Chrysler 2011 Annual Report Download - page 379

Download and view the complete annual report

Please find page 379 of the 2011 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

369 -

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

|

|

Motions

for AGM

378

9.2 Precedent Conversion Transactions Analysis

In determining the proposed conversion ratios, the Board of Directors first considered a group of compulsory conversions of preference and savings

shares on the Italian market between 1999 and the transaction announcement.

Such transactions have several common features: in most cases the transactions had a limited value4, converted shares represented a limited portion of

total share capital and converted shares had a low trading liquidity. For these reasons, the Board has considered the empirical evidence resulting from the

analysis not meaningful in determining the Conversion ratios.

The Board then identified a subset of such precedents deemed more relevant due to the more meaningful volume of historical trading in the converted

shares. With respect to such precedents, the Board observed that, on average, implied premium to special shareholders has been approximately 24%

calculated with respect to the converted share average prices in the three months preceding the announcement.

For the purpose of calculating the implied premia paid in precedent transactions, the Board of Directors used a three month period to calculate the

converted class average historical share price in order to mitigate the impact of potential speculations and rumours close to the announcement date that

might have affected the share price.

9.3 Implied Premia in the Proposed Conversion Ratios

Preference shares will be converted into newly issued ordinary shares at a conversion ratio of 0.850 ordinary shares for each preference share. Savings

shares will be converted into newly issued ordinary shares according to a conversion ratio of 0.875 ordinary shares for each savings share.

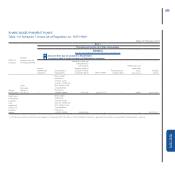

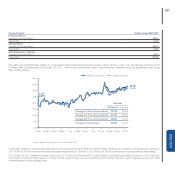

The table below shows the premia implied in the conversion ratios with respect to closing prices on October 26, 2011 and with respect to the average

prices different time horizons.

Premium Analysis Preference Savings Delta Pref vs. Sav

Announced Conversion Ratio 0.850 x 0.875 x (0.025)

Discount vs. Ordinary Shares

Share Price as of 26-October

Discount vs. Ordinary Shares

Implied Conversion Ratio

15.0%

3.24

33.7%

0.663

12.5%

3.34

31.6%

0.684

2.5%

(0.10)

2.1%

(0.021)

Premium Offered 28.2% 27.9% 0.3%

Average Share Price - Last 3 Months

Discount vs. Ordinary Shares

Implied Conversion Ratio

3.15

35.4%

0.646

3.21

34.2%

0.658

(0.06)

1.2%

(0.012)

Premium Offered 31.6% 33.0% (1.4)%

Discount vs. Ordinary Shares 2001-2010

Implied Conversion Ratio 2001-2010

30.8%

0.692

28.2%

0.718

2.5%

(0.025)

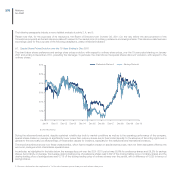

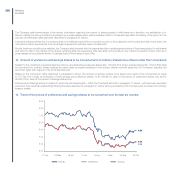

Special shareholders would receive an implied premium in excess of 30% calculated on the basis of the three months average price of the special share

classes pre-announcement. This premium favourably compares with premia paid in precedent transactions and aligns special classes of shares to a

discount with respect to ordinary shares well below the 10 years prior to the Demerger.

Furthermore, the Board has taken into consideration the greater economic rights of the savings shares compared to preference shares. Historically, such

greater rights have been reflected in a higher trading price of the savings shares (and hence a lower discount to ordinary shares) when compared to the

preference shares. In the 10 years period prior to the Demerger, the implied ratio of savings shares to ordinary shares has been 0.025 greater than the

implied ratio of preference shares to ordinary shares based on trading prices. Based on the closing prices on October 26, 2011 the implied ratio of savings

shares to ordinary shares was 0.021 greater than the implied ratio of preference shares to ordinary shares. In determining the conversion ratios, the Board

has determined to align this differential to the 2001-2010 average of 0.025.

4 Defined as the number of special shares subject to compulsory conversion, multiplied by the latest closing price before the announcement.