Holiday Inn 2012 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2012 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

112 IHG Annual Report and Financial Statements 2012

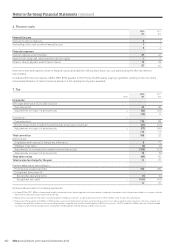

Notes to the Group Financial Statements continued

A general strengthening of the US dollar (specifically a five cent

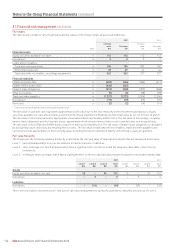

fall in the sterling:US dollar rate) would increase the Group’s profit

before tax by an estimated $2.8m (2011 $3.3m) and increase net

assets by an estimated $1.8m (2011 decrease of $10.4m). Similarly,

a five cent fall in the euro:US dollar rate would reduce the Group’s

profit before tax by an estimated $2.3m (2011 $1.9m) and decrease

net assets by an estimated $16.1m (2011 $10.3m).

Interest rate exposure is managed within parameters that stipulate

that fixed rate borrowings should normally account for no less

than 25% and no more than 75% of net borrowings for each major

currency. This is usually achieved through the use of interest rate

swaps. Due to relatively low interest rates and the level of the

Group’s debt, 100% of borrowings in major currencies were fixed

rate debt at 31 December 2012.

Based on the year-end net debt position and given the underlying

maturity profile of investments, borrowings and hedging instruments

at that date, neither a one percentage point rise in US dollar, euro nor

sterling interest rates would impact the annual net interest charge

in the current or prior year.

Liquidity risk exposure

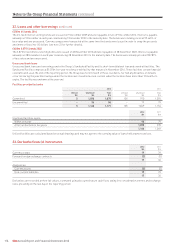

The treasury function ensures that the Group has access to

sufficient funds to allow the implementation of the strategy set

by the Board. Medium and long-term borrowing requirements

are met through the $1.07bn Syndicated Facility which expires in

November 2016, through the £250m 6% bonds that are repayable

on 9 December 2016 and through the £400m 3.875% bonds

repayable on 28 November 2022. The $1.07bn Syndicated Facility

was undrawn at the year end. The £400m 3.875% bonds, which

were issued during the year under the Group’s £750m Medium

Term Notes programme, extend the maturity profile and diversify

the sources of the Group’s debt. Short-term borrowing

requirements are met from drawings under bilateral bank facilities.

The Syndicated Facility contains two financial covenants: interest

cover and net debt divided by earnings before interest, tax,

depreciation and amortisation (EBITDA). The Group is in

compliance with all of the financial covenants in its loan documents,

none of which is expected to present a material restriction on

funding in the near future.

At the year end, the Group had cash of $195m which is

predominantly held in short-term deposits and cash funds which

allow daily withdrawals of cash. Most of the Group’s funds are

held in the UK or US, although $7m (2011 $2m) is held in a

country where repatriation is restricted as a result of foreign

exchange regulations.

Credit risk exposure

Credit risk on treasury transactions is minimised by operating a

policy on the investment of surplus cash that generally restricts

counterparties to those with an A credit rating or better or those

providing adequate security.

Notwithstanding that counterparties must have an A credit rating

or better, during periods of significant financial market turmoil,

counterparty exposure limits are significantly reduced and

counterparty credit exposure reviews are broadened to include

the relative placing of credit default swap pricings.

The Group trades only with recognised, creditworthy third parties.

It is the Group’s policy that all customers who wish to trade on credit

terms are subject to credit verification procedures.

In respect of credit risk arising from financial assets, the Group’s

exposure to credit risk arises from default of the counterparty,

with a maximum exposure equal to the carrying amount of

these instruments.

Capital risk management

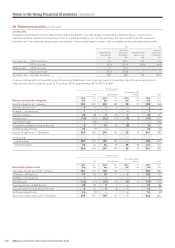

The Group manages its capital to ensure that it will be able to

continue as a going concern. The capital structure consists of

net debt, issued share capital and reserves totalling $1,382m at

31 December 2012 (2011 $1,085m). The structure is managed to

maintain an investment grade credit rating, to provide ongoing

returns to shareholders and to service debt obligations, whilst

maintaining maximum operational flexibility. A key characteristic

of IHG’s managed and franchised business model is that it is highly

cash generative, with a high return on capital employed. Surplus

cash is either reinvested in the business, used to repay debt or

returned to shareholders. The Group’s debt is monitored on the

basis of a cash flow leverage ratio, being net debt divided by

EBITDA, with the objective of maintaining an investment grade

credit rating.

Hedging

Interest rate risk

The Group hedges its interest rate risk by taking out interest rate

swaps to fix the interest flows on between 25% and 75% of its net

borrowings in major currencies, although 100% of interest flows

were fixed at 31 December 2012. At 31 December 2012, the Group

did not hold any interest rate swaps (2011 notional principals held

of $100m swapping floating for fixed). The Group designates

its interest rate swaps as cash flow hedges (see note 23 for

further details).

Foreign currency risk

The Group is exposed to foreign currency risk on income streams

denominated in foreign currencies. From time to time, the Group

hedges a portion of forecast foreign currency income by taking out

forward exchange contracts. The designated risk is the spot foreign

exchange risk. There were no such contracts in place at either

31 December 2012 or 31 December 2011.

Hedge of net investment in foreign operations

The Group designates its foreign currency bank borrowings

and currency derivatives as net investment hedges of foreign

operations. The designated risk is the spot foreign exchange

risk for loans and short dated derivatives and the forward risk

for the seven-year currency swaps. The interest on these financial

instruments is taken through financial income or expense except

for the seven-year currency swaps where interest is taken to the

currency translation reserve.

At 31 December 2012, the Group held currency swaps with a

principal of $415m (2011 $415m) and short dated foreign exchange

swaps with principals of EUR75m (2011 EUR75m) and USD170m

(2011 USD nil) (see note 23 for further details). The maximum

amount of foreign exchange derivatives held during the year as net

investment hedges and measured at calendar quarter ends were

currency swaps with a principal of $415m (2011 $415m) and short

dated foreign exchange swaps with principals of EUR75m (2011

EUR100m) and USD350m (2011 USD100m).

Hedge effectiveness is measured at calendar quarter ends.

No ineffectiveness arose in respect of either the Group’s cash

flow or net investment hedges during the current or prior year.

21. Financial risk management continued