Comcast 2015 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2015 Comcast annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

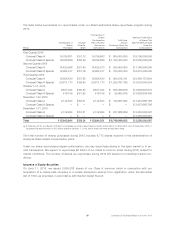

|

|

While our cable communications business is attempting to adapt to changing consumer behaviors, for exam-

ple, by deploying our X1 platform and Cloud DVR technology, products and services have emerged that

compete with our video services, including those that offer subscription video on demand services or the abil-

ity to download content that can be viewed on television sets, computers, smartphones and tablets. Some of

these products and services charge no fee or a lower fee than our traditional video packages for access to

their content, which adversely affects demand for our video services, including for expanded digital video

packages, premium networks, and our DVR and On Demand services.

The increased availability of these products and services, including some that also offer high-quality original

video programming that is exclusive to that service, have contributed to an increased number of entertain-

ment choices available to consumers, which intensifies audience fragmentation. Additionally, the increased

availability of DVRs and cloud-based recording services and video on demand services reduces the viewing

of content through traditional linear television distribution outlets. Reduced viewing of our content through

traditional linear television distribution outlets has caused and will likely continue to cause audience ratings

declines for NBCUniversal’s linear television content and may adversely affect the price and amount of adver-

tising that advertisers are willing to purchase from us and the amount NBCUniversal receives for distribution

of its content.

Additionally, several companies now offer smaller packages of channels directly to customers over the Inter-

net at price points lower than our standard packages, which could adversely affect demand for our video

services and reduce the subscription revenue that our cable networks or broadcast television businesses

receive from multichannel video providers. These smaller packages could also cause our cable communica-

tions business to offer more customized programming packages that may be less profitable.

The success of any of these ongoing and future developments or our failure to effectively anticipate or adapt

to emerging competitors or changes in consumer behavior, including among younger consumers, could have

an adverse effect on our competitive position, businesses and results of operations.

A decline in advertisers’ expenditures or changes in advertising markets could negatively impact

our businesses.

Our cable communications, cable networks and broadcast television businesses compete for the sale of

advertising time with other television networks and stations, as well as with all other advertising platforms,

such as radio, print and, increasingly, digital media. We derive substantial revenue from the sale of advertis-

ing, and a decline in expenditures by advertisers, including through traditional linear television distribution

models, could negatively impact our results of operations. Declines can be caused by the economic pros-

pects of specific advertisers or industries, increased competition for the leisure time of audiences and

audience fragmentation, by the growing use of new technologies, or the economy in general. In addition,

advertisers’ willingness to purchase advertising from us may be adversely affected by lower audience ratings,

which some of our networks have experienced and likely will continue to experience. Advertising sales and

rates also are dependent on audience measurement methodologies and could be negatively affected if meth-

odologies do not accurately reflect actual viewership levels. For example, certain methods of viewing content,

such as delayed viewing on DVRs or viewing content online, might not be counted in audience measurements

or may generate less, if any, revenue than traditional distribution methods, which could have an adverse

effect on our advertising revenue. Reductions in advertisers’ expenditures could adversely affect our revenue

and businesses.

Our businesses depend on keeping pace with technological developments.

Our success is, to a large extent, dependent on our ability to acquire, develop, adopt and leverage new and

existing technologies, and our competitors’ use of certain types of technology and equipment may provide

27 Comcast 2015 Annual Report on Form 10-K