less directly attributable transaction

costs. They are subsequently measured at amortised cost. Finance

charges, including the transaction costs and any discount or

premium on issue, are recognised in the income statement using

the effective interest rate method.

Borrowings are classified as non-current when the repayment date

is more than 12 months from the period-end date or where they are

drawn on a facility with more than 12 months to expiry.

Derivative financial instruments and hedging

Derivatives are initially recognised and subsequently remeasured

at fair value. The method of recognising the remeasurement

depends on whether the derivative is designated as a hedging

instrument, and if so, the nature of the item being hedged.

Changes in the fair value of derivatives designated as cash flow

hedges are recorded in other comprehensive income and the

unrealised gains and losses reserve to the extent that the hedges

are effective. When the hedged item is recognised, the cumulative

gains and losses on the related hedging instrument are reclassified

to the income statement.

Changes in the fair value of derivatives designated as net

investment hedges are recorded in other comprehensive income

and the currency translation reserve to the extent that the hedges

are effective. The cumulative gains and losses remain in equity

until a foreign operation is sold, at which point they are reclassified

to the income statement.

Changes in the fair value of derivatives which have either not been

designated as hedging instruments or relate to the ineffective portion

of hedges are recognised immediately in the income statement.

Documentation outlining the measurement and effectiveness of

any hedging arrangements is maintained throughout the life of the

hedge relationship.

Interest arising from currency derivatives and interest rate swaps

is recorded in either financial income or expenses over the term of

the agreement, unless the accounting treatment for the hedging

relationship requires the interest to be taken to reserves.

Self insurance

Liabilities in respect of self insured risks include projected

settlements for known and incurred but not reported claims.

Projected settlements are estimated based on historical trends

and actuarial data.

Provisions

Provisions are recognised when the Group has a present obligation

as a result of a past event, it is probable that a payment will be

made and a reliable estimate of the amount payable can be made.

If the effect of the time value of money is material, the provision

is discounted.

An onerous contract provision is recognised when the unavoidable

costs of meeting the obligations under a contract exceed the

economic benefits expected to be received under it.

In respect of litigation, provision is made when management

consider it probable that payment may occur even though the

defence of the related claim may still be ongoing through the

court process.

Taxes

Current tax

Current income tax assets and liabilities for the current and prior

periods are measured at the amount expected to be recovered from

or paid to the tax authorities including interest. The tax rates and

tax laws used to compute the amount are those that are enacted

or substantively enacted by the end of the reporting period.

Deferred tax

Deferred tax assets and liabilities are recognised in respect

of temporary differences between the tax base and carrying value

of assets and liabilities including accelerated capital allowances,

unrelieved tax losses, unremitted profits from overseas where

the Group does not control remittance, gains rolled over into

replacement assets, gains on previously revalued properties and

other short-term temporary differences.

Accounting policies continued