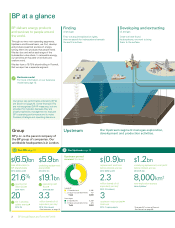

BP 2015 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2015 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

Our markets in 2015

See page 24 for information on oil and gas

prices in 2015.

Near-term outlook

The global economy continues to experience

weaker growth in the main developing

economies and slower than expected recovery

in the developed world. World gross domestic

product (GDP) is expected to grow by 2.8% in

2016, led by the OECD, but with significant

downside risks from emerging economies,

particularly commodity exporters.

After around four years of averaging about $100

per barrel, oil prices fell by nearly 50% in 2015.

Even as US production growth stalled and global

oil demand rebounded, a large increase in OPEC

production continued to push inventories higher.

Price declines continued into early 2016, with

daily prices reaching levels not seen since 2004.

Prices are expected to remain low at least

through the near term. And while we anticipate

supply chain deflation in 2016 and beyond, as

industry costs follow oil prices with a lag, this

will be a tough period of intense change for the

industry as it adapts to this new reality.

Long-term outlook

The world economy is likely to more than double

from 2014 to 2035, largely driven by rising

incomes in the emerging economies and a

projected population increase of 1.5 billion.

We expect world demand for energy to increase

by as much as 34% between 2014 and 2035.

This is after taking into account improvements in

energy efficiency, a shift towards less energy-

intensive activities in fast-growing economies,

governmental policies that incentivize lower-

carbon activity, and national pledges made at the

2015 UN climate conference in Paris.

There are more than enough energy resources

to meet this growing demand, but there are a

number of challenges.

We believe that a diverse mix of fuels and technologies will

be essential to meet the growing demand for energy and

challenges facing our industry.

Our market outlook

G

lobal energy consumption by region

(

billion tonnes of oil equivalent)

2035

18

16

14

12

10

8

6

4

2

1965 2000

Other ChinaOther Asia

OECD

Affordability

Fossil fuels are currently cheaper than

renewables but their future costs are hard to

predict. Some fossil fuels may become more

costly as the difficulty to access and process

them increases; others may be more affordable

with technological progress, as seen with US

shale gas. While many renewables remain

expensive, innovation and wider deployment are

likely to bring down their costs.

Supply security

Energy resources are often distant from the

hubs of energy consumption and in places

facing political uncertainties. More than half of

the world’s known oil and natural gas reserves

are located in just eight countries.

Sustainability

Fossil fuels – though plentiful and currently more

affordable than other energy resources – emit

carbon dioxide (CO2) and other greenhouse

gases (GHG) through their production and use in

homes, industry and vehicles. Renewables are

lower carbon but can have other environmental

or social impacts, such as high water

consumption or visual intrusion.

Effective policy

BP believes that carbon pricing is the most

comprehensive and economically efficient policy

to limit GHG emissions. Putting a price on

carbon – one that treats all carbon equally,

whether it comes out of a smokestack or a car

exhaust – would make energy efficiency more

attractive and lower-carbon energy sources,

such as natural gas and renewables, more cost

competitive. A carbon price incentivizes both

energy producers and consumers to reduce their

GHG emissions. Governments can put a price

on carbon via a well-constructed carbon tax or

cap-and-trade system.

For further detail on our projections of future

energy trends contained in this section,

please refer to BP Energy Outlook.

Source: BP Energy Outlook.

BP Annual Report and Form 20-F 201510