ADT 2009 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2009 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

|

|

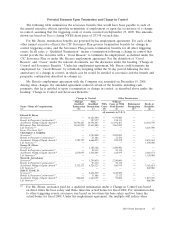

Potential Payments Upon Termination and Change in Control

The following table summarizes the severance benefits that would have been payable to each of

the named executive officers upon his termination of employment or upon the occurrence of a change

in control, assuming that the triggering event or events occurred on September 25, 2009. The amounts

shown are based on Tyco’s closing NYSE share price of $33.98 on such date.

For Mr. Breen, termination benefits are governed by his employment agreement. For each of the

other named executive officers, the CIC Severance Plan governs termination benefits for change in

control triggering events, and the Severance Plan governs termination benefits for all other triggering

events. In all cases, a ‘‘Qualified Termination’’ means a termination following a change in control that

would provide the executive with a ‘‘Good Reason’’ to terminate his employment, as defined under the

CIC Severance Plan or under Mr. Breen’s employment agreement. For the definition of ‘‘Good

Reason’’ and ‘‘Cause’’ under the relevant documents, see the discussion under the heading ‘‘Change in

Control and Severance Benefits.’’ Under his employment agreement, Mr. Breen could terminate his

employment for ‘‘Good Reason’’ by voluntarily resigning within the 30-day period following the first

anniversary of a change in control, in which case he would be entitled to severance and the benefit and

perquisite continuation described in column (c).

Mr. Breen’s employment agreement with the Company was amended on December 19, 2008.

Among other changes, the amended agreement reduced certain of the benefits, including cash

payments, that he is entitled to upon a termination or change in control, as described above under the

heading ‘‘Change in Control and Severance Benefits.’’

Change in Control Other Termination

Without With Without

Qualified Qualified With Cause or With Retirement/ Death or

Name / Form of Compensation Termination Termination Cause Good Reason Resignation Disability

(a) (b) (c) (d) (e) (f)(7) (g)

all amounts in U.S. $

Edward D. Breen

Severance(1) ........................ — 14,625,000 — 9,750,000 — —

Benefit & Perquisite Continuation(2) ......... — 327,197 — 218,131 — —

Accelerated Vesting of Equity Awards(3) ........ 16,596,487 16,596,487 — 16,596,487 — 12,032,970

Retirement Plan Distributions(4) ............ 13,643,000 13,643,000 — 3,861,000 — —

Life Insurance(5) ..................... — — — — — 3,245,000

Excise Tax Gross Up(6) ................. — — — — — —

Christopher J. Coughlin

Severance(1) ........................ — 4,784,000 — 3,200,000 — —

Benefit & Perquisite Continuation(2) ......... — 31,086 — 23,132 — —

Accelerated Vesting of Equity Awards(3) ........ 1,789,727 4,466,299 — 229,952 — 2,838,562

Life Insurance(5) ..................... — — — — — 1,500,000

George R. Oliver

Severance(1) ........................ — 2,188,148 — 2,400,000 — —

Benefit & Perquisite Continuation(2) ......... — 23,132 — 23,132 — —

Accelerated Vesting of Equity Awards(3) ........ 1,674,093 3,548,083 — 160,979 — 2,484,373

Life Insurance(5) ..................... — — — — — 1,150,000

Naren K. Gursahaney

Severance(1) ........................ — 1,204,650 — 2,240,000 — —

Benefit & Perquisite Continuation(2) ......... — 23,132 — 23,132 — —

Accelerated Vesting of Equity Awards(3) ........ 2,352,333 4,226,323 — 160,979 — 3,162,614

Life Insurance(5) ..................... — — — — — 840,000

John E. Evard, Jr.

Severance(1) ........................ — 2,406,950 — 1,610,000 — —

Benefit & Perquisite Continuation(2) ......... — 31,086 — 23,132 — —

Accelerated Vesting of Equity Awards(3) ........ 504,603 1,664,155 — 99,600 — 1,019,479

Life Insurance(5) ..................... — — — — — 866,000

(1) For Mr. Breen, severance paid for a qualified termination under a Change in Control was based

on three times his base salary and three times his actual bonus for fiscal 2008. For termination due

to other triggering events, severance was based on two times his base salary and two times his

actual bonus for fiscal 2008. Under his employment agreement, the multiple will reduce when

2010 Proxy Statement 65