BP 2015 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2015 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

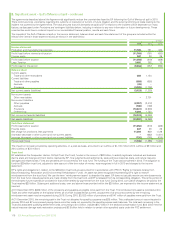

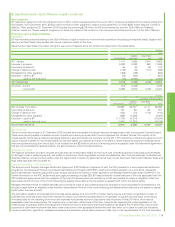

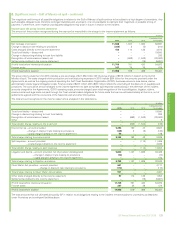

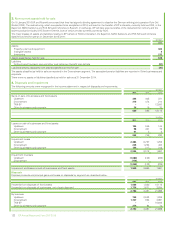

1. Significant accounting policies, judgements, estimates and assumptions – continued

liability and are charged directly against income. Capitalized leased assets are depreciated over the shorter of the estimated useful life of the asset or

the lease term.

Operating lease payments are recognized as an expense on a straight-line basis over the lease term.

Financial assets

Financial assets are recognized initially at fair value, normally being the transaction price plus, in the case of financial assets not at fair value through

profit or loss, directly attributable transaction costs. The subsequent measurement of financial assets depends on their classification, as follows:

Loans and receivables

Loans and receivables are carried at amortized cost using the effective interest method if the time value of money is significant. Gains and losses are

recognized in income when the loans and receivables are derecognized or impaired, as well as through the amortization process. This category of

financial assets includes trade and other receivables. Cash equivalents are short-term highly liquid investments that are readily convertible to known

amounts of cash, are subject to insignificant risk of changes in value and have a maturity of three months or less from the date of acquisition.

Financial assets at fair value through profit or loss

Financial assets at fair value through profit or loss are carried on the balance sheet at fair value with gains or losses recognized in the income

statement. Derivatives, other than those designated as effective hedging instruments, are classified as held for trading and are included in this

category.

Derivatives designated as hedging instruments in an effective hedge

These derivatives are carried on the balance sheet at fair value. The treatment of gains and losses arising from revaluation is described below in the

accounting policy for derivative financial instruments and hedging activities.

Held-to-maturity financial assets

Held-to-maturity financial assets are measured at amortized cost, using the effective interest method, less any impairment.

Available-for-sale financial assets

Available-for-sale financial assets are measured at fair value, with gains or losses recognized within other comprehensive income, except for

impairment losses, and, for available-for-sale debt instruments, foreign exchange gains or losses, interest recognized using the effective interest

method, and any changes in fair value arising from revised estimates of future cash flows, which are recognized in profit or loss.

Impairment of loans and receivables

The group assesses at each balance sheet date whether a financial asset or group of financial assets is impaired. If there is objective evidence that an

impairment loss on loans and receivables carried at amortized cost has been incurred, the amount of the loss is measured as the difference between

the asset’s carrying amount and the present value of estimated future cash flows discounted at the financial asset’s original effective interest rate. The

carrying amount of the asset is reduced, with the amount of the loss recognized in the income statement.

Significant estimate or judgement: recoverability of trade receivables

Judgements are required in assessing the recoverability of overdue trade receivables and determining whether a provision against those receivables

is required. Factors considered include the credit rating of the counterparty, the amount and timing of anticipated future payments and any possible

actions that can be taken to mitigate the risk of non-payment. See Note 28 for information on overdue receivables.

Financial liabilities

The measurement of financial liabilities depends on their classification, as follows:

Financial liabilities at fair value through profit or loss

Financial liabilities at fair value through profit or loss are carried on the balance sheet at fair value with gains or losses recognized in the income

statement. Derivatives, other than those designated as effective hedging instruments, are classified as held for trading and are included in this

category.

Derivatives designated as hedging instruments in an effective hedge

These derivatives are carried on the balance sheet at fair value. The treatment of gains and losses arising from revaluation is described below in the

accounting policy for derivative financial instruments and hedging activities.

Financial liabilities measured at amortized cost

All other financial liabilities are initially recognized at fair value, net of transaction costs. For interest-bearing loans and borrowings this is the fair value of

the proceeds received net of issue costs associated with the borrowing.

After initial recognition, other financial liabilities are subsequently measured at amortized cost using the effective interest method. Amortizedcostis

calculated by taking into account any issue costs and any discount or premium on settlement. Gains and losses arising on the repurchase, settlement

or cancellation of liabilities are recognized in interest and other income and finance costs respectively.

This category of financial liabilities includes trade and other payables and finance debt, except finance debt designated in a fair value hedge relationship.

Derivative financial instruments and hedging activities

The group uses derivative financial instruments to manage certain exposures to fluctuations in foreign currency exchange rates, interest rates and

commodity prices, as well as for trading purposes. These derivative financial instruments are recognized initially at fair value on the date on which a

derivative contract is entered into and subsequently remeasured at fair value. Derivatives are carried as assets when the fair value is positive and as

liabilities when the fair value is negative.

Contracts to buy or sell a non-financial item (for example, oil, oil products, gas or power) that can be settled net in cash, with the exception of contracts

that were entered into and continue to be held for the purpose of the receipt or delivery of a non-financial item in accordance with the group’s

expected purchase, sale or usage requirements, are accounted for as financial instruments. Gains or losses arising from changes in the fair value of

derivatives that are not designated as effective hedging instruments are recognized in the income statement.

If, at inception of a contract, the valuation cannot be supported by observable market data, any gain or loss determined by the valuation methodology is

not recognized in the income statement but is deferred on the balance sheet and is commonly known as ‘day-one gain or loss’. This deferred gain or

loss is recognized in the income statement over the life of the contract until substantially all the remaining contract term can be valued using

observable market data at which point any remaining deferred gain or loss is recognized in the income statement. Changes in valuation subsequent to

the initial valuation are recognized immediately through the income statement.

112 BP Annual Report and Form 20-F 2015